Save & Borrow: The Financial Needle the Middle Class Tries to Thread

By Article Posted by Staff Contributor

The estimated reading time for this post is 890 seconds

Table of Contents

- Save & Borrow: The Financial Needle

- Why Saving While Paying Debt Feels Impossible

- Tool Debt vs Trap Debt

- The Middle-Class Needle

- Save vs Pay Down Debt: Decision Ladder

- The Cash-Flow Calendar: Timing Matters

- The Two-Account System (Bills vs Life)

- Debt Triage: Which Fire First

- Sinking Funds: Predictable Emergencies

- Credit Score vs Cash Flow

- If You’re Already Behind

- Call Scripts for Negotiating Bills

- Real-Life Case Studies

- This Week / This Month / Next 90 Days

- The Truth That Hits Home

- Timeline

- FAQ

- Comment

Short on time? Read the Decision Ladder, Cash-Flow Calendar, and Call Scripts.

What to remember before you touch another dollar

- Slack beats perfection. A starter emergency fund keeps the next surprise from becoming a new monthly payment.

- High-interest credit cards are a leak. Pay them down steadily, but don’t drain your cash to zero.

- Timing is a budget category. Align due dates with paydays to shrink “danger weeks.”

- Structure wins. A Bills account + Life account reduces overdrafts, late fees, and panic swipes.

- Negotiate like an adult. Ask for APR reductions, hardship plans, payment plans, and fee waivers—then get terms in writing.

Save & Borrow: The Financial Needle the Middle Class Tries to Thread

On a random weekday that looks like every other weekday, somebody you know is doing the middle-class version of financial surgery at a kitchen table.

Payday is Friday. Rent is Monday. The car note lands in the first half of the month like it pays rent too. The insurance premium is on autopay—like gravity. Daycare is a second mortgage with finger paint. Groceries cost more even when you swear you’re buying the same things. And somewhere in the middle of that timeline is the advice people throw at you like it’s a personality trait: “Just save more.”

Save more…while you’re also borrowing to keep the whole system from tipping over. That’s the needle. Middle-class life demands you do three things at once: pay for today, prepare for tomorrow, and survive whatever surprise shows up next week. You’re not irresponsible. You’re compressed.

Why saving while paying debt feels impossible for the middle class

The problem isn’t that the middle class doesn’t know what to do. The problem is that the middle class is trying to do it without slack. Slack is the space between your life and the edge of the cliff. Slack is what turns a $700 car repair from “new credit-card balance” into “annoying inconvenience.” Slack is what lets you pause long enough to make a smart move instead of a panicked one.

Most middle-class households don’t lack discipline. They lack room. The baseline costs are heavy—housing, transportation, healthcare, childcare—and the timing rarely lines up with your pay schedule. When there’s no slack, debt becomes your emergency fund by default. Then interest turns one bad week into a long-term monthly payment.

Tool debt vs trap debt: the difference that decides your future

Debt isn’t automatically the villain. The issue is cost, purpose, and what the payment does to your cash flow. Tool debt is tied to stability and usually has a fixed payment and a clear end date. Trap debt is what you use to patch the month—because the month doesn’t care about your goals.

| What it looks like | Tool debt | Trap debt |

|---|---|---|

| Purpose | Supports stability (housing, reliable car, earning power) | Covers shortfalls (groceries, utilities, emergencies) |

| Cost | Typically lower APR and predictable | Often high APR and compounding |

| Cash-flow effect | Manageable, planned | Crowds out saving and creates “forever payments” |

| Risk | You can usually forecast the next 6–12 months | One surprise expense triggers a chain reaction |

The middle-class needle: pay debt fast enough to stop the bleeding, but not so fast you stay fragile

Here’s the paradox people learn the hard way: you can pay debt aggressively and still lose if you end up with no cash. Because the next time life hits—and it will—you’re back on the card. Back to borrowing. Back to interest. Back to minimum payments that feel like you’re pouring water into sand.

On the other side, saving while high-interest credit cards are charging you 20%+ is like trying to fill a bathtub with the drain open. Your savings grows slowly while the interest sprints. So you need a system that respects both realities: cash for shocks and payoff for leaks.

Save vs pay down debt: the decision ladder that actually works

If you’re trying to save while paying debt, you don’t need motivational posters. You need an order of operations that keeps you from sliding backward.

| Your situation right now | Your next move | Why it works |

|---|---|---|

| Little or no emergency cash | Build a starter buffer first ($500–$1,000 or one paycheck) | Without cash, every surprise becomes new debt |

| Starter buffer + high-interest card debt | Pay down the highest APR while keeping the buffer intact | Payoff sticks because you aren’t one expense away from swiping again |

| Stable income + shrinking balances | Build to one month of expenses | One month changes how your life feels |

| One month + manageable debt | Build 3–6 months over time and invest consistently | Wealth-building finally has a foundation |

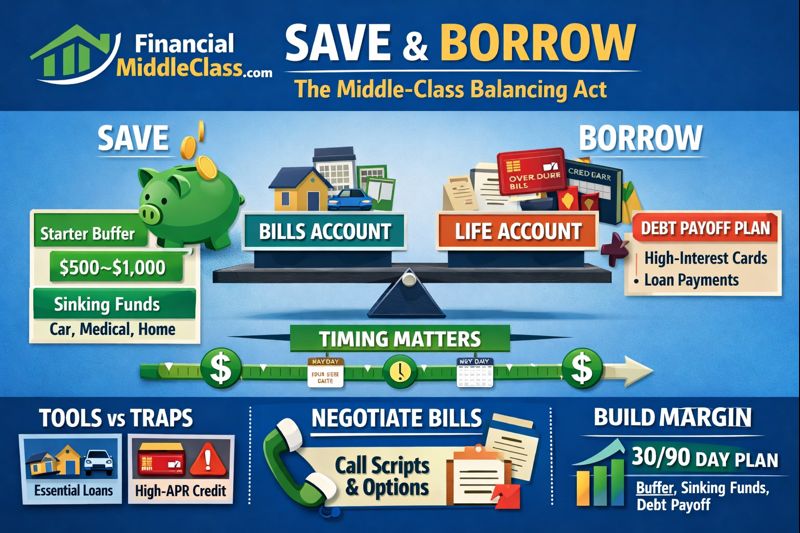

The cash-flow calendar: timing is the silent killer

A lot of middle-class stress isn’t about totals. It’s about timing. Money leaves in a clump. Paychecks arrive in a pattern that doesn’t match due dates. That mismatch creates overdrafts, late fees, and panic swipes. You can be good with money and still get wrecked by a calendar.

So treat the month like a calendar problem, not a willpower problem. Map your paydays and bill due dates. Find the danger week—the week where multiple big bills hit before money replenishes. That’s the week that turns budgeting into stress.

| Same income, same bills | Stacked month (stress) | Aligned month (control) |

|---|---|---|

| Rent/Mortgage | Due 1st | Due 1st |

| Car payment | Due 5th | Moved to 18th |

| Insurance | Due 8th | Split or moved to 22nd |

| Credit card minimum | Due 10th | Due 27th |

| Result | Early paycheck gets eaten; credit use rises | Fewer danger weeks; fewer “emergencies” |

The two-account system: stop your checking account from becoming a battlefield

A single checking account is where money goes to disappear. You look up and think, “I just got paid.” Then rent hits, insurance hits, the card minimum hits, and now you’re doing math like it’s a final exam. The two-account system isn’t fancy. It’s a boundary.

Bills account vs life account

Your Bills account is protected and boring. It’s for the expenses that don’t care how your month went: housing, utilities, insurance, daycare, minimum debt payments, phone. Your Life account is flexible and honest: groceries, gas, spending, and the things that change week to week.

You route money intentionally so Bills doesn’t have to compete with Life. If you’re paid biweekly, you transfer a set amount each payday. If you’re paid weekly, same idea—smaller transfers. This isn’t about being rigid. It’s about reducing the number of times you have to guess whether you can afford something. Guessing is expensive.

Debt triage: which fire to put out first

When you have multiple debts, the biggest balance isn’t always the biggest danger. The most dangerous debt is the one that bleeds your cash flow and punishes you for being human.

| Debt type | Why it’s dangerous (or not) | First move |

|---|---|---|

| High-interest credit cards (often 18%–30%+) | Compounds fast; minimums keep you stuck | Target highest APR while keeping a starter buffer |

| Payday/auto-title loans | Fees are the business model | Exit immediately; seek reputable nonprofit counseling |

| High-rate personal loans | Fixed payments can crush cash flow | Ask for modified terms; refinance only if rate truly drops |

| Auto loans | Necessary asset; repossession risk | Protect transportation; avoid extending terms unless it prevents default |

| Student loans | Rules are complex; options exist | Get on the right plan; avoid default at all costs |

| Mortgage | Often lower rate; housing stability | Protect housing first; don’t gamble with missed payments |

Sinking funds: predictable “emergencies” aren’t emergencies

Most emergencies aren’t surprises. They’re expenses you didn’t pre-fund. Tires, car repairs, school fees, back-to-school, holiday spending, annual premiums, co-pays, home maintenance. These are scheduled chaos. When they hit without a buffer, they become credit-card problems. When you drip money into sinking funds, they become inconvenient—but not disastrous.

Start small. A sinking fund isn’t a flex. It’s grown-up money. It’s you refusing to let August, December, or your next oil change ambush you.

Credit score vs cash flow: stop sacrificing stability to chase points

A good credit score is useful. But a lot of middle-class households treat the score like a fragile vase they can’t set down—even when cash is leaking out of their life. Here’s the reframe: cash flow keeps you alive. Credit helps you negotiate.

If you have to choose, protect housing, food, transportation, and stability first. A late payment hurts a score. A repossession hurts your life. A perfect score with no savings is not security. It’s optics. Credit recovers. Interest and instability can linger for years.

If you’re already behind: what to do when you’re late, delinquent, or in collections

If you’re already late, you don’t need guilt. You need order. Your priorities become brutally simple: protect the roof, protect the job, stop the snowball. That means housing first. Utilities next if shutoff is possible. Transportation if it affects work. Then minimum payments and payment plans.

Silence is expensive. If you can’t pay something on time, contact them before the due date—or as soon as you miss it—because that’s when you still have options.

Call scripts that actually work

You don’t have to sound desperate. You have to sound organized. Use these scripts and ask them to confirm the terms in writing.

“Hi, I’m calling because I want to avoid falling behind. I’m experiencing a temporary cash-flow crunch. Can you reduce my APR, waive recent fees, or place me on a hardship plan for 6–12 months? What options are available today, and can you confirm the terms in writing?”

“I want to pay this, but I can’t pay it all at once. What’s the lowest monthly payment you can offer with no interest? Also, do you offer financial assistance or charity care, and how do I apply?”

“I’d like to change my due date to align with my pay schedule. What dates are available, and can we keep autopay on the new date?”

“I want to keep coverage but lower my monthly premium. Can you review my policy for discounts, deductible options, or plan tiers that reduce cost?”

Real-life case studies: same income, different structure

Case study 1: single adult with a steady job and no slack

They aren’t reckless. They’re alone financially. A car repair becomes a credit-card balance. The fix isn’t “cut coffee.” The fix is a starter buffer plus one due-date shift so a single bill doesn’t trigger late fees, overdrafts, and panic borrowing.

Case study 2: family with childcare costs

They’re dual income, but daycare eats the margin. They aren’t bad with money. They’re funding a season of life that’s expensive. The win is building to one month of expenses, setting up sinking funds, and shrinking fixed costs where possible so the household stops living one surprise away from chaos.

Case study 3: homeowner with escrow swings and repairs

The mortgage jumps when taxes or insurance rise. Suddenly the budget breaks. The move isn’t panic-selling. The move is shopping insurance, reviewing escrow, and protecting housing while triaging other debts. Structure buys time. Time buys options.

A realistic plan: what to do this week, this month, and the next 90 days

This week: stabilize the month

Map paydays and due dates. Identify the danger week. Change one due date if you can. Separate Bills from Life if possible. Start a starter buffer—even if it’s small—because your next surprise should not become a new monthly payment.

This month: stop the bleeding

Pick the highest APR debt and hit it consistently while keeping the starter buffer intact. Make the calls that lower fees, reduce APR, or create payment plans. Reduce one fixed cost, even if it feels small, because small savings repeated monthly becomes slack.

Next 90 days: build the unbreakable floor

Grow the buffer toward one month. Start one sinking fund. Keep shrinking high-interest debt so the card stops being your emergency fund. You’re not aiming for perfect. You’re aiming for repeatable.

The truth that hits home

The middle class doesn’t struggle because it’s careless. It struggles because it’s expected to live an adult life on a budget that leaves no room for adult problems. And when there’s no room, the only thing that fits is debt.

Threading the needle isn’t about perfection. It’s about building enough slack that life stops turning into a payment plan—and starts feeling like something you can actually hold.

Timeline: the needle-threading sequence

Week 1–4: Build the starter emergency fund

Aim for $500–$1,000 (or one paycheck). This isn’t your forever emergency fund—this is your shock absorber so the next surprise doesn’t become a new balance.

Month 2–6: Pay down high-interest credit cards without draining cash

Target the highest APR first. Keep the starter buffer intact so you don’t boomerang back to the card the moment life happens.

Month 6–12: Build to one month of expenses

One month changes how your life feels. It reduces panic borrowing and gives you time to negotiate, adjust due dates, and make better decisions.

Year 1+: Build runway and invest consistently

Work toward 3–6 months over time, then invest like it’s a bill. The point isn’t maxing out everything—it’s building a floor that doesn’t crack.

FAQ: saving while paying debt

Should I build an emergency fund or pay off credit cards first?

Start with a small starter buffer first, then pay down high-interest cards while keeping that buffer intact. Paying debt to zero cash often sends people right back to the card.

What if my credit card APR is 0% promotional?

Still build the starter buffer, then make sure you can pay the balance down before the promo ends. The danger is the “cliff” when the rate resets.

How much should my starter emergency fund be?

Common targets are $500–$1,000 or one paycheck. Choose a number you can reach in 30 days so it becomes real, not theoretical.

How do I reduce the number of “danger weeks” in my month?

Align due dates to paydays. Ask to change due dates, split payments where possible, and route Bills money into a protected account first.

I’m already behind. What should I pay first?

Protect housing, then utilities if shutoff is possible, then transportation tied to work. After that, move debts into payment plans and get terms in writing.

Let’s talk

What’s your biggest “danger week” each month—rent, childcare, insurance, the car note, or something else? If you could move one due date, which one would it be?

RELATED ARTICLES

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

Leave Comment

Cancel reply

Gig Economy

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

By FMC Editorial Team

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

By MacKenzy Pierre

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan to escape 25% APR debt.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

What To Do If You Get Fired With an Outstanding 401(k) Loan

Fired with a 401(k) loan? Avoid taxes, offsets, and deadline traps with this step-by-step checklist. Read now.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

The Real Math of Money in Relationships

Split finances without resentment. Any couple, any income ratio. Use the worksheet + rules—start today.

By Article Posted by Staff Contributor

American Middle Class / Feb 03, 2026

Investing or Paying Off the House?

Invest or pay off your mortgage? See a $500k example with today’s rates, dividends, and peace-of-mind math—then choose your plan.

By Article Posted by Staff Contributor

American Middle Class / Jan 30, 2026

Gold, Silver, or Bitcoin? Start With the Job—Not the Hype

Gold, silver or Bitcoin? Learn what each is for—and how to size it—before you buy. Read the framework.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Florida Homeowners Pay the Most in HOA Fees

Florida HOA fees are surging. See what lawmakers changed, what’s next, and how to protect your budget—read before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Why So Many Homebuyers Are Backing Out of Deals in 2026

Why buyers are backing out of home deals in 2026—and how to avoid costly surprises. Read the playbook before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 28, 2026

How Money Habits Form—and Why “Self-Control” Is the Wrong Villain

Learn how money habits form—and how to rewire spending and saving using behavioral science. Read the framework and start today.

By FMC Editorial Team

Latest Reviews

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs....

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market...

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan...