3-type of Credit Card Interest Rates

The estimated reading time for this post is 157 seconds

Credit card interest rates can be as high as 29 percent. The interest is often compounding daily on average credit card balance, making the debt grossly expensive to service.

The debt can get even costlier depending on the type of balance that the cardholders are carrying over to the next month. Balance transfers, purchases, and cash advances can have different annual percentage rates (APRs)

American consumers used part, if not all, of their direct payments from the government last year to pay off credit card debt.

However, it does seem that they revert to their old habit and start racking up more credit card debt. According to New York Federal Reserve, credit card balances increased by $17 billion last quarter. The average credit card debt of U.S. families is about $5,500.

3-type of Credit Card Interest Rates

Bank of America Unlimited cash Rewards Credit Card

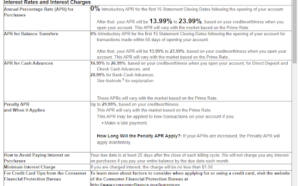

Balance Transfer APR– is the interest rate a cardholder will pay on the balances she transfers to a credit card once 0% introductory APR expires.

As the above Schumer Box shows, the Bank of America Unlimited cash Rewards Credit Card offers 0% introductory APR for the first 15 statement closing dates following the opening of the card, then its APR will be as high as 23.99%

Purchase APR is the interest rate a cardholder pays on purchases. If the cardholder does pay her to balance in full on or before the grace period or the due date, she pays no interests; otherwise, APR can be as high as 23.99%

Cash Advance APR is the interest rate a cardholder pays on liquid cash she withdraws from her credit card at a bank or ATM. Credit card cash advances often come with a fee and higher APR.

As the above Schumer Box shows, the cash advance APR can be as high as 28.99% on the Bank of America Unlimited cash Rewards Credit Card. Credit cardholders should strive to pay off their balance in full each month on or before the grace period. Those who have to maintain a balance on their credit card need to work on their credit profile and increase their credit score as high as possible to access the best credit card interest rates.

How Is Credit Card Interest Calculated

Whether it is cash advance or Purchase APR, credit card debt is expensive to service. Here’s how to calculate the actual cost of the debt for someone who is paying 23.99% and maintaining a daily balance of $1,800.

The daily rate is 0.000657 (0.2399/365). Now the APR is converted into a daily rate; it’s pretty simple to calculate the daily interest charge, which is $1.18 ($1,800 x 0.000657) or $431.82 ($1.18 x 365).

Some banks divide by 360 days rather than 365 days, but the difference will not be material. The higher is the cardholder’s daily balance, the more interest she will pay. Below is the quickest way to calculate the average daily balance:

Last statement balance

-payment

+posted transaction for each specific date

/# days in the billing cycle

The Bottom Line

Credit card interest rates tend to be higher than any loan. Moreover, balance transfers, purchases, and cash advances have different APRs, as high as 29.99 percent.

Pingback: 3 Best Everyday Credit Cards - Credit Cards

Pingback: Are You Money Smart? - Personal Finance