Debt Consolidation Risks for Homeowners Using Cash-Out Refis

Most middle-class debt stories don’t start with a shopping spree. They start with something that feels responsible: trying to “clean up” your credit card debt and do the grown-up thing.

You finally pick up the phone, call a lender, and say the words you’ve been rehearsing: “I’m trying to do the right thing. I want to consolidate my debt.”

On paper, it looks smart. You own a home. You’ve got equity—thanks to years of payments and wild home-price growth. You’re carrying $20,000 on credit cards at 25% interest. The lender suggests a cash-out refinance:

“We roll those balances into your mortgage, you wipe the cards clean, and your monthly budget can breathe again.”

You sign. The cards go to zero. For a moment, you feel light.

Fast-forward 18–24 months. The mortgage is bigger and more expensive than your old one. The payment crept up another few hundred dollars a month. And the credit card balances? They quietly climbed back into five figures.

Old debt, new debt, same income.

That’s the double-debt trap: house debt plus new card debt. It’s the dark side of debt consolidation risks nobody puts in the glossy brochure—and it’s hitting working- and middle-class homeowners harder than anyone wants to admit.

We’re going to walk through why this happens, what really happens when you roll card debt into your mortgage, and how a simple 90-day protocol can keep you from turning your house into an ATM and your future into collateral.

How We Got Here: Record Debt and the Home-Equity ATM

Start with the big picture.

Household debt in the U.S. is at record highs when you add up mortgages, car loans, student loans, and revolving balances—the full stack. Credit card balances alone sit north of the trillion-dollar mark. Delinquencies and defaults have climbed, especially for younger borrowers and households already stretched by rent, food, childcare, and gas.

At the same time, home prices shot up over the last few years. That means millions of homeowners are sitting on what the industry likes to call “tappable equity.”

Translation: your house is worth way more than your mortgage balance, and lenders see an opportunity.

Cash-out refinances have quietly taken over what’s left of the refinance market. Instead of refinancing just to get a lower interest rate, people are now refinancing to pull cash out. Recent data shows a large share of refinances are cash-out deals where borrowers are pulling tens of thousands of dollars out of their homes, on average, and raising their mortgage rate and monthly payment to do it.

And what do people say they’re using that cash for?

“Paying off other bills or debt.”

Of course they are. Cash-out borrowers, on average, are more likely to carry big balances on their cards and have more non-mortgage debt than homeowners who don’t cash out. When the pressure gets too high, someone finally mentions the magic phrase:

“Why don’t we use our home equity to knock this out?”

That’s the setup. Here’s the punchline.

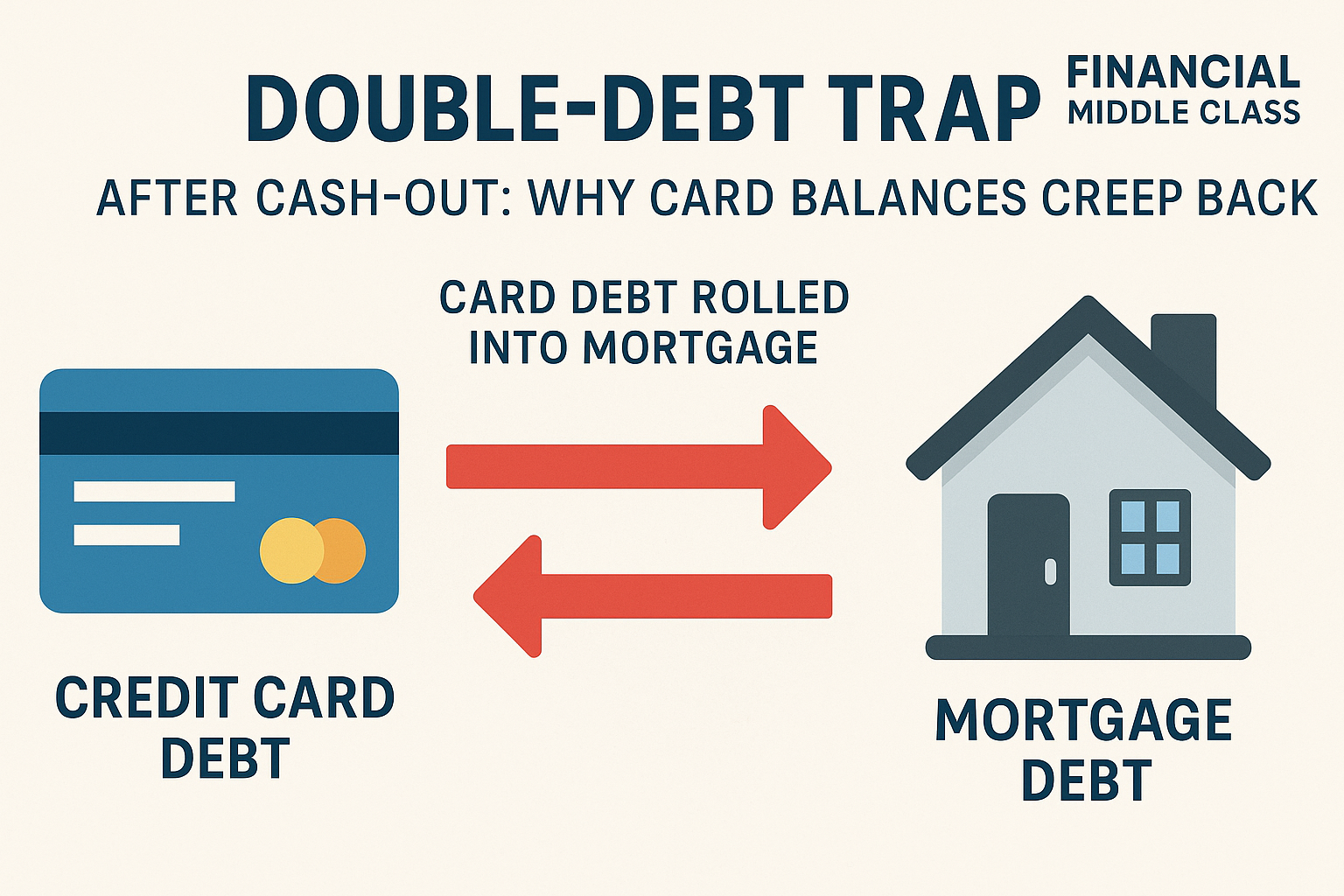

The Double-Debt Trap: What Really Happens After the Cash-Out

When researchers followed homeowners who did cash-out refinances, they saw a pattern that should make your stomach drop.

Right after the cash-out refi, credit card balances do fall. You sign the paperwork, the loan closes, the equity hits your account, and the cards get paid down. For a few months, those statements look beautiful.

Then time passes.

Within a couple of quarters, those same households start swiping again. Balances slowly creep back up. A few hundred here. A “temporary” charge there. A true emergency, yes, but also a bunch of “I’ll just put it on the card for now.”

Within a year or two, the average cash-out borrower often ends up with higher card balances than a similar homeowner who never cashed out at all.

So now, instead of:

- A smaller mortgage + big cards

You have:

- A larger, more expensive mortgage

- Plus new card balances starting to stack on top

That’s the double-debt trap.

And here’s the part that doesn’t show up in the refi pitch: once you’ve proven to yourself that you can “fix” a credit card problem by raiding your house, mentally, that option starts to live in the back of your mind.

“Worst case, we can always refinance again.”

You won’t say it out loud. But the brain remembers.

Am I Walking Into the Double-Debt Trap?

Answer these honestly. If you get a high score, you should not be rolling card debt into your house yet.

Financial Middle Class • Educational tool, not individual advice.

Why Rolling Card Debt Into Your House Is Different (and More Dangerous)

Plenty of people hear, “Debt is debt, what’s the difference what bucket it’s in?”

There’s a huge difference.

1. You’re trading unsecured debt for secured debt

Credit cards are unsecured. If you stop paying, the bank can wreck your credit, send you to collections, maybe sue you. That’s serious. But the card company can’t auction off your living room.

Your mortgage is secured by your home. You miss enough payments, and the thing you’re risking is the roof over your head. When you roll cards into your mortgage, you’re literally betting the house on your ability to never fall behind again.

That might be fine if your debt came from a one-time hit—medical bills, a layoff, a divorce—and your income is now stable. It is absolutely not fine if those balances came from years of overspending, lack of a real budget, and “I’ll worry about it later.”

Because “later” just got a deed attached to it.

2. The tax-break story is often a myth

A lot of people still think, “Well, at least mortgage interest is tax deductible.”

Not always. Tax rules now generally require that home-equity interest be tied to buying, building, or substantially improving the home. Paying off old credit card debt usually doesn’t qualify.

So if you’re imagining a neat little triangle—credit cards → mortgage → tax break—you’re probably drawing the wrong diagram.

3. The 30-year illusion: lower monthly, higher lifetime cost

Here’s the sneaky part: rolling $20,000 of credit card debt into a 30-year mortgage can absolutely drop your monthly payment. The spreadsheet will show a quick win.

Instead of sending $600 per month across several cards, you might only see your mortgage go up by $130–$150.

The cash flow feels better. But if you stretch that $20,000 over three decades at mortgage rates, you could easily pay more in interest over time than if you had just hit the debt hard and killed it in three to five years.

Lower monthly does not mean cheaper debt. It means slower, longer, stickier debt.

Cash-Out vs Kill-the-Cards: Which Costs More?

Enter rough numbers to see how much interest you could pay if you roll card debt into a 30-year mortgage instead of attacking it directly.

Your Card Debt

If You Roll It Into the Mortgage

Financial Middle Class • Estimates only. Real-world numbers will vary.

Combine that with a bigger, more expensive mortgage and a shaky economy with rising defaults, and you’ve created a fragile situation. One disruption—job loss, illness, another emergency—and there’s a lot more at stake.

The Behavioral Side: Why Balances Creep Back Even When You “Know Better”

Let’s be honest: most of us can do basic math. We know 25% interest is bad. We know maxing out cards is dangerous. We know a bigger mortgage is a big commitment.

So why do balances creep back anyway?

Because this isn’t about knowledge. It’s about how human beings actually behave under stress.

Present bias: “Future Me will handle that”

We’re wired to overweight today and discount tomorrow. Today’s relief, today’s “yes,” today’s convenience—it all feels heavier than some abstract future consequence.

The problem is that debt feeds off that bias. Every time you say, “I’ll just put this on the card and figure it out later,” you’re making a tiny bet against your own future energy and income.

When you’ve just had a “fresh start” from a cash-out refi, present bias gets louder: “We’re not in crisis now. It’s fine. We’ll pay extra next month.” Next month never shows up.

Mental accounting: “That was old debt; this is new money”

When you roll credit card debt into your mortgage, your brain files that old balance under “house stuff”: mortgage, taxes, insurance. A whole different category.

Now when you swipe your card at Target or book a flight or order takeout, it doesn’t feel like the same debt coming back. That was old debt. This is new spending. You tell yourself it’s temporary or exceptional.

It’s not. It’s the same behavior that filled the cards last time—just on a new cycle.

If you want to go deeper on this, read our behavioral primer on how money habits actually form and why willpower alone doesn’t cut it.

Debt illusion and the minimum-payment trick

Your credit card statement shows you a minimum due. Your mortgage shows you one monthly number. None of those documents are in the business of telling you, in plain English, “Keep this up and you’ll spend the next 15 years paying for last year’s DoorDash.”

We fixate on what fits this month. We rarely confront the total cost over the full timeline.

Lenders don’t have to lie to you. They can simply frame the numbers in a way that emphasizes comfort now and hides pain later. Your brain happily fills in the gap with optimism:

“It’ll be different this time. I’ve learned my lesson.”

Have you? Or did you just sign different paperwork?

Shame and the avoidance loop

There’s one more piece: shame.

Debt is one of the most isolating forms of stress. Middle-class folks especially are taught to believe, “If you’re in debt, you’re irresponsible.” So what do people do when the statements make them feel irresponsible?

They stop opening the statements.

They delete the emails. They avoid logging into accounts. They promise themselves they’ll take a hard look “once things calm down.”

Avoidance is exactly how balances creep. You can’t fix what you refuse to see.

When Debt Consolidation Can Actually Help (If You Don’t Lie to Yourself)

Let’s be fair. Not all consolidation is evil. In some cases, it’s rational.

It can make sense if you’re replacing chaotic, high-rate debt with a lower-rate, fixed-term loan; if you have a clear payoff timeline and a budget that supports it; if the debt came from a one-time crisis and your income is stable now. And it can only work if you’re willing to close or freeze the accounts that caused the problem in the first place.

It becomes dangerous if you plan to keep all the cards open “just in case,” if you don’t have a written budget, if you’ve “started fresh” before and ended up right back in the same spot, or if the main goal is “freeing up cash every month” with no specific plan for that freed-up cash.

Here’s a simple test:

If you haven’t changed the behavior that created the debt, you have no business strapping that debt to your house.

And you don’t fix behavior with good intentions. You fix it with structure.

The 90-Day Freeze: A Habit Protocol to Keep You Out of the Double-Debt Trap

You cannot spreadsheet your way out of a debt problem that is driven by habits. You need a season where the rules are different—where you train new reflexes before you touch your home equity or sign a consolidation loan.

Ninety days is a good starting point. Long enough to break patterns. Short enough to feel like a sprint.

Phase 0 (Prep Week): Count the Cost Before You Sign Anything

Before you talk to a lender, sit down with your numbers.

- List every card

Balance, interest rate, minimum payment. - Map your real budget

Take-home pay, fixed bills (housing, utilities, car, insurance, groceries, minimum debt payments), and what’s left over. Be honest. - Ask one blunt question:

“If we keep living exactly like this, will our debt be higher or lower a year from now?”

If the answer is “higher” and you still think using your house as a bailout is a solution, stop. You’re about to drag the same problem into a much more fragile place. Commit to a 90-day experiment first.

Your Debt Snapshot (Before You Touch the House)

Fill this in, then hit "Calculate Totals." You shouldn’t be signing a cash-out or consolidation loan if you can’t see every card and every rate in one place.

| Card / Lender | Balance ($) | APR (%) | Minimum Payment ($) |

|---|---|---|---|

Financial Middle Class • Reality first, decisions second.

Phase 1 (Days 1–30): Freeze and Automate

1. Freeze the cards. Not “I’ll try not to use them.” Freeze them.

- Take them out of your wallet.

- Put them in a drawer, a locked box, or literally a bag of ice in the freezer.

- Log into each card app and turn off “tap to pay” and saved card info wherever possible.

If you leave a card in your phone wallet, you did not freeze it. You just made it lighter.

2. Autopay above the minimum. Set up automatic payments for each card that are at least 1.5–2x the minimum, or a fixed dollar amount you know you can sustain.

If the minimum is $80, set autopay to $150. If the minimum is $35, make it $75. You’re sending a signal: “Bare minimum is not my plan anymore.”

3. Weekly Money Check-In. Pick one time each week—say, Sunday evening. Put it on your calendar. During that 20–30 minutes, log into each account, write down balances and payments made, celebrate small wins, and notice setbacks without beating yourself up.

4. Script your boundaries. You’ll run into invites, requests, and temptations. Prepare the words now: “We’re in a 90-day no-credit reset. If we can’t pay cash, we’re going to skip it.” You don’t owe anyone a full explanation.

Phase 2 (Days 31–60): Build Better Spend Lanes

Now that you’ve survived the first month without spontaneous swipes, it’s time to make the new behavior easier to maintain.

Create “spend lanes” with separate accounts for essentials and discretionary spending. When the fun account is empty, fun is paused. No “just put it on the card.”

Define emergencies in advance, on paper. Practice redirecting windfalls—tax refunds, bonuses, side money—toward debt instead of new obligations.

Phase 3 (Days 61–90): Decide From Reality, Not Hope

By the time you hit day 60, you’ve collected data on yourself. Did you leave the cards frozen? Did you stick with autopay above the minimum? Did you actually follow your weekly money check-in?

If the honest answer is no, you just learned something extremely valuable: you are not ready to strap this behavior to your house. That’s not a moral failing. It’s feedback. You need more time in training mode, not a bigger loan.

If the answer is yes—if balances are actually trending down, your budget is real, and you’ve made it two months without sneaky swipes—then you have options.

If you still choose to consolidate after 60–90 days, keep most cards closed or frozen, give any card you keep one job only, and treat the new payment as the floor, not the ceiling. If you decide not to consolidate, keep running the protocol and extend it.

90-Day Freeze Protocol Tracker

Use this tracker for the next 13 weeks. Each week, check off the basics: cards frozen, autopay ran, and you did a money check-in.

| Week | Cards still frozen? | Autopay above minimum ran? | Weekly money check-in done? |

|---|

Financial Middle Class • Screenshot or print this if you want to keep a paper copy on the fridge.

Join the 90-Day Freeze Challenge

If you’re serious about staying out of the double-debt trap, don’t try to white-knuckle this alone. Join the Financial Middle Class 90-Day Freeze Challenge and get:

- A 1-page printable version of the 90-day protocol

- Weekly email prompts for your money check-in

- Short lessons on habits, not hacks

By subscribing, you agree to receive Financial Middle Class updates. No spam, ever—just tools to build a real middle-class balance sheet.

Debt Consolidation Risks: FAQ

Is it smart to roll credit card debt into my mortgage?

It can make sense only in narrow cases: your income is stable, the debt came from a one-time event, the new loan has a lower rate and fixed payoff, and you are closing or freezing the cards that caused the debt. For many households, rolling card balances into a mortgage just turns short-term unsecured debt into long-term secured debt backed by your home, increasing foreclosure risk if something goes wrong.

What are the biggest debt consolidation risks for homeowners?

The big ones: converting unsecured card debt into secured housing debt, stretching balances over 20–30 years so total interest explodes, assuming mortgage-style tax deductions that may not apply, and failing to change the spending habits that created the card balances. That’s how people end up with both a larger mortgage and new revolving debt a year or two later.

How do I avoid running my credit cards back up after consolidation?

You avoid rebuilding balances by changing behavior before and after any consolidation: freeze or close most cards; set autopayments above the minimum; run a weekly money check-in; separate essential spending from fun money in different accounts; and use a 60–90 day “freeze” period to prove you can live within a realistic budget. If you can’t keep those habits for a few months, you’re not ready to tie the debt to your house.

Is a HELOC safer than a cash-out refinance for paying off debt?

Both use your home as collateral, so both can end badly if payments are missed. HELOCs are more flexible but can encourage ongoing borrowing. A cash-out refi locks the balance into a long fixed term. The safer move in either case is to borrow as little as possible, keep the payoff period short, and treat the line or cash-out as a one-time bridge—not a lifestyle subsidy.

If you want to compare options in more detail, pair this article with our breakdown of cash-out refinance vs. HELOC and our guide to debt snowball vs. avalanche vs. consolidation loans.

Your House Is Shelter, Not an ATM

Here’s the quiet truth no one making money off your debt consolidation risks is going to say out loud:

Your home is not supposed to be a line of credit. It’s supposed to be shelter, stability, and—if we’re lucky—an asset that quietly grows in the background while you live your life.

Every time you raid that asset to plug holes in a leaking budget, you make the whole structure shakier. You blur the line between “my family’s shelter” and “my lifestyle funding machine.”

The real flex isn’t a lower monthly payment on a bigger mortgage. The real flex is fewer creditors, lower stress, and more margin. That’s what gives you options when life happens.

If you’re staring at credit card balances right now and you’re tempted to solve it with a cash-out refi, here’s your move:

Run the 90-day freeze first.

For three months, freeze the cards, autopay above the minimum, check in weekly, build spend lanes, and practice saying no. At the end of those 90 days, you’ll have the one thing you don’t get from a lender: a clear look at your own habits.

And that clarity might be worth more than any equity check you’ll ever sign.