By Article Posted by Staff Contributor

The estimated reading time for this post is 588 seconds

Last updated: January 26, 2026 — pacing, cost checkpoints, and contingency planning reviewed for clarity (always adapt to your local market).

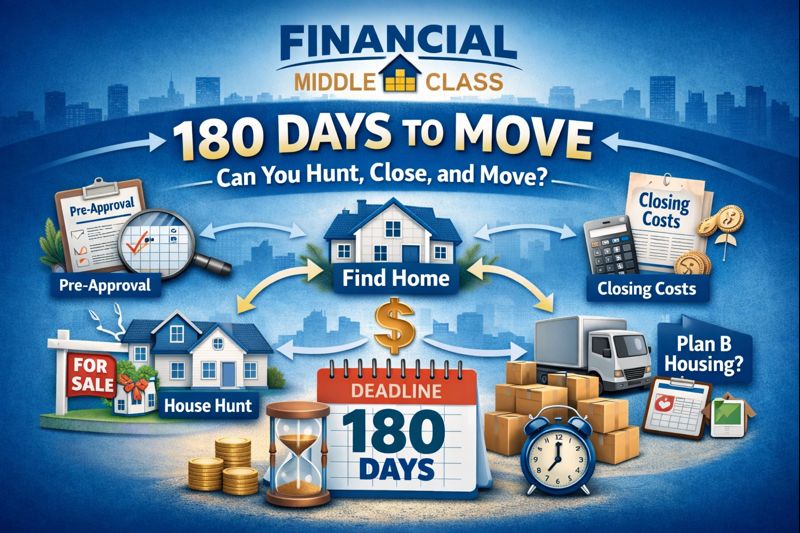

180 Days to Move: Can You Hunt, Close, and Move?

180 days sounds like a cushion. Six months. Enough time to breathe.

But in real life, an 180-day move isn’t one task. It’s three: find the home, finance the home, and move your life—all while your bills keep showing up on time.

The market doesn’t pause because your kid has a school deadline. Underwriting doesn’t speed up because your lease ends.

So yes: you can hunt, close, and move in 180 days. But only if you treat the clock like a budget. Spend it on purpose.

The timeline math nobody tells you

Most people think the mortgage is the slow part. Often, it’s the search.

Buyers report spending a median of 10 weeks looking, and many still say the hardest task is finding the right home.

That’s not because buyers are dramatic. It’s because “right” has to fit your price, your commute, your safety needs, and your monthly payment at the same time.

Then comes closing. Even when everything is “fine,” the process has steps that do not care about your feelings: appraisal, title work, underwriting review, final verification.

Your calendar doesn’t run the mortgage machine. The mortgage machine runs your calendar.

180-day timeline (no fluff—just pacing)

Days 1–30: Build your buyer engine

Get fully pre-approved. Gather documents. Decide your real payment ceiling. Clean up anything that creates underwriting questions.

The goal is simple: make your file easy to approve.

If you drift early, you pay later.

Days 31–90: Hunt like you mean it

Tour consistently. Track neighborhoods, comps, and deal-breakers. Make offers with a clear strategy: price, terms, and timing.

“We’ll see” is how 90 days turns into 150.

Decisiveness protects the calendar.

Days 91–140: Defend the closing date

Schedule inspection immediately. Keep negotiations tight. Get appraisal scheduled early. Push title and insurance in parallel.

Upload lender requests the same day.

Small delays stack. Stacked delays get expensive.

Days 141–180: Move without chaos

Lock in movers, utilities, school logistics, time off work, and a backup housing plan if the date slides.

Your goal is one move—not two.

A planned Plan B beats a panicked Plan B.

The Readiness Score: Are you Green, Yellow, or Red?

This isn’t about optimism. It’s about whether your timeline has slack.

Some people can do 180 days clean. Some can do it with guardrails.

And some are about to learn the hard way that hope is not a housing strategy.

| Readiness | What it looks like | What tends to break | The smart move |

|---|---|---|---|

| Green | Fully pre-approved, steady income docs, cash buffer, clear must-haves | Inventory and competition | Start hunting now; keep your file clean |

| Yellow | Approved but cash is tight; paperwork isn’t organized; credit is “fine but sensitive” | Small delays turn into real costs | Build buffer + pick Plan B housing early |

| Red | Credit issues, job/income changes, thin reserves, messy accounts | Underwriting delays + forced decisions | Stabilize first; choose flexibility over perfect |

If you’re Yellow or Red, you can still move. But you need fewer surprises and more options.

Your goal is not to “win the market.” Your goal is to get through the process without it draining you.

The Money Map: what 180 days really costs

Middle-class moves don’t collapse because people don’t work hard. They collapse because the process demands cash at inconvenient times.

Closing costs, prepaids, deposits, moving logistics—and then the silent category: delay costs.

A closing that slips a couple of weeks can create overlap rent, storage, rescheduled movers, extra childcare, and time off work.

If you’re middle class, that’s rarely “annoying.” It’s often credit card debt.

| Cost bucket | What it includes | Why it surprises people | What to do early |

|---|---|---|---|

| Deal costs | Inspection, appraisal, earnest money | You pay before you “own” anything | Set aside cash like a required fee, not a maybe |

| Closing costs | Lender/title/recording fees + prepaids | They add up fast and hit at once | Compare Loan Estimates early; ask for a fee breakdown |

| Move costs | Movers, truck, supplies, deposits | Last-minute bookings cost more | Get quotes and reserve by the midpoint |

| Delay costs | Rent overlap, storage, hotel, extensions | They’re not in most budgets | Choose Plan B housing before you need it |

If you want to be safe on a 180-day move, you’re not just saving for a down payment.

You’re saving for timing risk.

Rate lock and payment shock: your calendar becomes your rate

This is where timelines become expensive.

Rate locks can protect you, but they come with a window.

If your deal runs long, the cost can show up in your payment or your closing table.

The middle-class reality is simple: you don’t want your interest rate decided by a preventable delay.

So you manage the process like it matters—because it does.

Credit & underwriting: the “don’t make it harder” rules

People don’t usually lose time because they didn’t try. They lose time because they unknowingly create complications.

During your 180-day window, assume your lender is going to re-check things. Because they often do.

Don’t open new credit. Don’t finance furniture “because the payment is small.” Don’t switch jobs casually.

Don’t move large money around without documentation. Don’t miss payments.

Underwriting isn’t personal. It’s documentation. And documentation hates surprises.

Three 180-day roadmaps: pick your reality

Most advice fails because it assumes everyone is doing the same move. They’re not.

Your plan should match your situation.

| Scenario | What “success” looks like | Biggest risk | Plan B to choose early |

|---|---|---|---|

| Renting → Buying | Close before your lease ends | Search runs long | Month-to-month option or short-term rental |

| Selling → Buying | Two closings line up without panic | Market time + overlap costs | Rent-back, temporary housing, or list-first strategy |

| Relocation deadline | Land housing without rushing into a bad deal | Forced decisions under pressure | Short-term rental near work; buy after |

If you’re selling and buying, be honest: you’re juggling two transactions, two timelines, and one checking account.

You can still do 180 days—but you need more contingency planning than the other two groups.

Deal-killers that blow up closings (and how to protect your date)

Closings rarely fall apart from one big drama. It’s usually a few delays stacking.

Inspection: If issues show up, negotiations can drag. Protect your timeline by scheduling quickly and prioritizing safety and systems first.

Appraisal: A low appraisal can restart negotiations. Protect yourself by knowing the comps and staying grounded.

Title: Old liens or paperwork gaps can slow things down. Protect your date by asking for updates and pushing for clear next steps.

HOA/condo docs: These can be slow. Protect your timeline by requesting them immediately and confirming delivery dates early.

If you want to close on time, treat the closing date like it matters—because for most middle-class households, it does.

The Plan B Housing Playbook

A Plan B isn’t negative. It’s responsible.

Pick one option early so you’re not making expensive decisions under stress.

Month-to-month extension is clean but often pricier. Short-term rental costs more but gives control.

Rent-back can help when available. Storage plus a temporary stay works best when it’s planned—not improvised.

The point isn’t to assume things will go wrong. The point is to avoid panic choices if something slips.

Move logistics timeline: the unglamorous stuff that saves money

Moves get expensive when they become last-minute.

By Day 60, start quotes, start purging, and understand school enrollment requirements.

By Day 120, reserve movers or a truck, schedule time off, and line up childcare coverage.

By Day 150, confirm utilities, insurance, address changes, and your final walk-through plan.

The move itself is logistics. Logistics rewards early action.

Scripts: what to ask your lender, agent, and movers

These questions prevent vague answers and protect your timeline.

To your lender: “What delays loans like mine most often, and how do we avoid that?” “What’s the realistic close timeline for my file?”

“What lock period matches this contract?”

To your agent: “In this specific area, how long are homes taking to go pending?” “What terms matter most right now—price, timing, inspection, appraisal?”

“What’s our plan if the appraisal comes in low?”

To movers: “Is this quote binding or estimated?” “What triggers extra charges?” “What happens if my closing date moves?”

These questions don’t make you difficult. They make you expensive to surprise.

A real example: smooth close vs. a 21-day slip

Picture a household that looks like a lot of real people:

$120,000 income. A car payment. Student loans. Childcare costs. A revolving card balance.

Cash buffer after earnest money: $18,000. Goal: close before the lease ends.

| Outcome | What happens | The practical impact |

|---|---|---|

| Smooth close | Closing stays on schedule | Planned cash-to-close + planned move |

| 21-day slip | Appraisal delays + rescheduled movers + extra housing time | Overlap rent/storage + higher moving costs + stress spending |

That 21-day slip is where households feel the squeeze—not because they didn’t plan, but because the plan didn’t include enough slack.

FAQ

Can I do 180 days if I’m not pre-approved yet?

Yes, but your first 30 days become non-negotiable. A slow start is the easiest way to lose the timeline.

Can I close in 30 days?

Sometimes. Plan for a normal closing pace and be glad if you beat it. Fast closings usually happen when the file is clean and managed tightly.

Should I wait for rates to drop?

Waiting only helps if you can afford the wait. If you have a hard deadline, readiness and cash buffer usually beat forecasting.

What’s the most common reason a timeline blows up?

Small delays stacking: slow documents, late appraisal scheduling, title/HOA lag, and moving logistics planned too late.

If you only remember 7 things

- Treat 180 days like a budget.

- Don’t waste the first month.

- Build cash for timing risk, not just the down payment.

- Make your loan file easy to approve.

- Defend your closing date with same-day document habits.

- Pick a Plan B housing option early.

- Book logistics before you feel “ready.”

The truth that hits home

Middle-class moves don’t usually break because you didn’t try hard enough.

They break because the system charges you for delays, and most households don’t have unlimited slack.

Fees hit up front. Timelines shift. Bills don’t.

So if you’re doing this in 180 days, don’t rely on hope. Build structure. Build options. Protect your date.

Because the goal isn’t just finding a home. It’s getting there without the process draining you.

Quick question

If you had 180 days to move, what would worry you most: finding the home, the financing, or the move logistics?

Drop your situation (renting → buying, selling → buying, relocation deadline) and your biggest constraint—cash, timing, or credit.

RELATED ARTICLES

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

Leave Comment

Cancel reply

Gig Economy

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

By FMC Editorial Team

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

By MacKenzy Pierre

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan to escape 25% APR debt.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

What To Do If You Get Fired With an Outstanding 401(k) Loan

Fired with a 401(k) loan? Avoid taxes, offsets, and deadline traps with this step-by-step checklist. Read now.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

The Real Math of Money in Relationships

Split finances without resentment. Any couple, any income ratio. Use the worksheet + rules—start today.

By Article Posted by Staff Contributor

American Middle Class / Feb 03, 2026

Investing or Paying Off the House?

Invest or pay off your mortgage? See a $500k example with today’s rates, dividends, and peace-of-mind math—then choose your plan.

By Article Posted by Staff Contributor

American Middle Class / Jan 30, 2026

Gold, Silver, or Bitcoin? Start With the Job—Not the Hype

Gold, silver or Bitcoin? Learn what each is for—and how to size it—before you buy. Read the framework.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Florida Homeowners Pay the Most in HOA Fees

Florida HOA fees are surging. See what lawmakers changed, what’s next, and how to protect your budget—read before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Why So Many Homebuyers Are Backing Out of Deals in 2026

Why buyers are backing out of home deals in 2026—and how to avoid costly surprises. Read the playbook before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 28, 2026

How Money Habits Form—and Why “Self-Control” Is the Wrong Villain

Learn how money habits form—and how to rewire spending and saving using behavioral science. Read the framework and start today.

By FMC Editorial Team

Latest Reviews

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs....

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market...

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan...