Humanoid Is Coming for Your Middle-Class Job

By FMC Editorial Team

The estimated reading time for this post is 679 seconds

On a factory floor in the American South, the work still looks familiar: carts, racks, bins of parts staged like a diner’s mise en place—everything in reach, everything timed. The people move with the quiet speed you only get after months of repetition: bend, lift, scan, place, repeat. A job like this doesn’t make you famous. It makes you solvent. It pays for the truck and the orthodontist, and it comes with the kind of health insurance that turns a broken wrist from a financial crisis into an inconvenience.

And now, in the same ecosystem—warehouse aisles, logistics hubs, assembly lines—something new is walking in.

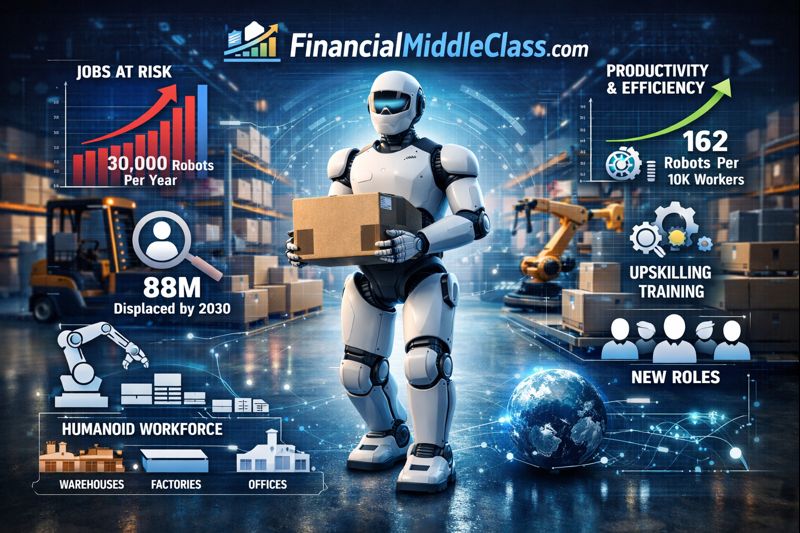

Not a fixed robotic arm behind a cage. Not a conveyor that never complains. A humanoid machine with legs, hands, and sensors, designed to operate in spaces built for people. At CES in early January 2026, Hyundai and Boston Dynamics unveiled Atlas in a public demonstration, and Reuters reported Hyundai plans to deploy Atlas at its Georgia manufacturing plant beginning in 2028, with tasks expanding in complexity by 2030. The company’s ambition isn’t subtle: a factory capable of producing 30,000 humanoid robots annually by 2028, part of a broader push into what Hyundai described as “physical AI.”

If you’re middle class—and your paycheck depends on work that is steady, repeatable, and performed in a structured environment—you don’t need to be a futurist to feel the pressure. You just need to have lived through one round of “efficiency” initiatives. The language is always calming. The outcome rarely is.

The shift is not “jobs.” It’s tasks—and that distinction matters.

The popular story about automation comes in two dramatic acts: first, the demo; then, the layoff. Real life is slower and more incremental. Work gets unbundled. Tasks get reassigned. Metrics tighten. The hiring ladder narrows. Overtime disappears. A role that used to be a full-time living becomes two part-time schedules stitched together by anxiety.

This is why the most accurate headline is not that humanoids are coming for your job. They’re coming for the portions of your job that can be turned into a repeatable sequence—especially the parts that are physically demanding, injury-prone, and easy to count.

It’s also why the humanoid form matters. Traditional industrial robots are extraordinarily productive, but they often require purpose-built cells, reconfigured lines, and controlled environments. Humanoids are a different bet: rather than redesigning the building for the machine, build the machine that can move through the building. They’re meant to climb the last mile of automation—into existing warehouses, stockrooms, and plants where the world is messy and the labor is human-shaped.

The pilots are no longer hypothetical

A useful way to separate hype from reality is to look for the places where companies are willing to attach their names to deployments—because reputational risk is real, and because “we tried it on our floor” is a stronger claim than “we posted a video.”

In logistics, Agility Robotics says Digit became the first humanoid deployed in commercial operations at a GXO facility near Atlanta, framing it as a “robots-as-a-service” milestone. The company later highlighted operational progress at the same deployment, including a milestone of 100,000 totes moved—an impressive number, but also one that should be read as company-reported performance rather than independently audited productivity data.

In auto manufacturing, BMW confirmed it conducted a successful test with Figure’s humanoid robots at its Spartanburg plant, while emphasizing there were no Figure robots currently deployed there and no set timetable for bringing them into ongoing operations. Figure, for its part, later published its own account of an 11-month deployment at Spartanburg, claiming “full deployment” on an active assembly line and citing figures like parts loaded and hours run—again, informative, but coming from the vendor and not a regulator or third-party evaluator.

Meanwhile, Mercedes-Benz entered a commercial agreement with Apptronik to pilot the Apollo humanoid robot in manufacturing facilities, with early focus on internal logistics such as delivering kits to the line.

The common thread is not that humanoids can do everything. It’s that they can do enough—reliably enough in bounded tasks—that major employers are willing to let them into production-adjacent environments.

And then there is Hyundai, which is placing a public, dated marker on the calendar: Atlas at the Georgia plant starting in 2028, with staged expansion toward more complex work by 2030.

The middle class is where the economy stores its repeatability

In American politics, “the middle class” is a sacred phrase and a vague one. In economic terms, it often maps onto a set of jobs that share an overlooked feature: they are stable precisely because they are repeatable. They occur within systems—distribution networks, compliance rules, production schedules—that can be measured and optimized.

That stability has always come with a bargain: you trade some autonomy for reliability. You show up, follow the process, hit the numbers, and in return you get a paycheck that doesn’t depend on vibes or venture capital.

Automation rewrites that bargain not through villainy, but through arithmetic.

The International Federation of Robotics reports that global robot adoption in manufacturing continues to accelerate: the global average robot density reached a record 162 units per 10,000 employees in 2023. IFR’s World Robotics 2025 statistics also report 542,000 industrial robots installed in 2024—annual installations topping 500,000 for the fourth straight year.

Humanoids arrive on top of this. They are not replacing the industrial robot; they’re meant to fill the gaps: the “in-between” work that is too variable for a fixed arm and too physical to ignore.

For the middle class, the risk isn’t only job loss. It’s job quality. When a company can credibly automate a meaningful chunk of tasks, it changes wage negotiations and staffing norms even if headcount stays flat for a time. It becomes easier to demand more output per worker. Easier to run lean. Easier to frame overtime as optional rather than necessary. Easier to let vacancies linger.

And that’s before we get to the part that hurts most over time: the ladder.

The ladder is the point

One under-discussed function of middle-class jobs—especially in operations-heavy sectors—is that they create a pathway. Entry-level roles teach the system. Supervisors and leads come from the floor. Skills are informal but real: the ability to spot a problem early, keep a line running, calm a bottleneck, coach a new hire, avoid an injury.

When the entry-level rung shrinks, the pipeline does too. In the long run, that can hollow out internal promotion and force workers into a more brittle labor market where experience is demanded but fewer employers are willing to pay to develop it.

This is why debates about automation often miss the texture of how a community changes. The factory may remain. The building still has shifts. The tax base might hold. But fewer people get their first shot at stability. The jobs that remain become either higher-skilled (maintenance, systems, QA) or more precarious (temp labor, irregular scheduling, “peak season” work). The middle compresses.

The pro-robot case is stronger than critics like to admit

It would be comforting if humanoids were merely corporate theater. It would also be inaccurate.

Companies have serious reasons to pursue them. Workplace injuries are costly and common in physically demanding environments; repetitive lifting and awkward motions wear down bodies and careers. Robots can be deployed to reduce strain. Hyundai, for example, has emphasized “high-risk and repetitive” tasks and described robots as a way to mitigate physical strain on workers.

There is also the competitiveness argument: if global rivals are adopting physical AI and automation, the logic goes, the U.S. cannot afford to romanticize labor-intensive processes—especially in manufacturing and logistics, where margins are thin and speed is king. Robot density data already reflects an international race.

And then there’s the simplest reason: labor markets are inconsistent. Turnover in warehousing and line work can be punishing. A machine that can do the least desirable tasks may stabilize operations and reduce burnout.

A fair reading of the pro-automation position is that it aims to keep production domestic, increase output, and reduce injuries—while shifting human work toward supervision, quality, and maintenance.

Some of this can even be true simultaneously.

The anti-robot case is not nostalgia. It’s bargaining power.

Critics don’t have to argue that robots are evil. They only have to point out that productivity gains do not automatically translate into shared prosperity. The U.S. has a long record of rising productivity with uneven wage growth, especially for non-college workers. Humanoids threaten to intensify that imbalance by putting pressure on the wage premium that comes from being necessary.

They also raise a political problem: if the middle class is partly defined by stable, benefits-based work, and if the economy shifts toward a smaller number of high-skill roles plus a larger number of contingent roles, then “middle-class politics” becomes harder to sustain. People feel it first as stress—then as cynicism.

And the labor impact won’t be confined to physical industries. The parallel story is already unfolding in services and finance, where AI tools can automate parts of compliance, documentation, and middle-office processes. In late December 2025, the Financial Times reported a Morgan Stanley forecast warning AI and digitalization could put more than 200,000 European banking jobs at risk by 2030—roughly 10% of the sector’s workforce—with vulnerability concentrated in back- and middle-office functions.

Different regions, same mechanism: once “routine cognitive work” becomes automatable, organizations restructure around exceptions and oversight—and they need fewer people to do the baseline tasks.

What we still don’t know

The most seductive thing about humanoid demos is how quickly they turn uncertainty into inevitability. But three uncertainties are huge.

Reliability and dexterity. Even optimistic coverage of Atlas notes limits around dexterity and scalability, and AP reported the CES demo involved remote control, with autonomy framed as a future iteration.

Economics. The question isn’t whether a humanoid can lift and carry. It’s whether it can do so cheaply enough, safely enough, and with low enough downtime that a CFO sees a stable return over years.

Adoption speed. Announced timelines are not the same as widespread deployment. Hyundai’s plan is notable precisely because it is dated and specific—but the jump from pilots to ubiquity is where many technologies slow down.

These uncertainties matter because they determine whether humanoids become a niche tool—like specialized robotics in certain facilities—or a general-purpose platform that spreads broadly.

The political choice hiding inside the technology story

Humanoids are often framed as an engineering problem. They are also a governance problem.

If physical AI raises productivity, the question becomes: who captures the value? If it reduces injuries, who benefits? If it shrinks the entry-level ladder, what replaces it?

A policy response doesn’t require a single grand bill. It requires a set of choices that shape incentives:

- Training tied to credentials and wage progression, not just “upskilling” as a slogan.

- Labor standards that keep safety and scheduling from becoming the adjustment valve when management runs lean.

- Tax and investment rules that don’t accidentally subsidize automation while underfunding human capital.

- Competition policy that prevents a handful of platform firms from capturing disproportionate gains from AI-robot ecosystems.

- Public procurement standards that reward deployments that demonstrably reduce injuries and create advancement pathways, rather than simply shrinking headcount.

These are political decisions because they determine whether automation expands the middle class—or turns it into a smaller island surrounded by precarious work.

The household strategy, minus the clichés

For a worker, the goal is not to “fight the robots.” It is to move closer to the tasks that remain scarce.

In practice, that means shifting from repeatability to responsibility. From doing the routine to managing the exceptions. From manual throughput to systems understanding.

The most durable roles in an automated environment tend to share traits: they involve safety judgment, troubleshooting, coordination across teams, quality validation, maintenance, training, and accountability when something goes wrong.

This is also why “learn to code” was never adequate advice. Most people don’t need to become software engineers. They need to become the person who can keep an automated system producing value on a Tuesday when something breaks and the metrics don’t care.

If you work in warehousing or manufacturing, that could mean gravitating toward maintenance support, QA, safety, inventory control, line lead roles, or any position that interfaces between operations and technology. If you work in an office-heavy industry, it may mean moving toward review, risk interpretation, client handling, and exception processing—the places where judgment and accountability remain hard to automate.

It’s not glamorous. That’s also the point.

The new middle-class question

For decades, American leaders have treated the middle class as a moral category: the people who work hard and deserve stability. Humanoid robots force a more practical question: what, exactly, produces stability in an economy that is learning to do more with fewer people?

The answer won’t be found in a demo video. It will be found in whether the gains from automation translate into broader wage growth, safer work, and intact ladders—or whether they concentrate into profits, higher output, and thinner staffing.

Hyundai’s plan to deploy Atlas in Georgia beginning in 2028 is a signal that the era of “humanoids are a gimmick” is ending. The era of “humanoids are a governance issue” is beginning.

And the middle class—whose lives are built on the reliability of systems—will be among the first to feel which direction we chose.

RELATED ARTICLES

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

Leave Comment

Cancel reply

Gig Economy

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

By FMC Editorial Team

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

By MacKenzy Pierre

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan to escape 25% APR debt.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

What To Do If You Get Fired With an Outstanding 401(k) Loan

Fired with a 401(k) loan? Avoid taxes, offsets, and deadline traps with this step-by-step checklist. Read now.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

The Real Math of Money in Relationships

Split finances without resentment. Any couple, any income ratio. Use the worksheet + rules—start today.

By Article Posted by Staff Contributor

American Middle Class / Feb 03, 2026

Investing or Paying Off the House?

Invest or pay off your mortgage? See a $500k example with today’s rates, dividends, and peace-of-mind math—then choose your plan.

By Article Posted by Staff Contributor

American Middle Class / Jan 30, 2026

Gold, Silver, or Bitcoin? Start With the Job—Not the Hype

Gold, silver or Bitcoin? Learn what each is for—and how to size it—before you buy. Read the framework.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Florida Homeowners Pay the Most in HOA Fees

Florida HOA fees are surging. See what lawmakers changed, what’s next, and how to protect your budget—read before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Why So Many Homebuyers Are Backing Out of Deals in 2026

Why buyers are backing out of home deals in 2026—and how to avoid costly surprises. Read the playbook before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 28, 2026

How Money Habits Form—and Why “Self-Control” Is the Wrong Villain

Learn how money habits form—and how to rewire spending and saving using behavioral science. Read the framework and start today.

By FMC Editorial Team

Latest Reviews

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs....

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market...

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan...