Universal Basic Income Is a Middle-Class Policy

By FMC Editorial Team

The estimated reading time for this post is 526 seconds

I. The Middle-Class Mirage

Every few election cycles, the American middle class is asked to choose between its ideals and its interests. Too often, it chooses the wrong one. It rallies against unions that once secured its weekends, votes to cut unemployment benefits that could cushion its own job loss, and supports budget cuts that weaken the very programs that sustain its purchasing power.

The middle class—the largest voting bloc in America—has been convinced that economic safety nets are “handouts” for the poor. That framing has been politically effective but economically disastrous. Because in truth, the middle class has far more in common with the working poor than with the ultra-rich who shape the economic narrative.

Universal Basic Income (UBI) may be the next victim of this misunderstanding. Often dismissed as “welfare,” UBI is actually one of the few modern policies that could restore balance to a lopsided economy. It’s not a bailout for the poor—it’s insurance for the middle class.

II. The Great Divergence: How Wealth Left the Middle Class Behind

The story of American prosperity since the 1980s is not one of collective growth—it’s one of selective enrichment. While productivity and corporate profits expanded, wage growth for typical workers stalled and the middle-class share of wealth fell toward pre-war levels.

According to the Federal Reserve’s Distributional Financial Accounts, as of late 2024/2025 the top 10% of households hold roughly 67% of all household wealth, leaving the bottom 90% with about 33%.

Recent quarters also saw record wealth levels at the very top, with multiple analyses noting the top 1% around one-third of household wealth and levels hitting fresh highs in 2025 amid market gains.

The main driver of these gains? Equities. Stock ownership, buybacks, and capital gains concentrate wealth among those who already own capital, while wage earners struggle to keep pace with living costs.

U.S. wealth distribution (late 2024–2025)

- Top 10%: ~67% of total household wealth

- Bottom 90%: ~33%

Sources: Federal Reserve DFA / St. Louis Fed.

III. The Algorithm Economy: Profit Without People

In the twentieth century, prosperity was tied to labor. In the twenty-first, it’s tied to code. A platform can create billions in shareholder value with a fraction of the workforce.

2018 example: Facebook (now Meta) reported $55.8B in revenue with 35,587 employees—about $1.6M per employee. Walmart reported $500.3B in revenue with ~2.3M employees—about $217K per employee. Most of that surplus accrues to shareholders at the top.

Meanwhile, productivity and typical workers’ pay have pulled apart: since 1979, productivity rose about 81% while average hourly compensation rose about 29% (through 2024–2025). That’s the collapse of the postwar compact: hard work no longer guarantees rising living standards.

IV. What Is UBI—and Why It’s Misunderstood

UBI is simple: periodic, unconditional cash to every adult citizen, regardless of income or employment.

The idea has deep roots—from Thomas Paine to Martin Luther King Jr. to Milton Friedman’s negative income tax (a cousin of UBI). The digital economy doesn’t guarantee employment, yet it generates unprecedented wealth; UBI recycles a fraction of that productivity to maintain stability and spending power.

Today, many in the middle class see UBI as a “handout.” That misses a hard reality: the middle class itself is increasingly precarious.

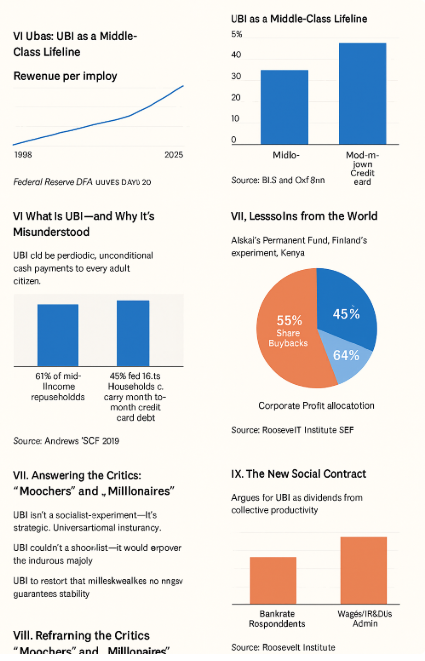

V. UBI as a Middle-Class Lifeline

The middle class is defined not by wealth, but by risk—mortgages, childcare, tuition, healthcare, retirement. A modest UBI—say $1,000/month—wouldn’t replace work; it would reinforce it by cushioning shocks, reducing high-interest borrowing, and enabling education or entrepreneurship.

As Andrew Yang argued in 2020, the “Freedom Dividend” could act as a shock absorber in an era where automation decouples work from income.

Household financial fragility (2025 snapshot):

Only 41% say they could cover a $1,000 emergency expense from savings; the rest would borrow, cut spending, or use credit.

About 46% of cardholders carry a month-to-month credit-card balance.

UBI, in this context, isn’t charity—it’s macroeconomic stabilization: when middle-class families can spend, small businesses thrive and communities are steady.

VI. Answering the Critics: “Moochers” and “Millionaires”

Two common critiques:

- “UBI creates moochers.” Evidence says otherwise. In Finland’s national experiment, recipients saw no significant drop in employment and higher well-being. Alaska’s long-running dividend shows no negative effect on employment and a modest rise in part-time work—consistent with local demand effects from cash.

- “Why give money to the rich?” Universality is a feature, not a bug. It minimizes stigma and bureaucracy—like Social Security—and is politically durable. The wealthy can always donate or be taxed back.

UBI won’t conjure freeloaders; it gives the industrious majority room to navigate volatility with dignity.

VII. Lessons from the World

- Alaska Permanent Fund (since 1982): Annual dividends with no reduction in employment; part-time work increases slightly.

- Finland (2017–2019): Modest employment effects; better perceived economic security and mental health.

- Kenya (GiveDirectly): Early results from a long-term UBI trial show recipients using funds to start businesses and improve outcomes, with cash proving productive rather than dependency-inducing.

- U.S. pandemic relief (2021): Direct cash and an expanded Child Tax Credit helped push child poverty to a record low (5.2%)—which reversed when supports ended.

Direct cash works.

VIII. Reframing UBI as Capitalism’s Insurance Policy

UBI isn’t socialism’s trial run—it’s capitalism’s seatbelt. Profits and market caps can’t float indefinitely if consumers lack purchasing power.

Consider corporate cash flows: in 2024, S&P 500 companies returned a record ~$1.6T to shareholders, including $942.5B in buybacks; Q1 2025 alone set a quarterly buyback record (~$293.5B), and major banks projected >$1T in 2025 repurchases. Meanwhile, corporate profits’ share of national income sat near recent highs (≈16.2% in late 2024) as labor’s share edged down.

Earlier research already flagged the long-run tilt toward payouts over reinvestment. From 2003–2012, S&P 500 firms spent ~54% of earnings on buybacks and ~37–39% on dividends. UBI effectively recycles a sliver of capital income back into broad demand—preserving the very system that created the wealth.

IX. The New Social Contract

UBI can be framed as a dividend on shared productivity. The internet, GPS, microchips, vaccines—foundational technologies were seeded by public investment; private fortunes compounded on public platforms. If society creates the conditions for wealth, society merits a modest return.

It’s also about time: a guaranteed floor lets parents be with kids, caregivers support aging relatives, and workers retrain or start businesses—without one bad month turning into ruin.

Ultra-wealth growth context: The global UHNW population (>$30M) surpassed 510,000 by mid-2025, with North America the largest hub. The U.S. contains a disproportionate share of this growth.

As the number of people living off capital compounds, the wage-only majority faces structural risk. UBI isn’t radical—it’s adaptive.

X. Conclusion: Saving the Middle Class Is Saving Democracy

The middle class built America’s identity—suburbs, small businesses, durable demand. Today that foundation is cracking; debt replaces savings, anxiety replaces stability.

UBI offers a third leg under the middle-class stool—alongside work and savings. We can keep pretending corporate tax cuts will trickle down, or we can recognize that prosperity spreads when every household has enough breathing room to participate in the economy.

UBI isn’t a threat to capitalism. It’s its renewal—a way to keep the American Dream within reach for the millions who actually keep the economy alive.

The middle class doesn’t need to fear UBI. It needs to claim it.

XI. Frequently Asked Questions (UBI)

1) What exactly is UBI?

A periodic, unconditional cash payment to every adult—no means test, no work requirement. It’s a floor, not a ceiling: enough to steady households through shocks without replacing work.

2) Would UBI discourage people from working?

Unlikely. Most people work for purpose, benefits, and higher income. Evidence from cash pilots shows little to no drop in employment—and some recipients use the cushion to upskill, switch jobs, or start a business.

3) How is UBI different from welfare?

Welfare is targeted and conditional; UBI is universal and simple. Universality cuts bureaucracy, slashes “benefits cliffs,” and removes stigma—more like Social Security than a patchwork of means-tested programs.

4) How could we fund it without blowing up the budget?

Use a mix: close preferential tax breaks on capital income, add a modest VAT or carbon dividend, apply a surcharge on very large buybacks, and consolidate overlapping cash programs with strict “no one worse off” protections. No single lever has to carry the whole load.

5) Would UBI be inflationary?

Design matters. A predictable, funded UBI—paired with competition policy and phased rollouts—need not drive persistent inflation. Recycling revenue from high-savings households (via taxes/dividends) helps contain demand spikes.

6) What happens to existing benefits?

Two models: (a) layer UBI on top of most programs, or (b) partially consolidate specific cash transfers with hard guardrails so vulnerable groups aren’t harmed. The principle: simplify without stripping essentials.

7) Why give UBI to the rich too?

Universality keeps costs low and errors down, and it builds political durability. High-income households can be “taxed back” on the backend—cleaner than trying to police eligibility at the front door.

8) How does UBI help the middle class specifically?

It smooths volatility—job loss, medical bills, childcare gaps—so families avoid 25% APR credit. It buys time to retrain, care for loved ones, or launch a side business. That steadier demand keeps mortgages current and local shops busy.

9) What about small businesses and entrepreneurship?

A reliable income floor de-risks the leap. Founders can bridge uneven cash flow; customers maintain spending through downturns. UBI supports both sides of the Main Street ledger.

10) Is UBI realistic in the U.S.—federal or state?

Both. Cities and states can run dividends or guaranteed-income pilots now; a durable, scaled version likely requires federal legislation with clear funding, phase-in, and ongoing evaluation.

References

Federal Reserve, Distributional Financial Accounts (2024–2025)

St. Louis Fed (FRED) & BEA, Corporate Profits as a Share of National Income (Q4 2024)

Bureau of Labor Statistics, Productivity and Costs (2025)

Economic Policy Institute, The Productivity–Pay Gap (2024–2025 update)

S&P Dow Jones Indices, S&P 500 Buybacks: 2024 Full Year & Q1 2025 Record (2025)

Reuters / Goldman Sachs, U.S. Share Buybacks Outlook (2025)

U.S. Census Bureau, Supplemental Poverty Measure—Child Poverty 2021–2023 (releases 2022–2024)

Bankrate, Emergency Savings Survey (2025)

Bankrate, Credit Card Debt & Month-to-Month Balances (2025)

Kela (Finland), Basic Income Experiment Final Report (2017–2019; published 2020, cited 2024)

Jones & Marinescu, “The Labor Market Impacts of Universal and Permanent Cash Transfers: Evidence from the Alaska PFD” (latest version)

GiveDirectly, Universal Basic Income (Kenya) Trial Results & Updates (2023–2025)

Wealth-X, World Ultra Wealth Report 2025

Meta Platforms (Facebook), 2018 Form 10-K (revenue & headcount)

Walmart Inc., 2018 Annual Report / Form 10-K (revenue & headcount)

RELATED ARTICLES

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

Leave Comment

Cancel reply

Gig Economy

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

By FMC Editorial Team

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

By MacKenzy Pierre

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan to escape 25% APR debt.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

What To Do If You Get Fired With an Outstanding 401(k) Loan

Fired with a 401(k) loan? Avoid taxes, offsets, and deadline traps with this step-by-step checklist. Read now.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

The Real Math of Money in Relationships

Split finances without resentment. Any couple, any income ratio. Use the worksheet + rules—start today.

By Article Posted by Staff Contributor

American Middle Class / Feb 03, 2026

Investing or Paying Off the House?

Invest or pay off your mortgage? See a $500k example with today’s rates, dividends, and peace-of-mind math—then choose your plan.

By Article Posted by Staff Contributor

American Middle Class / Jan 30, 2026

Gold, Silver, or Bitcoin? Start With the Job—Not the Hype

Gold, silver or Bitcoin? Learn what each is for—and how to size it—before you buy. Read the framework.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Florida Homeowners Pay the Most in HOA Fees

Florida HOA fees are surging. See what lawmakers changed, what’s next, and how to protect your budget—read before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Why So Many Homebuyers Are Backing Out of Deals in 2026

Why buyers are backing out of home deals in 2026—and how to avoid costly surprises. Read the playbook before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 28, 2026

How Money Habits Form—and Why “Self-Control” Is the Wrong Villain

Learn how money habits form—and how to rewire spending and saving using behavioral science. Read the framework and start today.

By FMC Editorial Team

Latest Reviews

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs....

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market...

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan...