I. The $900 Question

Let’s be honest: most middle-class Americans can’t wrap their heads around paying $795 to $895 a year just to own a credit card. That’s a car payment—or at least two weeks of groceries. Yet tens of thousands of people happily hand over that annual fee to hold a piece of metal with “Platinum” or “Reserve” etched on it.

If you’ve ever looked at the Amex Platinum or Chase Sapphire Reserve and thought, who are these people?, you’re not alone. This isn’t just about luxury perks—it’s about class psychology, perceived value, and the widening gap between financial identity and financial reality.

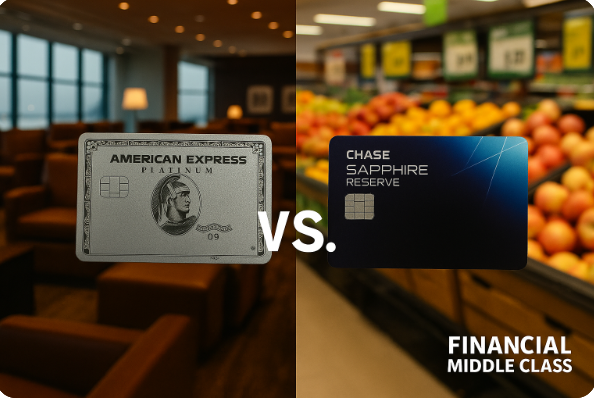

II. The Amex vs. Sapphire Rivalry: A Battle for America’s Richest Shoppers

The American Express Platinum and the Chase Sapphire Reserve are locked in a modern-day prestige war. Amex sells tradition, legacy, and concierge-level access. Chase sells flexibility, travel freedom, and sleek millennial branding.

Amex wants you to feel like a member of an exclusive club. Chase wants you to feel like a global explorer who happens to pay bills on time. Both cards target high-spending, high-credit households who can float $10,000 a month and still sleep well at night.

It’s Apple vs. Samsung all over again—different design philosophies, same endgame: get you to pay for loyalty.

Related Reads:

III. Why Some People Gladly Pay High Annual Fees

Here’s the psychology: for many affluent consumers, a premium credit card isn’t just plastic—it’s personal branding. The logic goes like this:

“I travel enough to make it worth it.”

“The perks pay for themselves.”

“It’s part of my lifestyle.”

In truth, most of those perks only pay off if you use them constantly. The average Platinum cardholder might earn $1,000 in travel credits—but they also spend $3,000 more per year on “eligible” expenses to access them. It’s a subtle illusion: you spend to save, and in the process, the bank wins twice.

The middle class, on the other hand, sees credit as a tool, not an accessory. It’s about managing cash flow, building credit history, and avoiding interest—not collecting status points at an airport lounge.

IV. Why the Middle Class Doesn’t Get It (And Doesn’t Need To)

Middle-class Americans look at a $900 card and say, “That’s my emergency fund contribution.” They view credit as a necessity, not a status symbol. It’s the difference between survival spending and status spending.

For most families, rising rent, student loans, and grocery inflation make paying for access feel ridiculous. It’s like the streaming wars—everyone wants your subscription, but none of them cover the basics that matter most.

Data from the CFPB shows that middle-income households carry higher credit utilization ratios and pay more in interest, even as they qualify for fewer rewards. The system rewards the already-rewarded.

V. When It Actually Makes Sense to Pay the Fee

That said, premium cards aren’t scams—they’re just not built for everyone. They make sense for a narrow band of consumers who travel frequently and can pay balances in full every month.

Amex Platinum vs. Chase Sapphire Reserve: The Head-to-Head

| Feature |

Amex Platinum |

Chase Sapphire Reserve |

| Annual Fee |

$695 – $895 |

$550 |

| Travel Credits |

Up to $200 hotel + $240 digital entertainment |

$300 travel credit |

| Airport Lounges |

Centurion + Priority Pass |

Priority Pass + Partner Lounges |

| Point Redemption |

Amex Travel + partners |

Chase Ultimate Rewards (1.5x value) |

The Break-Even Point

If you travel 8–10 times a year, dine out weekly, and book through partner programs, you can offset the fee. Otherwise, you’re chasing perks you’ll never fully use.

Practical steps:

- Calculate the value of perks you actually use.

- Skip upgrades unless you hit the break-even threshold.

- Call your issuer once a year—ask about retention offers or downgrade paths.

VI. The Credit Card of the Middle Class

While the wealthy debate lounge quality, the middle class just wants simplicity. Cards like the Citi Double Cash, Discover It Cash Back, and Chase Freedom Flex are household favorites for one reason: no games.

- No annual fee.

- Straightforward 1.5–2% cash-back rewards.

- Real-world perks—gas, groceries, utilities.

They’re the Honda Accords of credit cards: dependable, affordable, and built to last. A middle-class cardholder values predictability over prestige.

VII. What the Middle Class Actually Wants from Card Issuers

Let’s be clear—middle-income consumers aren’t asking for champagne in airport lounges. They want fairness and functionality:

- Lower interest rates and transparent terms.

- Real tools for budgeting and credit monitoring.

- Rewards that match everyday spending—groceries, gas, childcare, medical expenses.

- Customer service that doesn’t hide behind chatbots.

Stop Selling Us Status. Sell Us Stability.

Issuers who get that will win the next generation of loyal cardholders. The first bank that markets around peace of mind instead of platinum status could change the game.

Related Reads:

VIII. The Sidelines Aren’t Such a Bad Place

Here’s the punchline: sitting out the luxury-card war doesn’t make you less sophisticated—it might make you smarter. Every year, Americans pay billions in unnecessary fees chasing a lifestyle their net worth can’t sustain.

If you’re middle class, choosing a low-fee, high-value card isn’t playing it safe—it’s playing it wise. Financial peace is the real premium perk.

Before you chase perks, calculate your peace of mind.

The best credit card isn’t the one that gets you into a lounge—it’s the one that keeps you out of debt.