Jamie Dimon IS WRONG: Consumer Balance Sheet Is Not Strong

The estimated reading time for this post is 144 seconds

Consumers’ balance sheet is not strong; for the second quarter of 2019, America’s total household debt was $13.86 trillion. During a 60-minute interview, JP Morgan Chase’s CEO Jamie Dimon told Lesley Stahl that the American consumer’s balance sheet is strong. However, when you look at the total of personal loans, car loans, student loans, mortgages, and credit cards, Americans are overleveraged.

Easy access to money makes consumers look wealthier than they are. According to the Federal Reserve Bank of New York, for the second quarter of 2019, America’s total household debt was $13.86 trillion. In nominal terms, Americans hold more debt now than they did at the peak of $12.68 trillion in the third quarter of 2008. American consumers’ balance sheet is a long way from being strong.

Consumer Balance Sheet

A balance sheet or statement of financial position tally up a consumers’ assets and liabilities. The difference is the consumer’s current net worth, which can be either negative or positive.

In Jamie Dimon’s parlance, a strong balance sheet means American consumers’ total assets outweigh their liabilities. America’s total household debt and the resurgence of payday lending stores and car title loans tell a different story. Consumers are financing most, if not all, material items they purchase.

Strong Balance Sheet

Consumers’ Balance Sheet

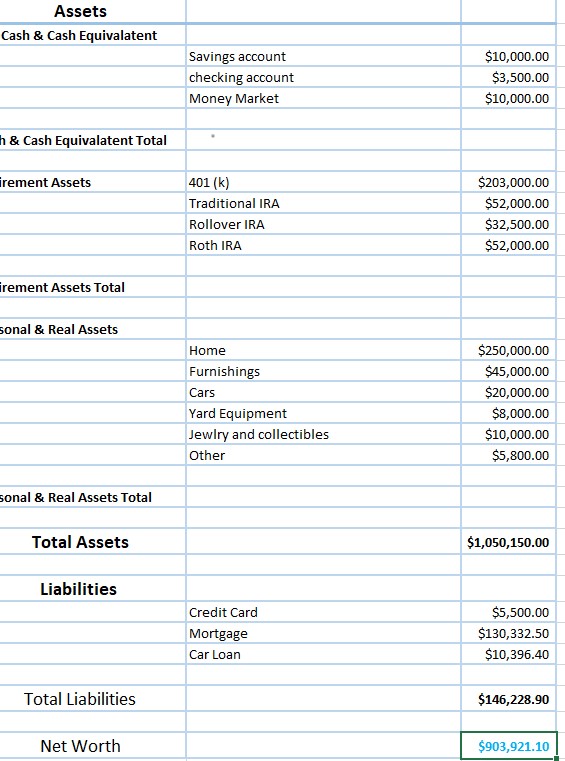

The Statement of Financial Position to the right is how a healthy one is supposed to look. It has a sizable amount of liquid assets or emergency funds. Savings and checking accounts and money market funds are all well-funded.

We know that most people don’t have $23,500 sitting in cash and cash equivalent that they can draw from in case of an emergency. Matter of fact, a Federal Reserve survey revealed two years ago that 40 percent of Americans don’t have $400 in the bank for an emergency.

2007-09 financial crisis eviscerated Americans’ retirement portfolios. The S&P 500, The Dow Jones Industrial Average, and Nasdaq are all at historic highs. However, the stock market stratospheric growth over the past decade did not benefit most Americans. They cashed out their 401 (k) during the recession and completely missed out on the historic market growth.

Real estate is the best, and sometimes the only way the middle class can build wealth and increase their net worth. Nearly 10 million homeowners lost their homes to foreclosure during the 2007-2009 financial crisis.

A decade after the financial crisis, the middle class is still recovering. More and more Americans now see a mortgage as a total bad debt because of their experience or their parents.

The Bottom Line

The bottom line is that American consumers’ balance sheet is not strong. They are financing cars for 108 months, using payday lending excessively, and spending a majority of their income on rents. Financial institutions that serve them are racking billion dollars in profits, even in this environment of low-interest rates.

Pingback: Should You Follow Becky Quick and Invest 100 Percent in Equities - FMC