Gig Economy Jobs Explained: Pros, Cons, and Survival Tips

By Article Posted by Staff Contributor

The estimated reading time for this post is 812 seconds

Last updated

December 19, 2025 — Refreshed with the latest pay-rule debates, platform realities, and the “real hourly rate” math most gig workers skip.

Jump to a section

Key Takeaways

- Gig economy jobs are flexible, not stable. The app provides access—you provide the safety net.

- Gross pay lies. Your real earnings are what’s left after gas, wear-and-tear, downtime, and taxes.

- Taxes are the silent killer. If you’re 1099, plan now or April will punish you.

- Diversify or get trapped. One platform can change rules overnight. Multiple lanes protect your month.

- Policy and algorithms matter. Pay floors, worker-status fights, and app logic can change your pay fast.

Gig Economy Jobs Explained: Pros, Cons, and Survival Tips

Focus keyphrase: gig economy jobs

You don’t “discover” gig economy jobs. You end up there.

Usually after the mortgage payment jumps. Or the car insurance renews. Or your kid needs something right now and your checking account says, “Not today.”

That’s the gig economy in real life: not a lifestyle brand. A pressure valve.

And yes—gig work can help. But let’s not pretend it’s a magic trick. The flexibility is real. The stability is still your problem.

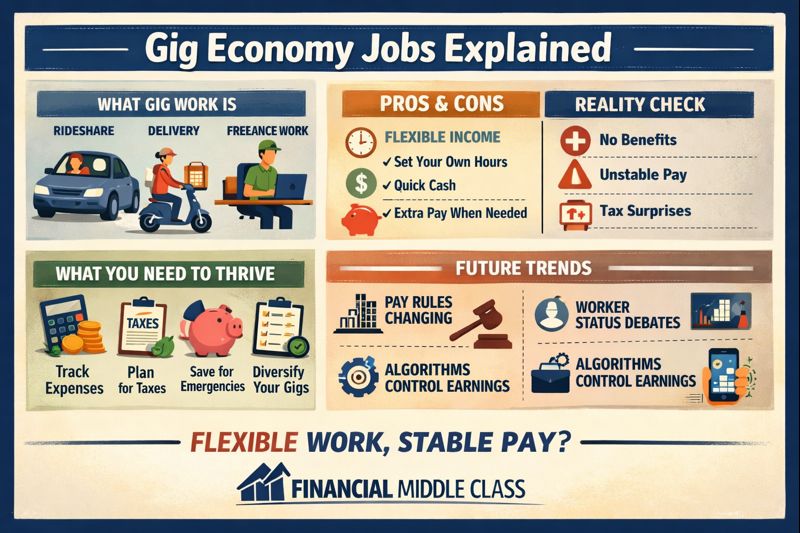

What the Gig Economy Is (Without the Hype)

The gig economy is paid work organized as short-term tasks instead of long-term employment. You take a job. You get paid. You repeat. Sometimes it’s app-based work. Sometimes it’s freelance clients. Sometimes it’s short-term W-2 work that looks “normal” until you realize it’s temporary.

Here’s the part that trips people up: different reports measure gig work differently. So the numbers can look confusing on purpose.

What the data says (and why it doesn’t always match your life)

The U.S. Bureau of Labor Statistics (BLS) reported 10.2% of workers were in “alternative employment arrangements” as their main job in 2023. That includes independent contractors, on-call work, temporary help, and contract company workers.

But ADP’s research captures something you already know: gig work is often not the main job—it’s the patch job. They found about 1 in 4 people did some gig work over the prior 12 months.

Translation: plenty of households touch gig work at some point during the year, even if nobody calls themselves “a gig worker” at Thanksgiving dinner.

Who a Gig Worker Really Is

A “gig worker” can mean three very different lives. And your strategy depends on which one you are.

1) Platform gig workers (app-based)

Rides, deliveries, errands. The app assigns tasks. The rules shift. Your rating matters. And you can get deactivated without a real conversation.

2) Freelancers (client-based)

Design, writing, tutoring, bookkeeping, marketing, IT support. You find clients, deliver work, invoice, and follow up. You learn quickly that “Net 30” is just a polite way of saying “we’ll see.”

3) Contingent workers (short-term W-2)

You’re technically employed, but the work is temporary. The “security” can be a mirage. One schedule change and your whole month moves.

All three share the same core truth: you’re carrying risk that employers used to carry.

Gig Economy Platforms: The Main Lanes People Actually Use

Not all gig economy jobs are created equal. They’re different lanes with different economics. If you treat them like they’re all the same, you’ll make bad choices with good intentions.

Rideshare and delivery

This is the loudest lane: Uber, Lyft, DoorDash, Instacart, Amazon Flex, and more.

The money flowing through these platforms is massive. DoorDash reported 8 million Dashers in 2024, earning over $18 billion total. Uber reported drivers and couriers earned $20.0 billion (including tips) in Q4 2024 alone.

But don’t confuse “big platform totals” with “stable household income.” Your net depends on gas prices, demand, tips, and what the algorithm decided about you this week.

Local task and service platforms

Taskrabbit, Thumbtack, Rover, Care.com—work that’s more “service business” than “app job.” It can pay better per task, but demand is inconsistent and your reputation is your currency.

Online freelancing marketplaces

Upwork, Fiverr, Freelancer, Toptal. This lane is less about driving and more about skills. Upwork’s research estimates freelancers generated $1.5 trillion in earnings in 2024.

This is where gig work can become a real independent career—if you treat it like one.

Asset sharing

Airbnb, Turo, and similar models. This can be powerful, but you’re not just earning—you’re risking an asset you need to last.

Gig Economy Pros and Cons (The Honest List)

Most people don’t join gig work because they love the grind. They join because the bills don’t care about your feelings.

Advantages: what gig economy jobs do well

Flexibility that fits real life. You can work around school pickup, a second job, or a rotating schedule. That’s not small.

Speed. When the alternator dies and your emergency fund is still “in progress,” quick cash matters.

A bridge, not a destination. Used right, gig income can help you catch up, pay debt down, and buy time.

A doorway to independence (for skilled work). Freelancing can turn into repeat clients, referrals, and eventually something that doesn’t depend on being “busy.”

Disadvantages: what gig work quietly dumps on you

Unpredictable pay. Your best week can be followed by a dead week. Incentives disappear. Demand shifts.

You pay the costs. All of them. Gas. Tires. Maintenance. Downtime. Supplies. Insurance gaps. This is the part people ignore—and then wonder why they’re exhausted with nothing to show for it.

Taxes can become a financial jump-scare. If you’re 1099, nobody is withholding for you. April doesn’t care that you “meant to” set money aside.

No built-in benefits. No paid leave. No employer retirement match. Often limited protection if something goes wrong on the job.

You can get cut off instantly. Deactivation isn’t a layoff with severance. It’s a locked door.

What You Need to Thrive in the Gig Economy (Not Just Survive)

If you want gig work to build stability instead of draining you, you have to treat it like what it is: a small business living inside your phone.

1) Know your real hourly rate (after expenses)

“$25 an hour” isn’t real if you’re burning $8–$10 an hour in gas, wear-and-tear, and downtime. Net pay feeds your household. Gross pay feeds your ego.

2) Separate gig money from life money

If gig deposits land in the same account as your mortgage auto-draft, you’ll never see what’s happening clearly. Middle-class money moves require clarity, not vibes.

3) Plan for taxes like an adult

If you’re 1099, assume you owe taxes. Period. If you don’t set aside money, you’re borrowing from the IRS—and the interest rate is panic.

4) Build your own benefits (because nobody is coming)

Emergency fund. Retirement contributions. Health coverage planning. Even small steps matter—because the gig economy doesn’t hand you a safety net. It hands you a login.

5) Don’t marry one platform

Apps change pay formulas. They change incentives. They change rules. If you rely on one platform like it’s a loyal employer, you’re trusting something that has no reason to be loyal.

6) Track what works and stop doing what doesn’t

What days pay best? What hours? What neighborhoods? What jobs leave you wiped out for pennies? This is the difference between “I do gigs” and “I run gigs.”

Gig Economy Companies and Apps People Actually Use

Here’s the quick map:

- Rideshare: Uber, Lyft

- Food delivery: DoorDash, Uber Eats, Grubhub

- Grocery delivery: Instacart, Shipt

- Packages/routes: Amazon Flex

- Tasks/services: Taskrabbit, Thumbtack

- Pet care: Rover

- Freelancing: Upwork, Fiverr, Freelancer, Toptal

- Asset sharing: Turo, Airbnb

And don’t ignore the second layer: mileage trackers, invoicing tools, tax estimators—because the hidden job of gig work is managing your own back office.

Trends Shaping the Future of the Gig Economy

This is where “flexible work” runs into power, policy, and the fact that platforms don’t like being told what to do.

Pay floor rules are spreading (and platforms are pushing back)

New York City implemented minimum pay rules for app-based delivery workers, with the minimum rate reported at $21.44/hour as of April 1, 2025.

But policy fights continue. Reuters reported Instacart sued NYC in December 2025 over laws tied to pay standards and tipping rules.

Worker status battles are still defining the industry

California’s Prop 22 remains a major reference point (with key legal rulings continuing to shape how app-based workers are classified). Meanwhile, the EU adopted a Platform Work Directive aimed at stronger worker protections and algorithm oversight.

Different places are answering the same question differently: are gig workers independent businesses—or employees without benefits? Your paycheck depends on that answer.

Algorithms are becoming the real boss

Pay isn’t just “what the job pays.” It’s how the platform distributes jobs, controls visibility, and makes decisions you can’t appeal. That’s not the future. That’s already happening.

Gig work is becoming permanent “second-income infrastructure”

That ADP “1 in 4 over a year” reality fits what middle-class households already know: gig work is becoming normal. Not glamorous. Normal.

So… Should You Do Gig Work?

Here’s the middle-class test.

If gig work helps you pay down high-interest debt, build an emergency fund, and stop living on overdraft adrenaline, it can be smart.

But if gig work keeps you busy without moving you forward—if it replaces rest with constant hustle and hides a budget that doesn’t fit the modern cost of living—it’s not freedom.

It’s a treadmill with a five-star rating system.

The Truth That Hits Home

The gig economy sells flexibility. And sometimes it delivers.

But the middle class isn’t starving for flexibility. We’re starving for stability—the kind where a dead car battery doesn’t turn into a debt spiral, where a slow week doesn’t threaten your rent, where your life doesn’t depend on an app update.

Gig work can be a bridge. It can even become a business.

But if you don’t build the guardrails—expenses, taxes, savings, benefits—then gig work doesn’t give you control.

It just gives your stress a schedule.

Timeline: How Gig Work Got Here (Quick Reality Map)

Click to expand each chapter. No plugins required.

2009–2014: The “app era” turns spare time into paid tasks

2015–2019: Gig work becomes mainstream side income

2020–2022: Demand spikes, then normalizes

2023–2025: Pay rules, classification fights, and algorithms move center stage

FAQ: Gig Economy Jobs

Are gig economy jobs worth it for middle-class households?

What’s the biggest mistake new gig workers make?

How should gig workers handle taxes?

Is it better to use one platform or multiple?

Can gig work turn into a real business?

Quick question for you

If you’ve done gig work, what surprised you the most: the taxes, the expenses, or how fast the pay can change week to week?

Drop your experience in the comments—your answer might save somebody else a painful lesson.

RELATED ARTICLES

High-Yield Savings Accounts: A Safer Home for Your Cash

A high-yield savings account can pay several times the national savings rate while keeping qualified deposits federally insured. Here is how it works, what to watch for, and where it belongs in your financial life.

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

Leave Comment

Cancel reply

Gig Economy

Personal Finance / Aug 01, 2026

Cash Strategy: Put Every Dollar in the Right Place

Your checking account, emergency fund, short-term savings, and investments should not be managed the same way. This cash strategy helps assign every dollar to the right...

By Article Posted by Staff Contributor

Personal Finance / Aug 01, 2026

Best HYSA: How to Choose Beyond the Highest APY

A competitive interest rate matters, but it is only one part of choosing a high-yield savings account. Compare insurance, fees, access, transfer speed, and promotional conditions.

By Article Posted by Staff Contributor

Personal Finance / Aug 01, 2026

High-Yield Savings vs. CDs, Treasury Bills, and Other Safe Places for Cash

High-yield savings accounts are excellent for accessible cash, but they are not always the best choice. Compare HYSAs, CDs, Treasury bills, money market accounts, and I...

By Article Posted by Staff Contributor

American Middle Class / Aug 01, 2026

High-Yield Savings Accounts: A Safer Home for Your Cash

A high-yield savings account can pay several times the national savings rate while keeping qualified deposits federally insured. Here is how it works, what to watch...

By Article Posted by Staff Contributor

Real Estate / Jul 30, 2026

Mortgage Lock-In Is Freezing the Housing Market

Millions are trapped by 3% mortgages. Learn how mortgage lock-in worsens affordability—and why homeowners are renovating instead.

By FMC Editorial Team

Real Estate / Jul 26, 2026

Is South Florida More Expensive Than New York? The Complete 2026 Relocation Guide

Is South Florida more expensive than New York? Compare housing, taxes, insurance and 104 municipalities before you move.

By Article Posted by Staff Contributor

Personal Finance / Jul 25, 2026

The Time Value of Life Experiences: What Compound Interest Leaves Out,

Money compounds, but life experiences do too. Explore what compound interest leaves out—and how to balance saving with living.

By MacKenzy Pierre

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

By FMC Editorial Team

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

By MacKenzy Pierre

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan to escape 25% APR debt.

By Article Posted by Staff Contributor

Latest Reviews

Personal Finance / Aug 01, 2026

Cash Strategy: Put Every Dollar in the Right Place

Your checking account, emergency fund, short-term savings, and investments should not be managed the same...

Personal Finance / Aug 01, 2026

Best HYSA: How to Choose Beyond the Highest APY

A competitive interest rate matters, but it is only one part of choosing a high-yield...

Personal Finance / Aug 01, 2026

High-Yield Savings vs. CDs, Treasury Bills, and Other Safe Places for Cash

High-yield savings accounts are excellent for accessible cash, but they are not always the best...