APR vs. APY, Revolving Debt, and the Interest Games Lenders Play

By Article Posted by Staff Contributor

The estimated reading time for this post is 647 seconds

APR vs. APY, Revolving Debt, and the Interest Games Lenders Play

Financial Middle Class • Updated for 2026-ready money decisions • Focus: revolving debt interest

Last updated:

Interest Isn’t “Just a Number.” It’s Rent.

If you’ve ever paid every month and still felt stuck, you’re not crazy. You’re just inside the math.

You’ve seen the numbers. APR. APY. 0% intro. “As low as.” They sit there on the screen like they’re just facts—like the weather. Neutral. Unemotional.

But interest isn’t neutral. Interest is a system. And if you don’t understand the rules, you’ll keep paying tuition for a class you never signed up for.

This is the middle-class reality: you’re not trying to get rich off leverage. You’re trying to stay stable. Mortgage paid. Car running. Kids fed. Credit score intact. You want the American Dream without the American fine print.

So let’s translate the language lenders use into something real.

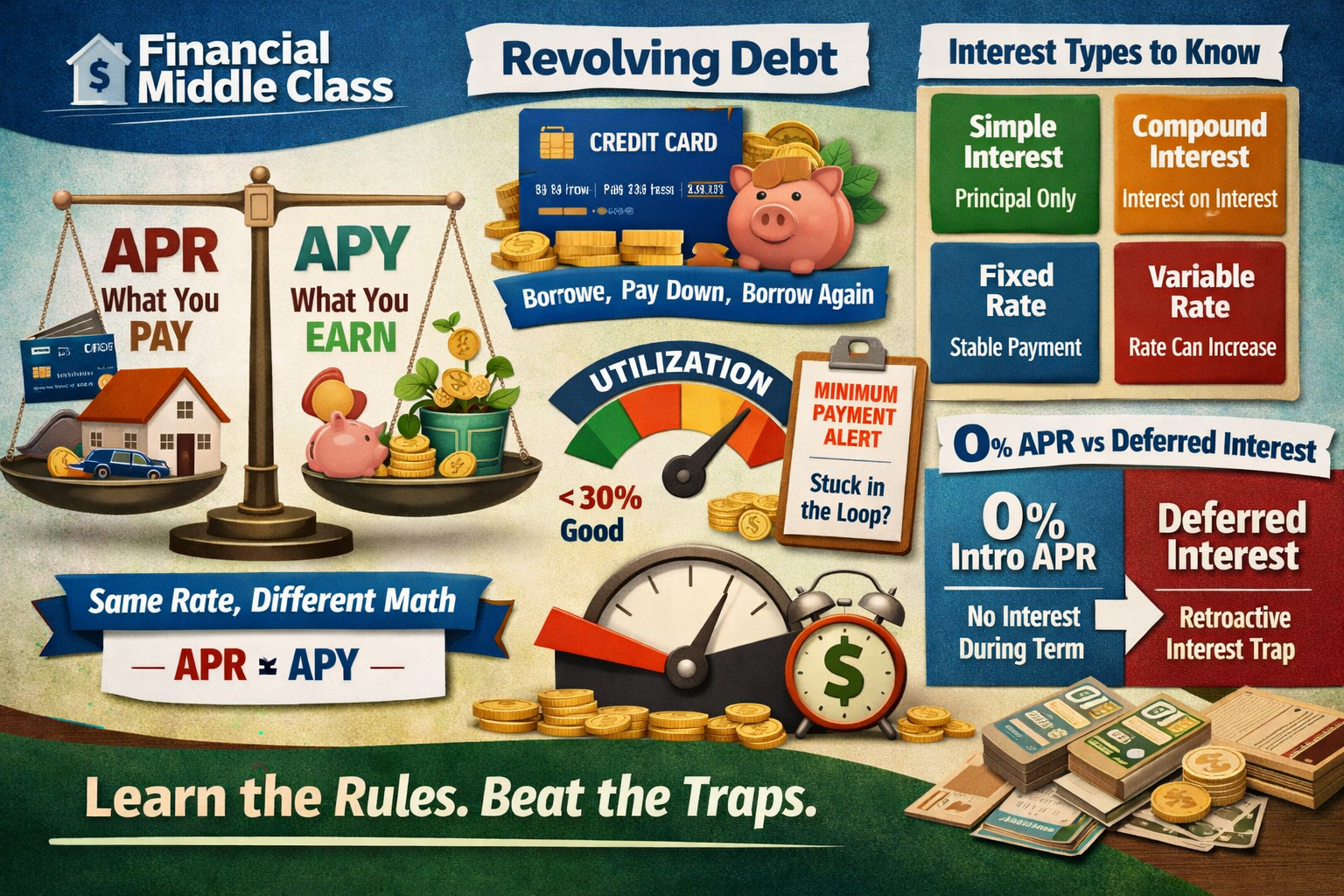

APR vs. APY: The Two Letters That Separate Borrowers From Earners

Let’s get this straight, because people mix these up all the time.

APR = what you pay

APR (Annual Percentage Rate) is the cost of borrowing, stated as a yearly rate. You’ll see it on credit cards, mortgages, auto loans, and personal loans. APR is the lender’s price tag. The sign in the window.

APY = what you earn

APY (Annual Percentage Yield) is what your money earns after compounding. You’ll see APY on savings accounts, money markets, and CDs. APY is the “real total” once interest starts earning interest.

Translation: APR is what debt does to you. APY is what savings does for you. And the bank would love for you to obsess over the wrong one.

The same rate, different reality

Here’s why APR and APY are not twins. If a savings account compounds monthly, the bank is paying you interest… and then paying interest on that interest. So the yield creeps higher than the simple headline rate.

Example: put $10,000 in a savings account at “5%” with compounding. Over the year, your APY ends up a little higher than 5% because you earned interest on interest along the way. That’s compounding—small in the short run, serious in the long run.

Now flip it. Credit cards often calculate interest daily. So even if the APR is “only” 24.99%, the day-by-day math means your balance doesn’t sit still. It grows quietly, like mold.

Revolving Debt: The Debt That Never Has to End

If installment debt is a train ride—fixed stops, fixed route—revolving debt is a treadmill. You can slow down, speed up, hop off if you can. But the belt keeps moving.

Revolving debt is a credit line with a limit that stays open: credit cards, HELOCs, personal lines of credit, and store cards. You borrow. You pay. You can borrow again.

This is why it’s seductive: it feels flexible. It feels like control. But flexibility cuts both ways.

The minimum payment is the most expensive “small” choice you’ll ever make

Minimum payments are marketed like mercy. They’re not mercy. They’re a business model.

When you pay the minimum on a credit card, you’re basically saying: “I’d like to rent this debt for as long as possible.”

Because minimum payments are built to keep your balance alive. They cover interest, maybe a sliver of principal, and then you do it again next month.

Real-life vibe: you carry a $4,000 balance at a high APR, pay the minimum, and your principal barely moves. The cruel part is you feel responsible because you “paid something.” That’s the trap: responsibility theater.

Utilization: the credit-score pressure point

Your credit score doesn’t just judge you for being late. It judges you for using the credit you were offered. That metric is utilization:

Utilization = Balance ÷ Limit

Example: limit $10,000, balance $3,000 → utilization 30%.

Practical thresholds: under 10% is strongest, 10–30% is decent, over 30% starts to hurt, and over 50% can bleed points. Yes, you can pay on time and still watch your score get dragged because your checking account isn’t a trust fund.

Grace periods: the part nobody explains until it’s too late

A grace period is the time between your purchase and when interest starts—if you pay the statement balance in full. But if you carry a balance, some cards stop giving you that grace period on new purchases. Translation: you can start paying interest immediately—even on things you bought yesterday.

This is how the loop happens: carry a balance from last month, buy groceries this month, groceries start accruing interest right away, you pay, but the balance stays sticky. It’s not just the APR. It’s the structure.

Simple Interest and the Other Types That Decide Whether You Win or Lose

Interest isn’t one thing. It’s a family of rules. And the rulebook matters.

1) Simple interest: clean math (usually)

Simple interest means interest is charged only on the principal. Example: borrow $10,000 at 6% for one year → interest is $600. Straightforward.

But many loans that call themselves “simple interest” accrue daily. Pay late and the cost rises because timing matters. Simple interest doesn’t always mean cheap—it means it’s not compounding on itself.

2) Compound interest: the accelerator

Compound interest is interest on principal and on accumulated interest. This is the engine that builds wealth in savings and investing. And it’s the engine that cooks you on high-interest debt.

Compound interest is not moral. It’s a tool. It helps when you’re on the earning side (APY). It hurts when you’re stuck borrowing at high APR.

3) Fixed vs. variable rates: predictable pain vs. surprise pain

Fixed rates stay the same. Predictable payment, easier planning. Variable rates move with an index plus a margin (common with credit cards and HELOCs). When rates rise, your payment rises—but your paycheck usually doesn’t. That squeeze is how households get cornered.

4) Amortization: why your mortgage feels slow in year one

If you’ve ever looked at your mortgage and thought, “How did I pay thousands and only a few hundred hit principal?”—that’s amortization. Early payments are interest-heavy. Later payments shift more toward principal. Not a conspiracy. Just math most people weren’t taught.

5) Daily accrual: timing is a money skill

Daily accrual means interest is based on your daily balance. Paying earlier in the month can reduce interest. Paying before your statement closes can also lower utilization as reported to credit bureaus.

6) Precomputed/add-on interest: the “you thought you saved money” loan

Some loans calculate interest upfront and bake it into the repayment. Paying early might not save you what you expect because the interest was packed in from day one. If the math feels stubborn, that’s why.

7) 0% APR vs. deferred interest: not the same

0% promotional APR typically means no interest during the promo period; interest begins going forward if a balance remains. Deferred interest often reads “no interest if paid in full by X date.” Miss it by even $1 and you can get hit with retroactive interest back to day one. That’s not “no interest.” That’s a deadline with teeth.

Real-Life Walkthrough: The Credit Card Loop

Let’s put it together. You’ve got a $4,000 balance at a high APR. You’re paying the minimum because life is life.

Here’s what happens: interest eats your payment, principal barely moves, utilization stays high, your score stays pressured, an emergency hits, the balance goes back up. That’s the loop—not because you’re irresponsible, but because the math profits from normal people having normal problems.

How you break it:

- Stop new charges (or isolate one card for essentials only).

- Pay more than the minimum and aim extra money at principal.

- Pick a method: avalanche (highest APR first) or snowball (smallest balance first).

- If you use a 0% balance transfer, treat it like surgery—not vacation (fees + payoff plan required).

The Middle-Class Playbook: Use Interest Without Getting Used

If you’re carrying revolving debt

- Pay more than the minimum—always.

- Pay earlier in the month to cut daily interest and reduce reported utilization.

- Call and ask for an APR reduction or hardship plan. (Yes, it works often enough to be worth 10 minutes.)

- If you balance transfer, write the payoff math down first. No math = no deal.

If you’re about to borrow (mortgage/auto/personal)

- Compare APR, not just the monthly payment.

- Ask what fees are included and look at total cost over the term.

- If your budget is tight and your life is already unpredictable, fixed rates are usually the calmer choice.

If you’re saving

- Compare APY (and watch for fees/minimums that quietly erase the benefit).

- Compounding rewards consistency, not perfection.

- Build an emergency fund so the next surprise doesn’t become revolving debt interest.

If you’re tempted by a promo

- Confirm: 0% APR or deferred interest?

- Write the exact end date down.

- Assume one late payment changes the deal—because it often does.

A 30-Day Timeline to Stop Interest From Running Your Life

Week 1: Audit what you really signed up for

- List every debt: balance, APR, minimum payment, due date.

- Separate revolving vs installment (cards/HELOCs vs loans).

- Flag promo terms: 0% APR vs “no interest if paid in full.”

Week 2: Break the revolving loop

- Stop new charges (or isolate one card for essentials only).

- Set autopay to avoid late fees (then pay extra manually).

- If utilization is high, pay before the statement closes.

Week 3: Attack interest intentionally

- Choose avalanche (highest APR) or snowball (smallest balance).

- Call lenders: request an APR reduction or hardship plan.

- Consider balance transfer only with a written payoff plan.

Week 4: Build defenses so you don’t end up back here

- Start/boost an emergency fund (APY matters, fees matter more).

- Automate savings the same way bills are automated.

- Set rules: “credit is a tool, not income.”

FAQ

Is APR the same as the interest rate?

No. APR is meant to reflect the overall borrowing cost. On some loans it may include certain fees, so it can be higher than the note rate.

Why is my credit card so expensive even when I’m paying on time?

Revolving balances can accrue interest daily, minimum payments can barely touch principal, and high utilization can keep your score under pressure.

What credit utilization should I aim for?

As a practical target: under 30% if you can, and under 10% if you’re optimizing your score. Lower is generally better.

Does paying twice a month help?

Often yes. It can reduce your average daily balance (interest) and can help your utilization if you pay before the statement closes.

Is a HELOC revolving debt?

Yes. A HELOC is a line of credit—usually variable rate—so costs can rise when rates rise.

What’s the difference between 0% APR and deferred interest?

0% APR typically means no interest during the promo period. Deferred interest can charge retroactive interest if you miss the payoff deadline.

Why do mortgage payments barely reduce principal early on?

Amortization schedules are interest-heavy upfront. Over time, more of your payment goes to principal.

Related Reads:

The 10 strategies that actually lower your mortgage rate

The Truth That Hits Home

The middle class doesn’t need more shame. We need more clarity.

Because most people aren’t drowning from buying yachts. They’re drowning from groceries, emergencies, and interest that compounds faster than their income grows.

And that’s the quiet part: your interest rate isn’t just a number. It’s a power relationship. Once you learn the language—APR, APY, revolving debt, compounding—you stop being surprised by the bill.

You start being strategic. And in a world where stability costs more every year, strategy isn’t optional. It’s survival.

Quick question for you

Where has interest hit you the hardest lately—credit cards, a car note, a mortgage, a HELOC, or a “no interest” promo that wasn’t really no interest?

RELATED ARTICLES

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

Leave Comment

Cancel reply

Gig Economy

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

By FMC Editorial Team

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

By MacKenzy Pierre

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan to escape 25% APR debt.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

What To Do If You Get Fired With an Outstanding 401(k) Loan

Fired with a 401(k) loan? Avoid taxes, offsets, and deadline traps with this step-by-step checklist. Read now.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

The Real Math of Money in Relationships

Split finances without resentment. Any couple, any income ratio. Use the worksheet + rules—start today.

By Article Posted by Staff Contributor

American Middle Class / Feb 03, 2026

Investing or Paying Off the House?

Invest or pay off your mortgage? See a $500k example with today’s rates, dividends, and peace-of-mind math—then choose your plan.

By Article Posted by Staff Contributor

American Middle Class / Jan 30, 2026

Gold, Silver, or Bitcoin? Start With the Job—Not the Hype

Gold, silver or Bitcoin? Learn what each is for—and how to size it—before you buy. Read the framework.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Florida Homeowners Pay the Most in HOA Fees

Florida HOA fees are surging. See what lawmakers changed, what’s next, and how to protect your budget—read before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Why So Many Homebuyers Are Backing Out of Deals in 2026

Why buyers are backing out of home deals in 2026—and how to avoid costly surprises. Read the playbook before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 28, 2026

How Money Habits Form—and Why “Self-Control” Is the Wrong Villain

Learn how money habits form—and how to rewire spending and saving using behavioral science. Read the framework and start today.

By FMC Editorial Team

Latest Reviews

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs....

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market...

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan...