Investors Need to Netflix and Chill

The estimated reading time for this post is 181 seconds

Investors need to Netflix and chill and cancel all the noise coming from Wall Street analysts. The company announced yesterday that it lost net subscribers for the first time in its 2 ½ decades; its shares plunged 20% in after-hours trading.

However, unlike many analysts and investors, I don’t think the company’s best days are behind it.

The streaming media giant is down nearly 35%, trading at a 52-week range low.

Net subscribers decline, geopolitical problems ( it has to exit Russia), and password-sharing are great reasons for investors to be wary, but their reaction might be exaggerated.

The world’s leading entertainment service company has an outstanding balance sheet, excellent operating margin, free cash flow, and nearly $1.3 billion in deferred revenue, meaning that many subscribers opt to pay for their membership yearly.

Analysts Concerns

Wall Street analysts are concerned that net subscribers decline and missed revenue expectations might signal that Netflix’s growth, which has been going on by leaps and bounds since 2011, has seen its best days.

They might be correct, but that does not mean you should abandon the stock. You might miss out on excellent future dividend yields and long-term capital appreciation if you decide to sell.

Netflix has become a staple for most consumers, and it has a wide moat; its days of stratospheric growth might be over, but the company will create excellent shareholder value in years to come.

With 222 million paid memberships in over 190 countries, slow growth should be expected as the incremental subscriber is getting thinner and thinner.

During the earnings call, the company CEO, Reed Hastings, said the following,

“We’re working on how to monetize sharing. We’ve been thinking about that for a couple of years, but when we were growing fast, it wasn’t the high priority to work on. And now we’re working super hard on it. And remember these are over 100 million households that already choose to view Netflix. They love the service, we just got to get paid,” Hastings told investors on the earnings call. “And then two, it’s really, we got great competition. They’ve got some very good shows and films out. And what we got to do is take it up a notch.”

To resolve the problems that Mr. Hasting outlined above, the company must move its focus from growth to value investors. Otherwise, the stock volatility will continue.

Why You Should Not Worry

Revenue Growth

Netflix missed its Q1 2022 revenue expectations, but revenues have grown consistently for the past nine quarters. The 2.5% revenue growth from Q4 2021 to Q1 2022 is way above the Global Entertainment and Media market’s projected growth of 5.9% compound annual growth rate (CAGR).

Most importantly, the pace of revenue growth is consistent with what value investors expect.

Reed Hastings talked about the ‘great competition and very good shows and films out” during the earnings call. The CEO is correct. The streaming service competition is brutal. Netflix can allocate nearly $1B towards content creation next quarter without hurting the operating margin. I was surprised to see an 18.2% decrease in the cost of revenue for the quarter.

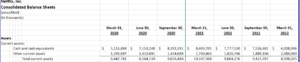

Balance Sheet

The firm has a sound balance sheet with more than $6 billion in cash and cash equivalents. It has no short-term debt. Its total current assets can cover its current liabilities more than 1x.

Balance Sheet

I find the early $1.3 billion in deferred revenue fascinating. Moreover, more than 100 million households view Netflix for free through password-sharing. Consumers love this company, and value investors might be too.