Student Loan Garnishment 2026: Default vs Delinquent

By FMC Editorial Team

The estimated reading time for this post is 966 seconds

If you’ve been living with student loans in the background—paying sometimes, ignoring sometimes, promising yourself you’ll “handle it after the holidays”—2026 is the year that stops being cute.

Two things are happening at the same time.

First, collections are ramping back up for borrowers already in trouble, including wage garnishment notices starting the week of January 7, 2026 (about 1,000 borrowers in the first wave, with more to follow).

Second, a major repayment overhaul begins July 2026 that reshapes repayment plans and future borrowing.

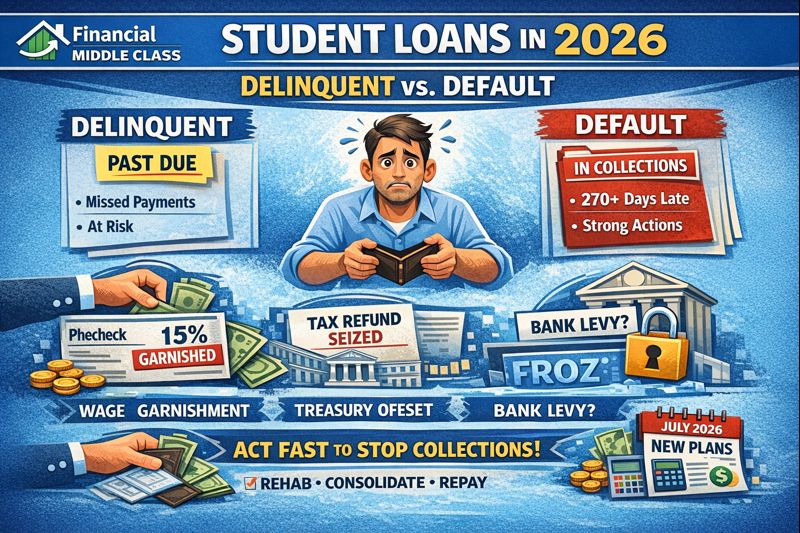

And here’s the part most people keep messing up online: being past due (delinquent) is not the same thing as being in default. Those words are not synonyms. In the federal system, that difference is the line between “you’re behind” and “they can start pulling levers you didn’t even know existed.”

So let’s get you clear, calm, and moving.

Start here: delinquent vs default (this is the whole ballgame)

For most federal student loans, default is triggered when you’re 270+ days past due. That’s roughly nine months of missed payments. Delinquency is what happens before that—missed payments, late fees, “past due” status, and a growing mess—without the government’s strongest collection tools fully kicking in.

Here’s the cleanest way to think about it:

| Delinquent (past due) | Default (the “collections switch” flips) |

|---|---|

| You missed a payment and haven’t fixed it yet. You’re behind, but you’re not at the “enforcement” stage. | For most federal loans, you’ve missed payments long enough to hit the default trigger (typically 270+ days). |

| You still have more room to cure the problem quietly: catch up, change plans, request relief, get current. | The government gets collection powers that can include administrative wage garnishment and Treasury offset. |

| You’re usually dealing with your servicer and standard repayment options. | You may be dealing with the Default Resolution Group and tools like AWG and TOP get real. |

The 2026 student-loan year in one sentence

January 2026 is about collections resuming; July 2026 is about the new repayment architecture.

If you only remember one thing, remember that.

A timeline you can actually follow

| What’s happening | When | Who feels it first | Why it matters |

|---|---|---|---|

| Wage garnishment notices begin rolling out (first wave ~1,000 borrowers) | Week of Jan. 7, 2026 | Borrowers already in default | This is the “collections are not theoretical anymore” moment. |

| Ongoing collections tools expand month-to-month | 2026 (rolling) | Defaulted borrowers and seriously delinquent borrowers moving toward default | The system is reactivating enforcement and pressure. |

| New repayment system begins rolling out (Standard + RAP) | July 2026 | New borrowers; some existing borrowers transitioning over time | Repayment options get simplified, and for many people, less generous. |

| Parent PLUS borrowing caps apply to new Parent PLUS loans | July 1, 2026 | Families financing college with Parent PLUS | Middle-class families get squeezed hardest. |

| Grad PLUS eliminated; new caps for grad/professional borrowing | Starts in the overhaul window | Grad and professional students | Less federal access means more private-loan temptation (and risk). |

Now let’s talk about what everybody is really afraid of: paychecks and bank accounts.

What the government can actually do (and what people think it can do)

When people say “they’re going to take my money,” they’re usually mixing up three different things:

- Administrative Wage Garnishment (AWG): paycheck withholding without going to court (federal loans in default).

- Treasury Offset Program (TOP): withholding certain federal payments (like tax refunds) to pay a federal debt.

- Bank levy: a court-driven move more common with private debts after a judgment (and the IRS for taxes), not the typical federal student-loan playbook.

Here’s the straight translation:

| Tool | What it hits | Do they need a court judgment? | When it usually becomes possible |

|---|---|---|---|

| AWG (wage garnishment) | Your paycheck (your employer withholds a portion) | No for defaulted federal student loans | Usually at/after default |

| TOP (Treasury offset) | Federal payments like tax refunds, some benefits | No; there is a required notice process | Usually at/after default |

| Bank levy (true levy) | Your bank account (freeze/seize funds) | Typically yes via court judgment for private loans | Usually after lawsuit → judgment |

If you’ve heard “bank levy” in the federal-loan context, what they often mean is Treasury offset—money getting intercepted before it ever reaches you, especially via a tax refund. That’s not the same as your checking account being frozen like a courtroom drama.

Wage garnishment in 2026: the paycheck reality check

The Department of Education has said the first wave of wage garnishment notices is expected to go out the week of January 7, 2026. Those notices are the moment you stop arguing with your own calendar and start responding to official paper.

For defaulted federal student loans, the government can order your employer to withhold up to 15% of your disposable pay through administrative wage garnishment. “Disposable pay” is what’s left after required deductions—not what’s left after your rent, your car note, and your kid’s braces. That’s why garnishment feels like a surprise attack: the math doesn’t care that you were already on the ropes.

And before you ask: no, you don’t have to be rich for this to hurt. Garnishment doesn’t scale down based on your feelings. It scales down based on rules.

The Department of Labor also notes that federal law authorizes this up to-15% garnishment for defaulted debts owed to the U.S. government (including defaulted federal student loans).

The “bank levy” myth: what’s real is Treasury offset

What’s more common than a “bank levy” for federal student loans is Treasury offset.

TOP is basically the government saying: “Before we pay you, we’re paying us.” Treasury describes TOP as a program that collects delinquent federal debts by offsetting federal payments, and it requires agencies to provide notice and due-process steps, including a letter at least 60 days before the debt is referred for offset.

Federal Student Aid’s default-and-collections guidance also describes TOP as withholding tax refunds or certain federal benefits, and it outlines timelines tied to notices—including a window where taking action can prevent offset and garnishment if you move quickly.

So if you’re sitting there thinking, “They’re going to drain my checking account,” pause. For federal loans, the most common “seizure” people experience is interception—refunds and eligible federal payments getting captured upstream.

Private student loans: why the rules get harsher (and more court-like)

Now, private loans are a different beast. A private loan collector generally can’t garnish your wages without a court order, and they can’t do federal-style offsets the way the government can. That means the road to wage garnishment (or a true bank levy) usually runs through lawsuit territory.

So if your debt is private and you get actual court paperwork, this is not the time to “manifest” your way out of it. Ignoring court mail is how people turn a bad debt into a locked bank account.

Who gets hit first in 2026 (find yourself before you spiral)

If you’re delinquent but not defaulted, your mission is prevention: you want to stay out of default so you never see the heavy tools at all.

If you’re already in default, your mission is interruption: you want to stop involuntary collections and get back into a sustainable status.

If you’re a Parent PLUS borrower or the parent of a rising college student, your mission is planning: July 2026 changes will squeeze families who don’t qualify for big need-based aid but also don’t have cash lying around.

If you have private loans, your mission is risk management: you want to reduce legal exposure and negotiate before it becomes a judgment.

How to check your status in five minutes (because guessing costs money)

You don’t need a motivational speech—you need certainty.

If your loans are federal, StudentAid.gov is the hub, and when federal loans are in default, Federal Student Aid also points borrowers to MyEdDebt.ed.gov, the official site used for defaulted federal loans being handled through the Default Resolution Group.

If you’re not sure what you have, the fastest mental shortcut is this: if your loan can be “in TOP” or “in AWG,” you’re in federal-default territory. Federal Student Aid even translates those statuses plainly: “Certified for TOP” is the Treasury offset pathway, and “Account is in AWG” is administrative wage garnishment.

And if you’re holding private loans, pull your credit reports and look for the lender/servicer trail—because private collection often changes hands, and confusion is how people pay the wrong party.

Notice-letter decoder: translate the scary language into action

Most borrowers don’t ignore student loans because they’re irresponsible. They ignore them because the letters sound like they were written by a robot that hates you.

Here’s the translation table:

| What the notice says | What it usually means | What you do next |

|---|---|---|

| “Notice of intent to garnish” | AWG is on the table if you don’t act | Treat it like a deadline. Federal guidance ties avoidance windows to moving fast after notice. |

| “Certified for TOP” | Refunds/eligible federal payments can be intercepted | You need to resolve or enter an agreement before offsets hit. |

| “Account is in AWG” | Your employer can be ordered to withhold up to 15% disposable pay | You’re in enforcement territory; act immediately. |

| “Default Resolution Group” | You’re in federal-default servicing | Your path is rehab, consolidation, or a repayment agreement. |

The money math: what garnishment does to a real middle-class budget

Let’s make this tangible, because “15% of disposable pay” sounds manageable until it’s eating your grocery money.

Imagine two households. These aren’t perfect numbers—they’re realistic enough to feel the pain.

| Household A: single renter | Household B: family with kids | |

|---|---|---|

| Gross pay (annual) | $55,000 | $85,000 |

| Gross pay (monthly) | ~$4,583 | ~$7,083 |

| Disposable pay (monthly, after required deductions—rough example) | ~$3,500 | ~$5,300 |

| AWG estimate (15% of disposable pay) | ~$525/month | ~$795/month |

| What that breaks in real life | A utility bill + groceries, or car insurance + meds | Childcare gap, grocery gap, or mortgage cushion |

That’s why “I’ll deal with it later” doesn’t work when you’re in default. Later becomes payroll.

Credit impacts: the part that follows you around quietly

Default doesn’t just take money. It takes options.

Federal Student Aid warns that if action isn’t taken within certain windows, defaulted loans can be reported to major credit bureaus, and the record of default can remain for years—though rehabilitation has a specific benefit: after completing the required rehab payments, ED requests removal of the default record, even if the earlier late-payment history remains.

Translation: if you’re trying to rent a better apartment, finance a car without getting cooked on the rate, or qualify for a mortgage, letting default sit is like walking around with a weight vest you didn’t choose.

What actually works: pick the lane you’re in

If you’re delinquent but not default

Your best move is boring and powerful: get into a payment you can actually keep. You’re trying to avoid crossing the default line where wage garnishment and Treasury offset become much more likely.

This is also where you stay alert to the shifting repayment landscape. The overhaul is pushing toward fewer repayment options over time, with changes beginning in 2026 and additional transitions for existing borrowers through 2028. If you can lock in stability now, you’re not scrambling later.

If you’re in default and staring at collections

Federal Student Aid lays out the practical exits: you can pursue rehabilitation, consolidation, or a repayment agreement, each with different trade-offs.

Here’s the comparison you actually need:

| Rehabilitation | Consolidation | Repayment agreement | |

|---|---|---|---|

| What it does | Gets you out of default after a series of on-time payments | Replaces the defaulted loan with a new loan | Starts paying under an agreement to stop enforcement |

| Biggest upside | Can remove the default record after completing rehab | Can be faster to get out of default status | Can stop the bleeding quickly if you start payments fast |

| Biggest trade-off | Takes time and consistency | Default history can remain on credit | Doesn’t erase default by itself; it’s a management tool |

| Why FMC readers like it | It’s the “repair my record” path | It’s the “speed” path | It’s the “stop the hammer” path |

And here’s the non-negotiable point: the sooner you move after a notice, the more control you have. Federal Student Aid explicitly ties avoidance of offset and garnishment to making the first payment within the notice windows it describes.

If your loans are private and you’re behind

Private collectors generally need a court judgment to garnish wages. That means your priority is to respond early, document everything, and treat legal notices like emergencies—not spam.

Your next 72 hours (triage without panic)

In the next three days, your goal is to replace fear with facts. You confirm whether your loans are federal or private, and you identify whether you’re delinquent or default. If you’re in default, you look for signs you’re headed toward AWG or TOP—language like “Certified for TOP” or “Account is in AWG” is not decorative.

You also gather the basics you’ll need to make any plan stick: income proof, household obligations, and your real monthly margin. Not the “I could cut back” margin—the real one.

And you respond to any notice like it’s a work deadline, because it is. The government’s process includes notice steps, but the point of notice is not to comfort you. It’s to start the clock.

Your next 30 days (stability, not perfection)

Over the next month, you’re trying to get to one place: a payment status you can maintain. That might mean formal rehab or consolidation if you’re in default, or it might mean switching into a sustainable repayment structure if you’re delinquent but still above water. The win is not “pay it off.” The win is “stop the enforcement and stop the damage.”

If you’re in default, you also track credit reporting risks. Federal Student Aid notes how default can show up on credit reports and how different resolution paths affect that record. That’s not vanity. That’s future housing and future borrowing.

Scam-proofing: 2026 is prime season for people trying to rob you

Anytime repayment rules change, scammers show up like it’s Black Friday.

Federal Student Aid warns that scammers often promise immediate forgiveness and charge upfront or monthly fees, and it points borrowers to official channels. The FTC also warns not to pay upfront for student-loan debt relief and not to share sensitive login info with random callers or texts.

If someone contacts you and says they can “unlock” a plan for a fee, understand what’s happening: they’re trying to get paid for forms you can submit through official sites.

July 2026: the repayment overhaul that changes the future (even if your problem is “right now”)

Starting in July 2026, the system moves toward two core repayment choices: a revised standard plan and a new income-based plan called the Repayment Assistance Plan (RAP).

RAP is described as an income-based option with payments set at 1%–10% of income (AGI) with a minimum $10 payment and forgiveness after 30 years. The standard plan sets fixed payments over 10–25 years based on original balance, and Investopedia lists the balance bands (10 years under $25k; 15 years for $25k–$49,999; 20 years for $50k–$99,999; 25 years for $100k+).

Here’s the side-by-side you’ll want bookmarked:

| New Standard Plan | RAP (Repayment Assistance Plan) | |

|---|---|---|

| Payment style | Fixed | Income-based (AGI-based) |

| Term | 10–25 years depending on balance | Up to 30 years to forgiveness |

| Who it tends to help | People who want certainty and can handle fixed payments | People who need income flexibility (but it’s less generous than prior systems) |

| Floor | Not an income floor; it’s balance-based | Minimum monthly payment is $10 |

At the same time, new borrowing constraints hit families. Parent PLUS loans taken out after July 1, 2026 are capped (reported as $20,000 per year and $65,000 per child) and Parent PLUS borrowers with new loans are not eligible for RAP in the reporting around the overhaul.

The overhaul also eliminates Grad PLUS and implements new borrowing caps for grad and professional programs.

If you’re a parent or a grad borrower, this is the part of the article you read twice—because it changes how families finance school.

Two case studies (because middle-class life is not a spreadsheet)

Case study #1: The “I’m only behind” borrower who waits too long.

Marcus is 34, makes $62,000, and missed payments during a rough year. At first he’s delinquent, telling himself he’ll catch up after he gets through car repairs and a rent increase. The problem is time doesn’t stop. Once delinquency stretches and he crosses into default territory, the tone of his mailbox changes. Now he’s not negotiating; he’s responding. When the system shifts into enforcement mode, he’s facing the possibility of AWG—money taken from his paycheck before he can decide which bill “wins” this month. That’s why the best time to act was when he was embarrassed, not when he was scared. Default is where fear gets expensive.

Case study #2: The Parent PLUS trap that hits “responsible” families.

Denise is 52, household income is decent, and she’s helping her daughter start college. She doesn’t qualify for much need-based aid, and she doesn’t have $25,000 a year in spare cash either—because she’s also saving for retirement and paying Florida insurance premiums like they’re a second mortgage. The July 2026 Parent PLUS cap changes the math for families like hers, limiting how much federal Parent PLUS can cover and potentially pushing families toward private loans with harsher enforcement rules if things go bad. Denise’s real “student loan plan” isn’t just repayment; it’s financing decisions that don’t blow up her 60s.

FAQs (the questions people type when they’re stressed)

Can they garnish me if I’m only delinquent?

In general, the heavy tools like administrative wage garnishment are associated with defaulted federal loans, not early-stage delinquency. The default line (typically 270+ days past due for most federal loans) is the key threshold.

Is Treasury offset the same thing as a bank levy?

No. Treasury offset is the government intercepting certain federal payments to collect a delinquent federal debt, with required notice steps. A bank levy is usually a court-driven process (more common with private debts after judgment).

Do private lenders need a court order to garnish wages?

A private student loan collector generally may not garnish wages without a court order.

What’s the big change in July 2026?

The system begins shifting to a revised standard plan (10–25 years by balance) and a new income-based RAP plan (1%–10% of AGI, minimum $10, forgiveness after 30 years), with borrowing cap changes for Parent PLUS and graduate/professional loans.

The FMC bottom line

2026 is not a year to “see what happens.” For a lot of borrowers, what happens is payroll.

If you’re delinquent, your power move is staying out of default—because the strongest seizure tools usually live on the other side of that line. If you’re already in default, your power move is interrupting enforcement and choosing your exit path before the system chooses one for you. And if you’re a family planning college financing, July 2026 is the new era—same dream, different rules, tighter caps.

No shame. Just strategy. The middle class doesn’t need lectures—we need leverage.

RELATED ARTICLES

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

Leave Comment

Cancel reply

Gig Economy

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

By FMC Editorial Team

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

By MacKenzy Pierre

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan to escape 25% APR debt.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

What To Do If You Get Fired With an Outstanding 401(k) Loan

Fired with a 401(k) loan? Avoid taxes, offsets, and deadline traps with this step-by-step checklist. Read now.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

The Real Math of Money in Relationships

Split finances without resentment. Any couple, any income ratio. Use the worksheet + rules—start today.

By Article Posted by Staff Contributor

American Middle Class / Feb 03, 2026

Investing or Paying Off the House?

Invest or pay off your mortgage? See a $500k example with today’s rates, dividends, and peace-of-mind math—then choose your plan.

By Article Posted by Staff Contributor

American Middle Class / Jan 30, 2026

Gold, Silver, or Bitcoin? Start With the Job—Not the Hype

Gold, silver or Bitcoin? Learn what each is for—and how to size it—before you buy. Read the framework.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Florida Homeowners Pay the Most in HOA Fees

Florida HOA fees are surging. See what lawmakers changed, what’s next, and how to protect your budget—read before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Why So Many Homebuyers Are Backing Out of Deals in 2026

Why buyers are backing out of home deals in 2026—and how to avoid costly surprises. Read the playbook before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 28, 2026

How Money Habits Form—and Why “Self-Control” Is the Wrong Villain

Learn how money habits form—and how to rewire spending and saving using behavioral science. Read the framework and start today.

By FMC Editorial Team

Latest Reviews

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs....

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market...

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan...