The Real Math of Money in Relationships

By Article Posted by Staff Contributor

The estimated reading time for this post is 943 seconds

Skip to Table of Contents

Skip to Key Takeaways

Skip to Timeline

Skip to FAQ

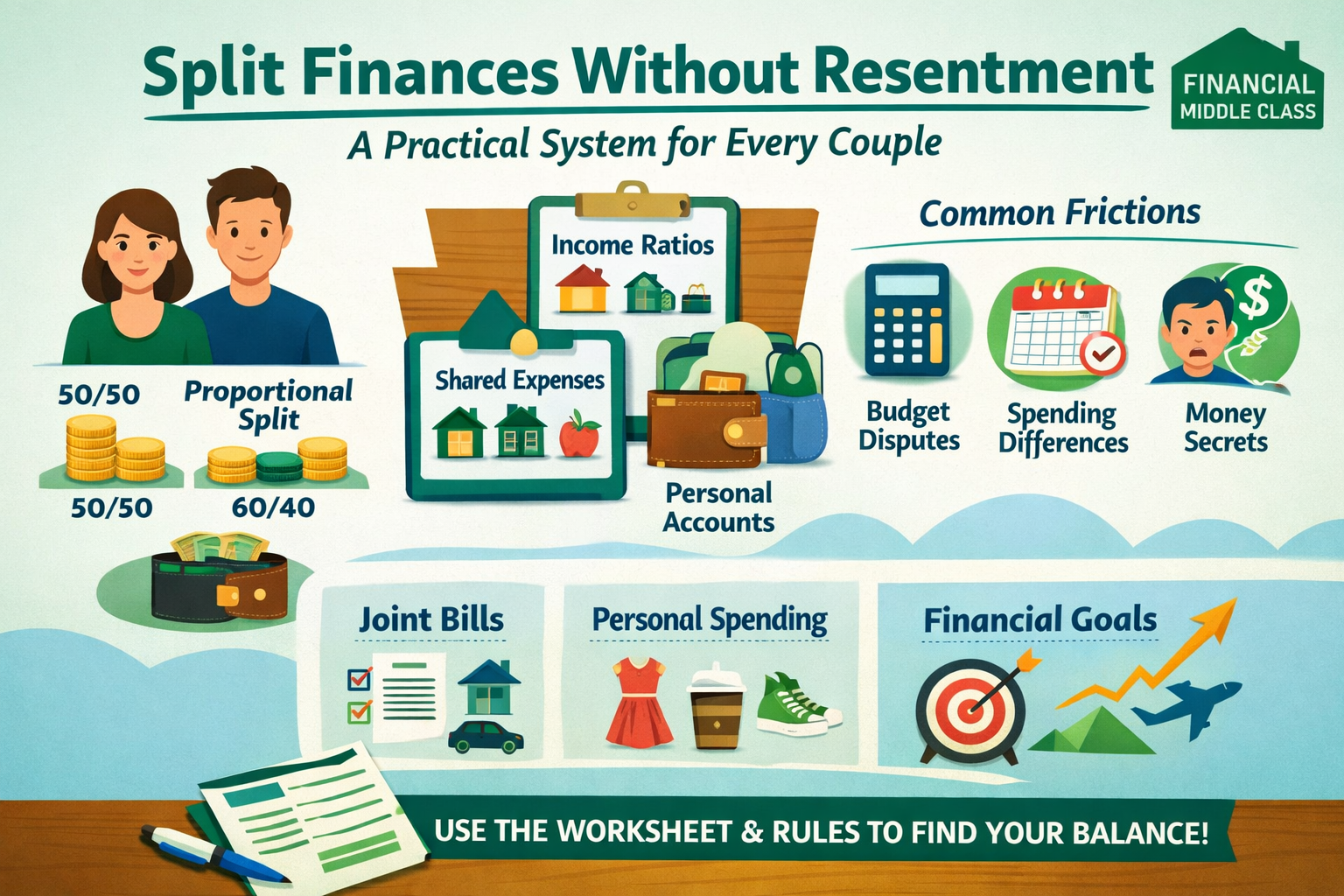

Split Finances as a Couple Without Resentment

A comprehensive guide for every couple—any income ratio, any living arrangement, any friction.

Couples don’t fight about money because they can’t do math.

They fight because money sits on top of things most people don’t say out loud: power, freedom, safety, dignity, and the fear of being trapped—by debt, by a lifestyle you can’t afford, by expectations you didn’t agree to, or by a partner who keeps score.

So, when someone says, “Should we do 50/50?” what they often mean is:

- “Will you respect me if I earn less?”

- “Will you control me if we combine?”

- “Will I end up carrying you?”

- “If this ends, will I be financially wrecked?”

- “If this works, will I still feel like an adult?”

Key Takeaways

- “Equal” and “fair” aren’t synonyms. Decide what “fair” means before touching numbers.

- Use the 3-bucket framework: Essentials (shared), Upgrades (special rule), Personal (no debate).

- Personal money prevents control. Every couple needs autonomy that doesn’t require permission.

- Hybrid usually wins: joint-for-bills + separate personal, funded equally or proportionally.

- Stress-test your plan against debt, variable income, unpaid labor, family support, and resentment.

Intro: what you’re really arguing about

If your relationship ever turned into a courtroom over $12 at Target, don’t feel special. That’s normal. Because the argument is rarely about $12.

Money arguments are often about who feels safe, who feels respected, and who feels like they’re losing freedom inside a relationship that’s supposed to add freedom—not subtract it.

The goal of this guide isn’t to crown one “correct” system. It’s to help you build a system that’s:

- Sustainable (nobody is quietly drowning)

- Transparent (no secret landmines)

- Protective (your household can absorb real life)

- Dignified (no one feels parented, audited, or minimized)

Truth: The “best” split is the one that prevents resentment from compounding quietly over time.

Timeline: what to do at each relationship stage

Use this as a practical path. You don’t need full financial merging to build trust—just the right structure for your stage.

Stage 1: Dating (not living together)

- Keep finances separate; agree on dates/trips (alternate, split, proportional, or one pays by choice).

- Talk values early: debt tolerance, savings habits, lifestyle expectations.

- Avoid “silent tests” (spending to prove love).

Stage 2: Cohabiting (unmarried)

- Use a joint bills account (or bill-splitting tool) + separate personal accounts.

- Write down basics: rent split, deposits, ownership of shared purchases, move-out plan.

- Avoid buying property/co-signing/merging debt without a contract.

Stage 3: Married (or legally merged)

- Any system can work, but protect autonomy (personal money) and clarify joint liability (debts/contracts).

- Define purchase thresholds and shared goals (emergency fund, sinking funds, retirement).

- Hold a short monthly money meeting to adjust the system as life changes.

Stage 4: Kids / Blended families / Prior obligations

- Define what’s “shared household” vs “prior obligations.”

- Create sinking funds for predictable kid-related costs.

- Align norms for spending, gifts, activities, and family support.

Stage 5: Variable income (commission / gig / business)

- Use base contribution + buffer (1–3 months) + quarterly true-up into goals.

- Don’t build your lifestyle off peak months; build it off conservative averages.

Define “fair” before you touch the numbers

Most couples argue forever because they’re using different definitions of fairness without realizing it.

| Definition | What it means | What can go wrong |

|---|---|---|

| Equal contribution | 50/50 on shared bills and goals. | Looks clean on paper—until one person is stretching, stressed, or silently borrowing to “keep up.” |

| Equal sacrifice | Contribute proportionally so the strain feels similar. | Can slide into “provider vs dependent” if autonomy and dignity aren’t protected. |

| Equal lifestyle | Both partners share a similar quality of life. | Without upgrade rules, the higher earner can unintentionally set the lifestyle and call it “normal.” |

| Equal autonomy | Each person keeps money they can spend without permission. | Autonomy becomes secrecy when spending undermines shared goals without disclosure. |

The question that unlocks the whole conversation:

What would feel unfair to you—even if the math looked clean?

What the data suggests (and what it doesn’t)

Two things can be true at once:

- A lot of couples keep at least some money separate.

- Pooling money is often associated with higher relationship satisfaction—but that doesn’t prove it causes happiness.

How common is “separate”? Recent U.S. Census Bureau reporting (using 2023 data) suggests that nearly a quarter of married couples had no joint bank account, and the share without a joint account increased compared with earlier decades. Meanwhile, a Bankrate survey of committed couples (married/civil partnership/cohabiting) found that most keep at least some accounts in their name only.

Who stays together longer? Multiple research papers find that full pooling (versus fully or partly separate) is associated with higher relationship satisfaction and lower likelihood of breakup over time. But remember the real-world caveat: couples who already feel “like a team” may be more willing to pool money in the first place. So treat this as guidance—not destiny.

How to use this information like an adult

- Don’t copy a system because it’s “traditional.” Copy it because it fits your risk profile and friction profile.

- If you choose separate or hybrid, the fix is not guilt. The fix is clarity, thresholds, and transparency.

- If you choose pooling, the fix is not “one pot.” The fix is autonomy money so nobody feels parented.

Decision tree: pick a system in 5 minutes

Use this as your first pass. You can adjust later. What matters is having a system instead of vibes.

| Your reality | Start here | Why it works |

|---|---|---|

| Dating / not living together | Separate finances + clear date/travel rules | Builds clarity without premature entanglement |

| Living together, incomes close | 50/50 or Hybrid | Simple, stable, low friction |

| Living together, meaningful income gap | Proportional or Hybrid (funded proportionally) | Prevents “keep up” stress |

| History of control/resentment | Hybrid + strong autonomy lanes | Reduces surveillance and scorekeeping |

| Variable income | Hybrid + buffer + quarterly true-up | Stability in down months, momentum in up months |

| Stay-at-home / caregiving unpaid labor | Team household model + autonomy for both | Recognizes real contribution beyond paychecks |

The 4 finance systems (and what breaks them)

There are four common setups. None is morally superior. Each breaks in predictable ways if you ignore its weak points.

System A: 50/50 split

Best when: incomes are similar and lifestyle expectations match.

Breaks when: one person is quietly stretching or borrowing to “keep up.”

System B: Proportional split (income ratio)

Best when: meaningful income gap, uneven burdens, or one partner is transitioning.

Breaks when: it becomes “provider vs dependent” instead of “team.”

System C: Hybrid (joint-for-bills + separate personal)

Best when: you want stability without turning your relationship into an audit.

Breaks when: you never define what’s shared vs personal—so everything becomes a debate.

System D: Full pooling (one pot)

Best when: aligned values, shared mission, high transparency.

Breaks when: autonomy disappears and secret spending starts.

Evergreen default for most couples: Hybrid. Joint bills + joint goals + personal lanes. Fund joint parts equally or proportionally depending on the income gap.

The 3-bucket framework

Most conflict is “category conflict.” People fight because they’re arguing about what a purchase is.

Bucket 1: Essentials (shared life)

Housing, utilities, groceries, insurance, transportation basics, childcare, basic household needs.

Bucket 2: Upgrades (optional lifestyle)

Nicer home, premium car, pricier vacations, elevated dining, subscriptions that raise baseline spending.

The rule that prevents lifestyle coercion:

If one partner pushes the upgrade, that partner covers the difference or the lifestyle caps at the lower earner’s comfort.

Bucket 3: Personal (autonomy)

Hobbies, personal travel, gifts for your people, clothes splurges, beauty/hair, personal subscriptions.

Rule: Personal money pays. No debate. No cross-examination.

Personal money: autonomy that prevents control

Every couple—yes, even the “one pot” couples—needs no-questions-asked personal money. Without it, you get the permission economy:

- “Do you really need that?”

- “How much was that?”

- “Must be nice…”

That’s not budgeting. That’s parenting.

Simple rule: set personal money as either 5–15% of take-home pay or $200–$500 per person per month (scaled to your budget). Many couples do best with equal-dollar personal money because autonomy is psychological.

Examples for every income ratio (and the frictions to expect)

Below is a practical way to split shared costs without turning your marriage into a spreadsheet war.

| Income ratio | How to fund Essentials + Goals | Common friction | Fix that works |

|---|---|---|---|

| 50/50 | Split joint costs evenly. Keep personal money equal. | Saver vs spender fights. | Personal lanes + shared discretionary cap + purchase threshold. |

| 60/40 | Fund Essentials/Goals proportionally (60/40). Personal money often equal-dollar. | Lifestyle creep driven by the higher earner. | Upgrade rule: cover the difference or cap lifestyle. |

| 70/30 | Proportional funding (70/30). Protect autonomy money. | Provider/dependent psychology. | Explicitly value non-income contributions + protect autonomy. |

| 80/20+ | Heavily proportional. Build strong rules so money doesn’t become authority. | “Because I pay for it” energy. | Ban weapon phrases; use thresholds + buckets + a monthly reset. |

| One-income | Team household model. Autonomy for both. Retirement protection for non-earner. | Unpaid labor gets minimized; resentment builds. | Define roles + protect dignity: personal money, time, long-term security. |

The upgrade rule in real life (quick example)

If the lower earner is comfortable spending $2,000/month on housing and the higher earner wants the $3,000 place, you have two clean options:

- Option A: cap the housing budget at $2,000 and live there—no resentment tax.

- Option B: live in the $3,000 place, but the person pushing the upgrade covers the extra $1,000.

What you don’t do is call it “our choice” while one person quietly sacrifices.

Living arrangements: dating → cohabiting → married → blended

Same principle, different risks.

Dating (not living together)

Keep money separate. Agree on how dates and trips are handled. Don’t use spending as a loyalty test. Talk values early.

Cohabiting (unmarried)

Hybrid works best here: joint bills + separate personal. Put the basics in writing: rent split, deposits, ownership of shared purchases, and what happens if someone moves out.

Married

Any system can work, but joint liability matters more than account structure. Protect autonomy. Set thresholds. Build shared goals. Hold a monthly reset.

Long-distance

Keep finances separate; create a shared “together fund” for visits and align expectations on frequency and cost. Don’t let one person finance the relationship.

Blended families / prior obligations

Define what’s “shared household” vs prior obligations. Build sinking funds for kid-related costs. Align norms for gifts, activities, and family support. Hidden assumptions become future resentment.

Common frictions (and fixes that stick)

Most couples don’t need more advice. They need a better operating system.

Friction: Bills (predictability)

Fix: automate transfers after paychecks, autopay fixed bills, and keep a bills buffer (at least $1,000–$2,000 or one month of essentials).

Rule: no bill should depend on memory.

Friction: Debt (shame + delayed goals)

Pick a policy on purpose:

- Personal debt, personal payments (with transparency + timeline)

- Shared mission payoff (joint goals prioritize debt temporarily)

- Hybrid (higher earner covers more essentials so the debtor can pay faster)

Rule: debt can’t be a secret if it affects shared life.

Friction: Spending (values clash)

Fix: personal money lanes + shared discretionary cap + purchase threshold for shared funds (anything over $X requires a quick check-in).

Rule: stop turning every swipe into a character trial.

Friction: Saving (uneven urgency)

Fix: agree on a savings floor, build sinking funds for predictable “surprises,” and protect fun money so the plan doesn’t feel like punishment.

Rule: a plan that feels like punishment gets sabotaged.

Friction: Family support (money leaving the household)

Fix: create a family support line item with a cap, define “emergency” vs “ongoing,” and treat anything that touches shared goals as a shared decision.

Friction: Control / resentment (the quiet killer)

Fix: equal autonomy money, a monthly reset meeting, and a ban on weapon phrases (“because I pay for it,” “my money,” “you don’t contribute”).

Use clean language instead: “I feel like the safety net.” / “I feel monitored.”

Friction: Unequal unpaid labor (often ignored, always costly)

Fix: treat unpaid labor as real contribution. Protect autonomy for both partners and plan retirement/security for the non-earner.

Rule: earnings-only “fair” fails here.

Friction: Irregular income (commission / gig / business)

Fix: base contribution + buffer (1–3 months) + quarterly true-up into goals.

Rule: don’t build lifestyle off peak months.

Friction: Financial infidelity / secrecy

Fix: separate autonomy is fine; secret obligations that undermine goals are not. Agree on disclosure rules: debts, recurring commitments, and anything that risks bills or savings.

Rule: privacy protects dignity; secrecy destroys trust.

Transparency without surveillance

Transparency doesn’t mean constant auditing. It means both partners understand the household reality:

- Both know bills, goals, and obligations

- Debts and recurring commitments are disclosed

- No hidden spending that undermines shared goals

Line in the sand: privacy protects dignity; secrecy destroys trust.

The 25-minute monthly money meeting

Every system fails if it never gets updated. This meeting isn’t romantic. It’s maintenance.

Agenda (25 minutes): one win → bills check → upcoming 30–60 days → goals progress → adjustments → resentment scan

Rule: no blame language, real numbers, end with a decision.

A plug-and-play setup you can implement tonight

Keep it simple. Complexity is where resentment hides.

Step 1 Choose your system (50/50, proportional, hybrid, pooling).

Step 2 Create lanes: Joint Bills + Joint Goals + two Personal lanes.

Step 3 Set 3 rules: upgrade rule + personal money rule + purchase threshold.

Step 4 Automate transfers + autopay + low-balance alerts.

Script that prevents the dumb fight:

“I want this to feel fair and sustainable. Let’s fund essentials based on our reality, protect personal money for both of us, and make upgrades explicit.”

Printable worksheet: House Money Rules

Fill this out together. Then stop re-litigating the same arguments.

Living arrangement dating / cohabiting / married / long-distance / blended

Fairness definition equal contribution / equal sacrifice / equal lifestyle / equal autonomy

System 50/50 / proportional / hybrid / pooling

Bucket definitions

Essentials (shared):

Upgrades (rule): If one partner pushes the upgrade, they cover the difference OR we cap lifestyle to the lower earner’s comfort.

Personal (personal):

Personal money (no questions asked)

$ ______ per person per month

Shared goals (next 90 days)

Goal 1: ____________________ $ ______ / month

Goal 2: ____________________ $ ______ / month

Goal 3: ____________________ $ ______ / month

Purchase threshold

Purchases over $ ______ from shared funds require a check-in

Money meeting

Date/time each month: ____________________

Agenda: win → bills → upcoming → goals → adjustments → resentment scan

FAQ

Is keeping separate accounts a red flag?

No. Secrecy and resentment are the red flags. Many stable couples use hybrid systems for clarity and autonomy.

Is 50/50 the only “fair” way?

No. 50/50 is one definition (equal contribution). Depending on your situation, equal sacrifice, equal lifestyle, or equal autonomy may be more sustainable.

What if one partner earns more and wants nicer things?

Use the upgrade rule: the partner pushing the upgrade covers the difference, or you cap the lifestyle to the lower earner’s comfort. No passive pressure.

Should we combine everything when we get married?

Only if autonomy and transparency survive. Marriage doesn’t require elimination of boundaries.

How do we stop fighting about “little purchases”?

Personal money lanes + shared discretionary cap + a purchase threshold for shared funds. That’s the adult version of peace.

What if one partner does unpaid labor (kids/caregiving/household management)?

Treat it as real contribution. Protect autonomy for both partners and plan retirement/security for the non-earner. Earnings-only “fair” will fail here.

Comment: What’s your biggest money friction right now—bills, debt, spending, saving, family support, unpaid labor, or control/resentment—and what system are you using today?

Closing thought: Structure isn’t cold. Structure is how love survives real life. A good system makes two things true at once: the household is stable, and both partners feel like adults—respected, safe, and free.

RELATED ARTICLES

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

Leave Comment

Cancel reply

Gig Economy

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

By FMC Editorial Team

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

By MacKenzy Pierre

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan to escape 25% APR debt.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

What To Do If You Get Fired With an Outstanding 401(k) Loan

Fired with a 401(k) loan? Avoid taxes, offsets, and deadline traps with this step-by-step checklist. Read now.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

The Real Math of Money in Relationships

Split finances without resentment. Any couple, any income ratio. Use the worksheet + rules—start today.

By Article Posted by Staff Contributor

American Middle Class / Feb 03, 2026

Investing or Paying Off the House?

Invest or pay off your mortgage? See a $500k example with today’s rates, dividends, and peace-of-mind math—then choose your plan.

By Article Posted by Staff Contributor

American Middle Class / Jan 30, 2026

Gold, Silver, or Bitcoin? Start With the Job—Not the Hype

Gold, silver or Bitcoin? Learn what each is for—and how to size it—before you buy. Read the framework.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Florida Homeowners Pay the Most in HOA Fees

Florida HOA fees are surging. See what lawmakers changed, what’s next, and how to protect your budget—read before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Why So Many Homebuyers Are Backing Out of Deals in 2026

Why buyers are backing out of home deals in 2026—and how to avoid costly surprises. Read the playbook before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 28, 2026

How Money Habits Form—and Why “Self-Control” Is the Wrong Villain

Learn how money habits form—and how to rewire spending and saving using behavioral science. Read the framework and start today.

By FMC Editorial Team

Latest Reviews

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs....

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market...

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan...