The argument for the so-called business-friendly environment—low to no corporate taxes, lax financial and environmental regulations—is that we all benefit from a thriving stock market. After all, what are you complaining about? Isn’t your 401(k) benefiting from a healthy stock market?

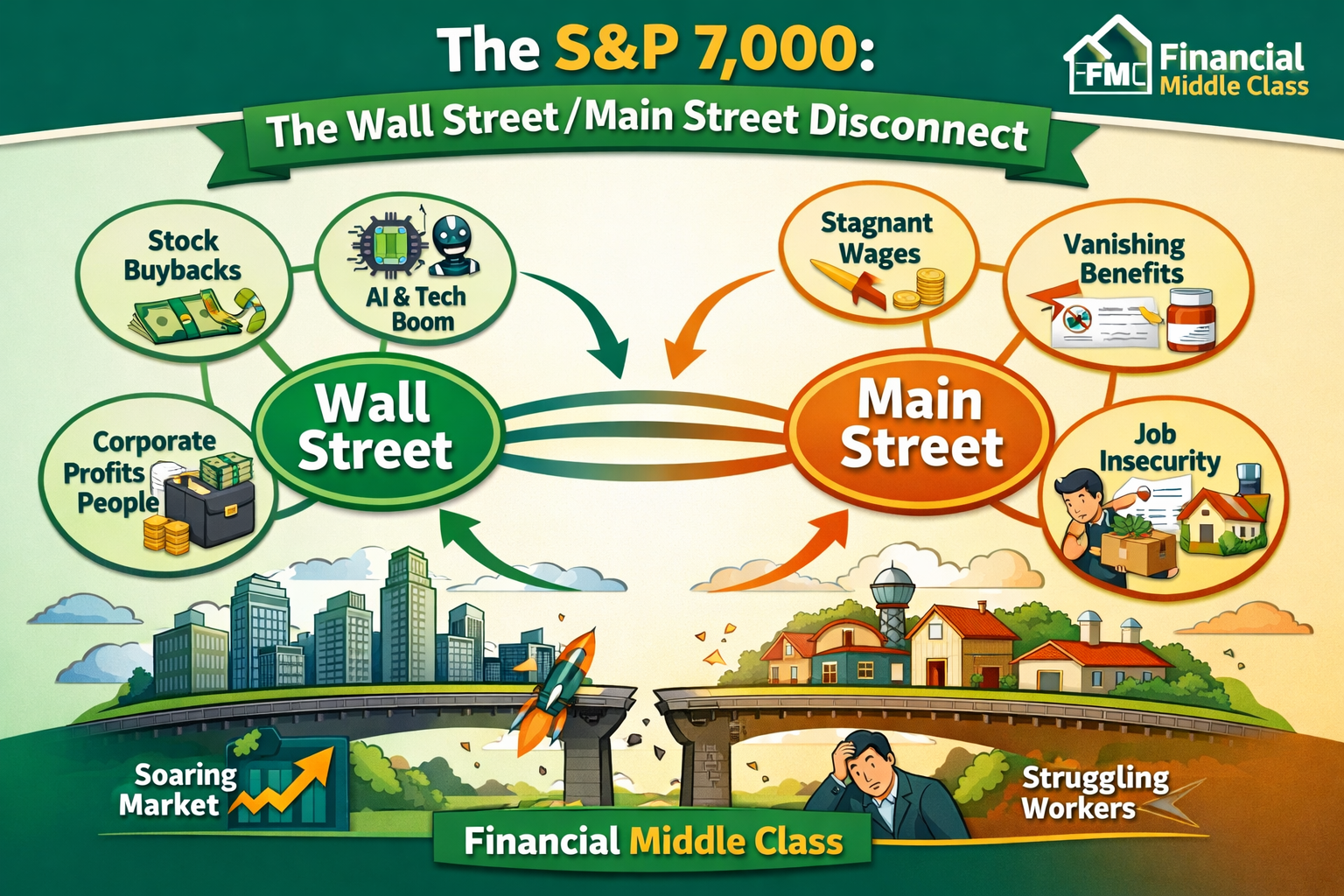

That argument is patently flawed because modern-day capital expenditures (CapEx), stock buybacks, and the stratospheric growth of AI and semiconductors have built a wall between the stock market and the macroeconomy. The market can be flying while regular people are just trying to keep their head above water.

There was a time when the stock market was the economy and the economy was the stock market. Those days are gone. The days of Hershey, PA and Oneida, NY are long gone. As a believer in capitalism, I often bring up those cities during any conversation around this topic to cement my argument for true and well-regulated capitalism. Milton Hershey built the company town to provide housing, schools, parks, and more to the employees of his thriving chocolate factory. Can you think of a company right now that would do such a thing—I’ll wait!

Companies used to see their stock prices go up because their business fundamentals were strong—great management, great product, a thriving workforce. Companies’ CapEx spending used to be in tangible infrastructure, including manufacturing plants that employed more people and manufactured better products. And companies used to use part of their profits to give bonuses to employees, pay them better wages, and provide them with better benefits.

Companies see employees on the right side of the balance sheet now.

And once you start looking at what corporate America does with its profits, you can see why the stock market and the real economy don’t move together the way they used to.

Let’s start with stock buybacks.

Buybacks, although a lazy way to allocate capital, are the cleanest way to make Wall Street happy without doing much for Main Street. A company can take billions of dollars, buy its own stock, shrink its outstanding shares, and suddenly earnings per share looks better—even if the business itself didn’t really change. That helps the stock price. That helps executive compensation. That helps the headlines. But it doesn’t build a plant. It doesn’t train workers. It doesn’t lower health insurance premiums. It doesn’t make a town more stable.

And look, I’m not saying buybacks should never happen. I’m saying they’ve become a habit. They’ve become a priority. They’ve become “the plan.” Meanwhile, the same companies will turn around and tell you raises have to be “measured,” benefits have to be “reviewed,” and headcount has to be “optimized.” That’s the disconnect right there. Companies in the S&P 500 bought about $943 billion worth of their own stock in 2024.

Now let’s talk about CapEx, because CapEx isn’t what it used to be either.

When people hear “investment,” they picture something real: a manufacturing plant, a warehouse, equipment, trucks, a new line that hires hundreds of people. That’s what CapEx used to look like for large parts of the economy. Today, a lot of CapEx is not that. It’s software. It’s data centers. It’s AI infrastructure. It’s spending that can be massive and still not create a lot of jobs for regular people in regular places.

So yes, companies are “investing,” but it’s often investment that doesn’t bring back the kind of broad-based employment that used to lift entire regions. It’s investment that supports scale, not payroll. And the more the economy shifts in that direction, the easier it becomes for the market to soar while wages and job security don’t.

And then there’s benefits—this is where the middle class really feels it.

People love to say, “Don’t worry, you have a 401(k).” Like that’s supposed to replace everything. But what about pensions? What about affordable health insurance? What about a benefit package that doesn’t feel like it’s getting smaller every year? What about stability?

Too many workers are paying more out of pocket for healthcare while companies brag about cost reduction. Too many workers are watching retirement shift from something an employer helped guarantee to something the worker has to figure out alone, in between rent, groceries, and car insurance. And then we’re told to clap because the S&P is up.

This is what I mean when I say employees are on the right side of the balance sheet now.

A worker used to be treated like an asset—human capital—something to develop, retain, and build around. Now workers are treated like a cost to reduce. Headcount is something to “trim.” Labor is something to “manage.” Benefits are something to “contain.” And shareholders love and reward companies’ layoffs. Sometimes a layoff is necessary. Fine. But now layoffs can happen even when companies are doing well—because Wall Street wants “lean,” and lean has become a religion.

The stock market has been deviating from companies’ fundamentals for a while now, and that deviation has been getting worse for the past five years. The top 4 world’s most valuable public companies have a combined valuation of about $14.9 trillion, and together they have a grand total of 620,820 employees.

The world’s most valuable public company by market capitalization—Nvidia—at roughly $4.45T has an anemic, lean operation of about 36,000 employees. Just for comparison, my local grocery store Publix employs over 260,000 people—read that again.

The biggest companies in today’s market can be shockingly light on labor compared to the older models of American corporate power. And that’s exactly why you can’t keep telling people, “The market is up, so you’re fine.”

Because the market can be up while benefits get worse. The market can be up while workers get treated like a cost problem. The market can be up while the town you live in doesn’t feel any better at all.

That’s the Wall Street/Main Street disconnect. And until we stop pretending the stock market is the economy, we’ll keep having the same argument—while regular people aren’t feeling the boom.