Balancing Emotions and Money When the Holidays Hit Hard

By MacKenzy Pierre

The estimated reading time for this post is 1322 seconds

Every year, somewhere between the first Christmas commercial and the last day of school before winter break, otherwise rational people lose their footing.

You know exactly what your money situation looks like. You know how much is sitting on those credit cards, which bill you’re pushing a little too close to the due date, how tight that gap is between payday and “out of money.” You might still be carrying leftovers from last December’s “we’ll figure it out in January” plan.

And yet, one group text about a big family trip, one beautifully staged photo of matching pajamas, one email screaming “50% OFF – TODAY ONLY” can flip a switch in your brain. Suddenly you’re not thinking about interest rates or budgets. You’re thinking about your kids’ faces when they open gifts. You’re thinking about your parents getting older and how many holidays you really have left together. You’re thinking about the year you missed something important and how you promised yourself you’d make up for it.

The holiday season is where emotions and money collide at full speed. When you’re middle class, you’re standing right at that intersection. On one side: genuine love, generosity, nostalgia, even faith. On the other: rent, card balances, student loans, groceries, and wages that haven’t kept up with the price of anything.

This isn’t a lecture about not buying gifts. It’s an honest look at why so many people feel emotionally held hostage by a season they’re supposed to enjoy—and why the bill for that pressure shows up in January, February, and sometimes all the way into the next December.

The goal here is simple: help you build a holiday that your heart can enjoy and your bank account can survive.

When December Hits Both Your Feelings and Your Bank Account

Picture this for a second.

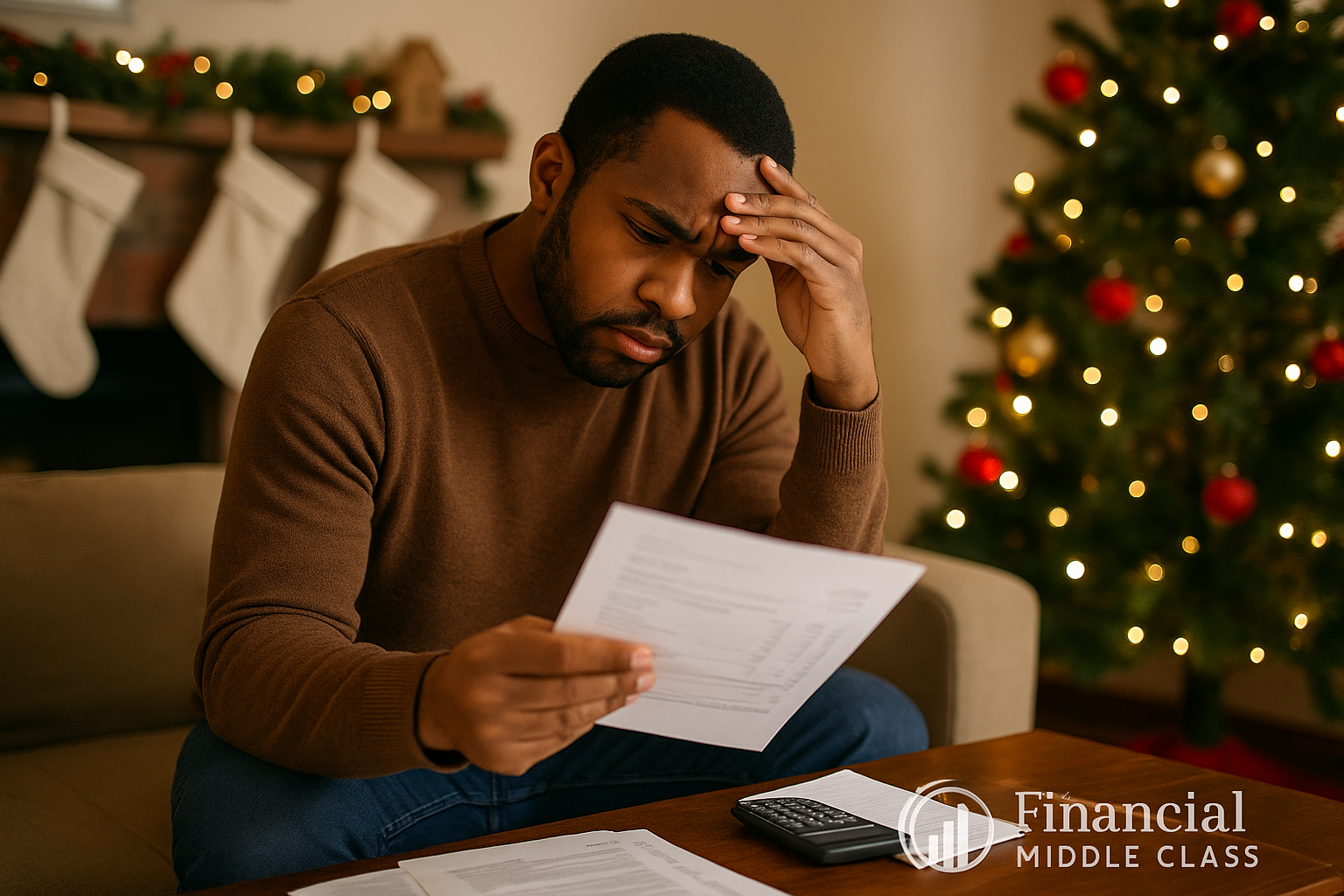

You’re in the parking lot of a big-box store. The air has that damp, chilly feel. Traffic is a mess. Somewhere nearby, a speaker is playing the same three holiday songs on repeat. You’ve been at work all day, you’re tired, and you’ve still got to grab something for the office party and maybe one more gift for your kid because “everyone else in their class” has that thing.

You open your banking app. It’s not a mystery; you already knew the numbers, but seeing them lined up on the screen still hits you. There’s the card with last year’s holiday balance you never fully shook off. There’s the emergency repair from the summer that got parked on a different card. The checking account has just enough lined up to cover the basics if nothing goes wrong.

While you’re staring at those numbers, your phone lights up.

Your child drops a link to a wish list that looks like a monthly paycheck. Your cousin is asking if you’re in for the “let’s do something big this year” rental house. A coworker is reminding the team about the Secret Santa and the charity drive and the optional but not really optional happy hour.

You love these people. You want to show up for your family, your kids, your community. At the same time, a quieter voice in your head is asking, “How on earth are we supposed to afford this?”

That’s the holiday split for a lot of working- and middle-class households. It’s not that you’re “bad with money.” It’s that you’re constantly being asked to prove your love, your stability, your worth, with your wallet—during the one stretch of the year when the pressure is turned all the way up.

The culture around you pushes one message: make it magical, don’t be the only one who doesn’t participate, you work hard, you deserve this. Your bank account is whispering a different message: please don’t do this to us again.

You’re not choosing between being a good person and being good with money. You’re trying to figure out how to care for the people you love without sacrificing your own financial future in the process. That’s not a small question. That’s the whole thing.

The Emotional Volume of the Holidays

From the outside, the holidays are branded as cheerful and simple: lights, food, gifts, family. On the inside, they are anything but simple.

For a lot of adults, December is emotionally loud. There’s genuine joy, sure. There’s also grief when a chair at the table is empty for the first time—or the tenth. There’s loneliness when adult kids can’t make it home, or when you’re the one who moved away. There’s resentment in families where the same person always hosts, always pays, always smooths things over. There’s the quiet ache of “we used to be close” when certain relationships have frayed.

On top of that, there’s comparison. You see friends flying across the country for extended stays in rentals that look better than most people’s permanent homes. You see coworkers who seem to have endless budget for concerts, dinners, and “just a little trip.” You see social media feeds full of curated trees, curated outfits, curated children.

The holidays magnify whatever is already going on inside you. If the year has been hard, that shows up. If you’re already carrying guilt or shame or insecurity around money, that gets louder. It’s like someone takes every unresolved feeling, every family dynamic, every financial worry, and pushes “boost.”

Money is the volume knob on all of this. When money is tight, every invitation, every ask, every “It’s only $25” hits differently. You’re not just asking, “Can we afford this?” You’re asking, “What does it mean if we say no?”

That’s how money stops being math and becomes identity. A gift is no longer just a gift; it’s proof you’re doing okay. A trip is no longer just a trip; it’s proof your kids aren’t missing out. Saying “we can’t” starts to feel like admitting some kind of failure—even though you’re living in the same economy as everyone else, with prices that have quietly climbed up a ladder your paycheck never quite caught.

If you’re the one holding everything together—planning the meals, tracking the events, making sure everyone has a gift, smoothing over family tension—this hits even harder. Parents, especially, absorb a lot of the emotional labor of “making it special.” Kids don’t see the credit card statement, but they see your mood. They feel where the tension is in the house. They can tell when you’re physically present but mentally somewhere else, doing numbers in your head.

Calming your financial stress isn’t just some abstract “responsible adult” move. It’s emotional protection for your home. A smaller, calmer holiday can be healthier for everyone in the room than a big, impressive one that leaves you barely holding it together.

The Numbers Behind the Feelings

Even if you never saw a single commercial, the financial part of this story would be heavy all on its own. Holiday spending is big business. And a lot of that business runs straight through middle-class households that can’t really afford it.

In a typical recent season, surveys show Americans planning to spend somewhere around a thousand dollars on gifts alone. That’s an average, which means some households are much lower and some are much higher, but it gives you an idea of the expectations. Then you add travel, holiday food, work functions, school events, outfits, decorations, “little extras” that don’t feel like much until you add them all up. It’s not hard for a normal family to slide into the low-thousands over the course of a single season.

For people whose wages haven’t kept up with housing, food, and transportation costs, that’s not just a “nice to have.” That’s huge.

The story doesn’t end on December 31. A sizeable chunk of Americans don’t pay off that holiday spending in one shot. They finance it the way everything else gets financed in this country: on credit cards, store cards, and buy-now-pay-later plans. Surveys from the last few years show that roughly one in three holiday shoppers end the season with new holiday debt. The average amount regularly lands over a thousand dollars. Many of those folks are still carrying pieces of that balance when the next holiday season rolls around.

So you’re not walking into December with a blank slate. You’re walking in with last year’s choices still sitting on your statement.

That’s the part that gets missed when the headlines celebrate “record holiday sales.” On paper, the economy looks like it’s thriving because people are spending. On the ground, a lot of that “thriving” is being financed at 20% interest by people called “consumers” in reports and “barely hanging on” in real life.

It’s not evenly distributed either. Higher-income households may complain about prices, but they can usually absorb them without tapping as much high-interest credit. Lower- and middle-income families are more likely to stretch, juggle, and push, hoping overtime, tax refunds, or “something” will eventually help them catch up. They feel every extra dollar more acutely, not because they care more, but because they have less margin for error.

So when you feel like the holidays are pushing you into a corner, you’re not imagining it. You’re standing in the gap between how this season is sold to you and what your actual balance sheet can handle.

Money Wounds and Guilt Gifts

If the holidays were just about numbers, this would be easy. You’d make a budget, stick to it, and call it a day. But there’s a reason so many smart, disciplined people lose control of their spending this time of year. The holidays are where your money story and your emotional story overlap.

A lot of people are walking around with what therapists and financial counselors sometimes call “money wounds.” You don’t have to like the term for it to ring true. These wounds come from growing up in homes where bills were a constant source of fear or silence. They come from hearing “we don’t talk about money” whenever you had a question. They come from being shamed for asking for things, or from never asking because you knew the answer was always going to be no.

They also come from adulthood: the overdraft you still remember because it happened at the worst possible time, the eviction notice, the car that got taken away, the job loss that forced you to survive on a card and a prayer. Those experiences live in your body, not just your memory. They shape how you feel when you walk into a store or open your banking app.

The holidays put pressure on all of that. Old scripts pop up: my kids will not grow up like I did. I refuse to look broke in front of my family again. I’m going to prove I’m doing okay now. That voice in your head is not interested in your budget spreadsheet.

That’s how you end up guilt-gifting. You’re not just buying a toy; you’re attempting to rewrite your childhood or make up for the time you weren’t there. You’re not just buying a plane ticket; you’re buying forgiveness for missing holidays before. You’re not just sending money to a relative; you’re trying to quiet down a feeling you don’t want to sit with.

Add social media to that. You’re not just seeing what your neighbors are doing; you’re seeing how people with much more money—or more credit—are living their holiday season. Photos of elaborate dinners, luxury trips, staged “candid” moments start to feel like the standard. If you’re not careful, you’re no longer asking, “What makes sense for my household?” You’re asking, “How do I keep up with a life that isn’t even mine?”

None of this makes you shallow. It makes you human. You’re swimming in a culture that tells you love, success, and “being a good parent” all have a price tag—and that December is when you prove it. But if you don’t recognize those money wounds and emotional triggers, they’ll drive your spending more than your actual goals ever do.

The Hidden Costs of Pushing Through

Ignoring that stress doesn’t make it disappear. It just makes it more expensive.

Financial anxiety doesn’t stay in your bank app. It shows up in your body. You sleep worse. You feel more on edge. You pick fights faster. You start snapping at the people who live with you instead of at the systems and expectations that are boxing you in.

When two people share a household, this stress often splits into roles. One person becomes the “let them be kids, it’s Christmas” parent. The other becomes the “I’m looking at the actual numbers” parent. If you don’t have a shared plan, every purchase turns into a small referendum on your values. One of you feels controlled, the other feels ignored, and now you’ve got money stress and relationship stress, wrapped in the same torn gift wrap.

Then the calendar flips. The decorations come down. Social media moves on. Meanwhile, the charges don’t go anywhere. They’re quietly accruing interest while you try to deal with the regular emergencies of regular life: a car problem, a medical bill, a layoff rumor at work. And because you’re still paying for last December, you have less room to deal with this March or next June.

This is how the middle class gets stuck. Not because we don’t know better in theory, but because the structure of our financial lives—low savings, high-interest credit, unpredictable costs—collides with the emotional load of “doing the holidays right,” and we don’t give ourselves permission to step off the treadmill.

You can’t control everything about your income or this economy. But you do have more control over how you move through this season than the commercials would like you to remember.

Starting From Values Instead of Sales

Trying to solve holiday stress with “just make a budget” is like telling someone with a sprained ankle to “just walk better.” The budget matters. But the way you use it—and what it’s built around—matters more.

Instead of starting with what’s on sale, start with what actually matters to you. If you stripped away all the noise and had to keep only a few things, what would make the holidays feel real for you?

For some people, it’s sitting around a particular table with a particular set of people. For others, it’s seeing the kids light up during one specific tradition: baking, a movie night, a church service, a volunteer event. Maybe it’s calling a relative in another country and staying on the phone long enough to feel like you really checked in, not just exchanged greetings.

If you can name two or three things like that—the ones that would hurt most to lose—you suddenly have a compass. Those are the things your time and money should protect first. Everything else can get scaled down, moved around, or simply dropped.

Once you know what you care about, then you put numbers around it. Not the other way around.

You don’t need a complicated system. You can divide your holiday spending into a few basic buckets—gifts, food and hosting, travel, everything else—and put a realistic cap on each. Realistic means “this won’t throw the rest of my life into chaos,” not “this is what the commercials say a ‘normal’ holiday costs.”

Write those numbers down somewhere you can’t ignore them. Call them what they are: boundaries meant to protect your future from your feelings in the moment. That’s not cold or unloving. It’s one of the ways you make sure there’s still a roof, still lights, still groceries long after the wrapping paper is gone.

Practical Money Moves You Can Actually Use This Year

Big philosophical shifts are nice. You also need moves you can use when you’re standing in a store or hovering over a “checkout” button.

One move is to create a small, temporary holiday fund even if you’re late in the game. Look at how many paychecks you have left before you hit your main round of holiday spending. Decide what you can realistically carve out of each one without shorting rent, food, or already-existing minimum payments. Park that money in a separate account or at least label it mentally as “holiday only.” That’s your pool. Once it’s gone, the answer is “we’re done,” not “let’s open a new card.”

Another move is to decide how you’re going to use credit before the emotions kick in. If you still have last year’s holiday balance sitting at a painful interest rate, this is not the year for financing big gestures. You might decide you’ll only put something on a card if you’re certain you can pay it off within one or two cycles. You might decide that store cards and buy-now-pay-later offers are an automatic no this year because they blur your sense of what things truly cost.

There are also what I’d call “high-risk days”: the big sale weekends and the frantic last-minute rush days. Instead of letting those days ambush you, you can give them a simple plan: a written list and a hard dollar ceiling. You don’t have to announce it to the world, but you should be honest with yourself. “Today we’re spending no more than this amount, and once it’s gone, we stop.” That alone can keep a bad day from becoming a bad month.

These aren’t magic fixes. They’re small structural choices that keep you from wandering into the most expensive emotional traps.

Handling Feelings Without Swiping Them Away

Balancing emotion and money doesn’t mean turning into a robot. Your feelings are not the enemy. They just shouldn’t be in charge of your Visa.

One of the simplest tools you can use is a pause. Before you buy something, especially something that wasn’t in the plan, ask yourself what’s actually going on. Are you tired? Embarrassed? Pressured? Lonely? Trying to prove something? Trying to avoid a hard conversation?

You don’t have to ask this out loud in the middle of a store aisle. You can do it silently. “What am I hoping this purchase will fix?” If the honest answer is “I want my kid to stop comparing our tree to their friend’s,” that tells you something. If the answer is “I’m trying to make up for the fact that I’ve barely been home this month,” that tells you something too.

Naming the feeling doesn’t make the desire to buy vanish. What it does is give you a chance to decide whether money is the best way to respond. Sometimes it is. Sometimes you really do want to stretch a bit for something meaningful. A lot of the time, though, what you and the people you love actually need is time, attention, rest, or an honest conversation—not another package on the doorstep.

That’s where low-cost or no-cost alternatives become more than clichés. A movie night with real phones-off presence can land deeper than one more expensive gadget. A simple meal cooked with care can feel better than a reservation someone had to put on a card. A few hours of help—childcare, rides, job search support, showing someone how to navigate a system—can mean more than anything in a box.

You are allowed to meet emotional needs with emotional tools instead of financial ones.

Saying the Hard Things Out Loud

A lot of holiday overspending hides under silence. You don’t say what you can afford. You don’t say what you’re worried about. You don’t say that this year has taken more out of you than usual. You just nod along and hope you can figure it out.

There’s another option: saying something before everything is set in motion.

With extended family or friend groups, that might mean speaking up early. You can say, in plain English, that you’re keeping things simple to protect some financial goals and your sanity. You can suggest a name-draw instead of everyone buying for everyone. You can push for thoughtful, lower-cap gifts or shared experiences that don’t require anyone to go into the red.

With a partner, it probably means an actual sit-down, not a rushed exchange while one of you is half asleep. You lay everything out: what matters to each of you emotionally about the season, what the real numbers look like, what you’re both willing to say no to this time. You can make one simple rule: no big holiday purchase happens without both of you saying yes to it. That turns each swipe into something you’re doing together instead of something one person resents and the other defends.

When it comes to kids, you don’t have to dump your whole budget situation on them. But you also don’t have to pretend you live in a store ad. Age-appropriate honesty goes a long way: this year we’re focusing on fewer gifts and more time together; this year we’re being careful so we’re not stressed in January. That’s not “ruining the magic.” That’s modeling what it looks like to be responsible in a world that presses the gas pedal on spending and hands the bill to you later.

Boundaries are rarely comfortable at first. But they’re a lot less painful than carrying quiet resentment and loud debt.

When You’d Rather Skip the Whole Season

There’s one more reality that never makes it into the commercials: some people don’t want “more” from the holidays. They want out.

Maybe you’re grieving someone and the entire season feels like a reminder. Maybe family relationships are messy or unsafe. Maybe you’re dealing with depression or burnout so heavy that the idea of one more obligation feels like too much. Maybe the money situation is so tight that you can’t imagine enjoying anything while you’re this worried.

If that’s you, you’re not broken. You’re not “ruining it for everyone.” You’re human in a hard season trying to survive a culture that only knows how to sell joy at full volume.

You’re allowed to do less. Less decorating. Fewer events. Fewer people. You can build a smaller container that feels manageable: one person you see, one thing you attend, one ritual you keep, if any. You can step away from traditions that feel like obligations and toward ones that actually help you heal.

Sometimes the only thing you can give in a season like that is your honesty and a small dose of kindness—to yourself and to others. That might look like volunteering somewhere for a few hours, or sending a message to someone else who’s struggling, or just not spending money you don’t have to create a fake picture of everything being fine.

There is no single correct way to do this season. There is only the way that doesn’t destroy you.

Turning This Holiday Into a Pivot Point

Balancing emotions and money for the holidays is not a one-year project. It’s part of a bigger shift in how you carry your middle-class life in an economy that constantly invites you to live beyond your means and then blames you when the math doesn’t work.

You won’t get everything perfect this year. You’re not supposed to. But you can decide this is the last year you move through the season on autopilot.

One small step is to do a quiet debrief with yourself in January. No self-insults, no dramatics. You look at roughly how much you spent, how much of that landed on credit, what parts of the holiday genuinely fed your soul, and what parts just drained you. You write that down. Next fall, instead of starting from scratch or from other people’s expectations, you start from your own notes.

Another step is to treat next year’s holiday like the predictable event it is. You know it’s coming. That means you can build for it, even in small amounts. A little set aside each month into a labeled account adds up faster than you think. More important than the exact number is the habit: you stop treating December like an emergency and start treating it like something you prepare for, the same way you prepare for property taxes or back-to-school.

Underneath all of this is a bigger cultural shift you’re allowed to make inside your own family: you do not go into debt for the holidays anymore. You don’t have to put that slogan on a mug, but you can quietly build your choices around it. You can decide that your standard is thoughtful, grounded, sustainable—not impressive, not Instagram-approved, not designed to compete with people whose situations you don’t actually know.

Middle-class households keep a lot of this country running. You deserve a version of the holidays that doesn’t leave you wrecked emotionally or financially. You deserve a season where you can laugh without doing math in your head at the same time.

If you do nothing else this year, pick three things: one financial boundary you’re going to honor, one emotional boundary you’re going to set, and one act of kindness you’re going to offer that doesn’t require you to swipe a card. Build your holiday around those.

The commercials will still yell. The emails will still arrive. But you’ll be operating from a different place—one where your heart and your bank account are on the same team.

Senior Accounting & Finance Professional|Lifehacker|Amateur Oenophile

RELATED ARTICLES

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

Leave Comment

Cancel reply

Gig Economy

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

By FMC Editorial Team

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

By MacKenzy Pierre

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan to escape 25% APR debt.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

What To Do If You Get Fired With an Outstanding 401(k) Loan

Fired with a 401(k) loan? Avoid taxes, offsets, and deadline traps with this step-by-step checklist. Read now.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

The Real Math of Money in Relationships

Split finances without resentment. Any couple, any income ratio. Use the worksheet + rules—start today.

By Article Posted by Staff Contributor

American Middle Class / Feb 03, 2026

Investing or Paying Off the House?

Invest or pay off your mortgage? See a $500k example with today’s rates, dividends, and peace-of-mind math—then choose your plan.

By Article Posted by Staff Contributor

American Middle Class / Jan 30, 2026

Gold, Silver, or Bitcoin? Start With the Job—Not the Hype

Gold, silver or Bitcoin? Learn what each is for—and how to size it—before you buy. Read the framework.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Florida Homeowners Pay the Most in HOA Fees

Florida HOA fees are surging. See what lawmakers changed, what’s next, and how to protect your budget—read before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Why So Many Homebuyers Are Backing Out of Deals in 2026

Why buyers are backing out of home deals in 2026—and how to avoid costly surprises. Read the playbook before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 28, 2026

How Money Habits Form—and Why “Self-Control” Is the Wrong Villain

Learn how money habits form—and how to rewire spending and saving using behavioral science. Read the framework and start today.

By FMC Editorial Team

Latest Reviews

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs....

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market...

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan...