Health Insurance as Startup Infrastructure:

By FMC Editorial Team

The estimated reading time for this post is 541 seconds

Health Insurance as Startup Infrastructure: How the ACA Opened the Door to Entrepreneurship—and how the 2026 Subsidy Cliff Could Slam It Shut

Dek: The Affordable Care Act didn’t “create entrepreneurs.” It did something more practical: it lowered the penalty for leaving payroll work by making health coverage portable. The scheduled expiration of enhanced ACA subsidies after December 31, 2025 risks rebuilding the very lock the law helped loosen.

Executive summary

- Entrepreneurship lock is real. When health insurance is tied to a job, starting a business often means gambling with your family’s coverage.

- The ACA reduced that lock by protecting people with preexisting conditions, building Marketplaces, and subsidizing premiums so coverage could follow the person—not the employer.

- The best empirical work finds measurable increases in self-employment among people most constrained by pre-ACA individual-market barriers—exactly where you’d expect the effect to show up.

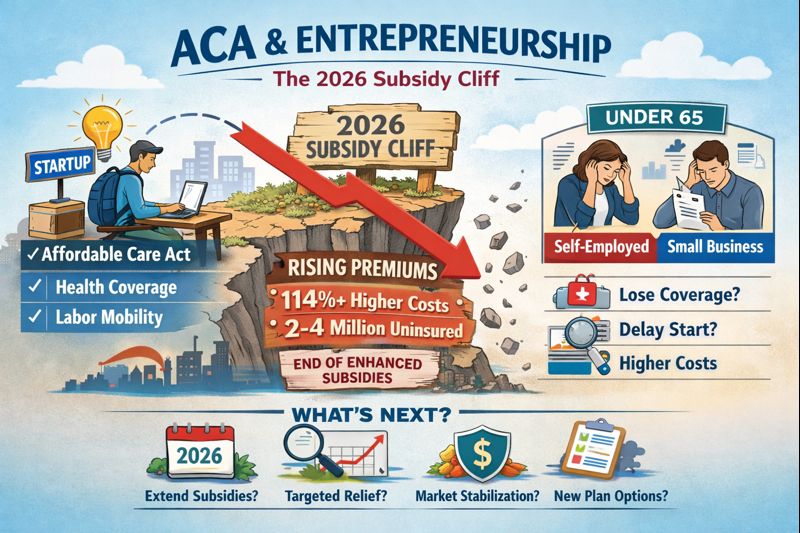

- But the affordability bridge is wobbling. Enhanced premium tax credits (the more generous subsidy rules) are scheduled to expire after Dec. 31, 2025, reverting on Jan. 1, 2026.

- Premium shock isn’t hypothetical. KFF estimates that, without an extension, subsidized Marketplace enrollees’ premium payments would rise 114% on average in 2026 (about $1,016 more per year), more than doubling what many households pay now.[

- Coverage loss is expected. CBO estimates 2.2 million more people would be uninsured in 2026 if the enhanced subsidies lapse; other modeling (Urban Institute) projects roughly 4.8 million becoming uninsured in 2026 under similar assumptions.[4][5]

- Congress hasn’t reached a deal heading into late December 2025; multiple reports describe any fix slipping into January 2026, which adds uncertainty on top of rising sticker prices.

- This is an economic policy choice, not just a health policy choice. When net premiums jump, people delay quitting jobs, postpone launching ventures, or go uninsured—each outcome dulls local economic dynamism.

- Most workable path: a multi-year extension (or durable reform) of enhanced credits paired with market-stabilizing tools (like reinsurance) and administrative simplification to reduce churn.

1) What the ACA changed: the mechanism behind “freedom to start”

In the U.S., entrepreneurship has never been just about ideas. It has always been about risk—especially the kind of risk that doesn’t show up in a pitch deck.

Health coverage is the clearest example. If your insurance comes through your employer, leaving that employer is not a clean transition. It’s a cliff. Before the ACA, the individual market could price people out, exclude conditions, or deny coverage outright. That reality kept plenty of would-be founders anchored to payroll jobs even when their skills, ambition, and market opportunity said “go.”

The ACA attacked that anchor through a set of blunt, practical interventions:

- Guaranteed access: ACA-compliant plans can’t refuse you because your medical history is complicated.

- A real purchase channel: Marketplaces made individual coverage legible—plans, prices, enrollment rules, and assistance in one place.[1]

- Subsidies that move with income: Premium tax credits lowered what many households pay out of pocket.

- A floor for low-income adults (where adopted): Medicaid expansion offered coverage that can survive volatile earnings—exactly the pattern early-stage founders often face.

Put those pieces together and you get something that looks less like “health reform” and more like economic infrastructure: a risk-management system that allows people to leave jobs without losing medical security.

2) What the research shows (and what it doesn’t)

Policy arguments about entrepreneurship are usually built on stories. Stories matter, but they aren’t evidence. The serious question is whether we can observe behavioral change after the ACA among people most likely to be locked in place by insurance risk.

One of the cleaner findings in the literature is that the ACA increased self-employment for groups with high demand for health insurance—people who, before the ACA, faced the steepest penalties for buying coverage outside an employer. In other words: the effect shows up where the theory says it should.

That’s important for two reasons:

- It suggests the ACA’s portability provisions did more than reshuffle coverage; they changed labor-market choices at the margin.

- It avoids the lazy claim that “the ACA caused a startup boom.” The evidence is more modest—and more credible.

Limits still matter. Self-employment is an imperfect proxy for entrepreneurship. Not every new LLC is a high-growth firm. And the strength of the ACA’s effect depends on local market conditions (insurer competition, premium levels) and state policy (Medicaid expansion). So the honest conclusion isn’t that the ACA turned everyone into a founder. It’s that it made the option of founding less punishing for the people previously trapped by medical risk.

3) The 2026 subsidy cliff: why “ballooning premiums” is not an exaggeration

The looming problem is not that the ACA disappears on January 1, 2026. The architecture remains. The problem is that the more generous subsidy rules—enhanced premium tax credits—are scheduled to end after December 31, 2025, reverting on January 1, 2026.

When the enhanced credits lapse, many households face a sharper version of the same reality: the sticker price of coverage is rising, and the cushion between sticker and what you actually pay gets thinner—or vanishes for some.

KFF’s estimate is blunt: without an extension, premium payments for subsidized Marketplace enrollees would rise 114% on average in 2026—about $1,016 more per year, on average.[3] “Average” hides the pain. Premium impacts vary by age, location, plan choice, and income. But as a policy signal, a doubling of what people pay is the kind of shock that changes behavior.

Coverage losses follow affordability losses. CBO estimates that 2.2 million additional people would be uninsured in 2026 if enhanced subsidies are not extended. The Urban Institute projects a larger hit—roughly 4.8 million becoming uninsured in 2026—depending on modeling assumptions.

Congress’s posture worsens the damage. Late-December reporting describes lawmakers heading into year-end without an agreement to extend the subsidies, pushing any possible fix into January 2026. Even if a deal eventually materializes, uncertainty is not neutral. People plan around worst-case scenarios when it comes to healthcare costs.

4) Why this hits entrepreneurs first: cash flow, risk, and timing

Founders don’t fear “costs.” They fear unpredictable fixed costs. Rent is predictable. Software subscriptions are predictable. Health premiums—when policy is uncertain—are not.

The typical early-stage entrepreneur lives in the gap between idea and steady income. Revenue can be uneven. Client contracts slide. One slow quarter becomes two. In that environment, a sudden jump in net premiums isn’t just annoying—it changes the launch calculus.

When net premiums spike, would-be founders tend to respond in a handful of predictable ways:

- Delay the leap. Keep the job, keep the coverage, postpone the venture.

- Downshift the idea. Choose a smaller, safer model that can be run alongside payroll work.

- Go uninsured. A risky bet that can turn a medical event into business failure.

- Rely on fragile stopgaps. Short-term coverage strategies that don’t match the reality of multi-year startup runways.

This is also a geography story. Premiums differ dramatically across states and counties, driven by insurer competition and underlying healthcare prices. KFF has shown that the burden of the subsidy expiration is uneven and, in some places, severe. If you want to understand why entrepreneurship clusters in certain regions, don’t ignore healthcare affordability. It quietly shapes who can afford to take a risk.

One more detail that matters: 2026 sticker prices are already moving. KFF estimates Marketplace insurers are raising premiums substantially for 2026, which means the post-subsidy world would force more households to feel more of that increase directly. When the base cost rises and the subsidy shrinks, the squeeze multiplies.

5) Policy menu: four paths, real tradeoffs

There’s no single “right” policy. There are options with costs and consequences. The key is to evaluate them the way entrepreneurs would: by asking what they do to volatility, not just averages.

Option A: Extend enhanced premium tax credits (multi-year or permanent)

What it does: Prevents the 2026 affordability shock and stabilizes expectations.

Upside: Preserves portability and labor mobility; reduces the odds that would-be founders stay stuck in jobs for coverage.

Downside: Budget impact is real; CBO has shown sizable deficit effects for packages that include subsidy extensions.

Option B: Target the cliff (limit extreme spikes rather than extending everything)

What it does: Focuses resources on households most exposed to losing subsidies or facing very high net premiums.

Upside: Lower fiscal cost than a full extension; reduces the most dramatic premium jumps.

Downside: Adds complexity and new “edges,” where a small income change triggers a big premium change—exactly the kind of instability founders can’t manage.

Option C: Pair a smaller subsidy extension with reinsurance and market stabilization

What it does: Lowers premiums by reducing insurer risk exposure and improving the risk pool.

Upside: Addresses sticker prices, not just what consumers pay; can help stabilize local markets.

Downside: Design matters; poorly targeted stabilization can move costs around without changing underlying drivers.

Option D: Alternative coverage approaches (e.g., association health plans) instead of extension

What it does: Tries to lower premiums for some groups by offering different plan structures.

Upside: Politically appealing to some lawmakers; may offer lower premiums for healthier groups.

Downside: Risk pool fragmentation can raise costs in ACA-compliant markets and weaken the very protections that reduce entrepreneurship lock.

6) Counterarguments (and the parts worth keeping)

“Most entrepreneurs can use a spouse’s plan.” Some can. Many can’t. And the research that finds the strongest ACA effects tends to focus on people without easy alternative sources of coverage—precisely because that’s where lock is binding.

“Subsidies just mask high healthcare costs.” True, subsidies don’t fix hospital pricing or pharmaceutical costs. But they do affect behavior, because behavior responds to net premiums. A sudden doubling of net premiums is a behavioral event, not an accounting detail.

“Extending subsidies is too expensive.” Cost matters. But so do the costs of coverage loss and labor-market rigidity. CBO’s uninsured estimates are not abstract; they imply more uncompensated care and more medical debt risk—both of which hit small business owners hard.

Conclusion: if Congress wants growth, stop treating Marketplace affordability like a footnote

The ACA’s underrated achievement is simple: it made it less dangerous to leave a job. That’s not a cultural shift. It’s a change in the downside math.

Letting enhanced subsidies expire after December 31, 2025 risks rebuilding entrepreneurship lock by making the cost of going independent jump sharply—at the exact moment many households are already staring at rising 2026 sticker premiums. KFF’s estimate of a 114% average premium-payment increase is the kind of shock that reshapes plans in real time.

A serious pro-entrepreneurship agenda would do three things: lock in a multi-year subsidy policy so households can plan, stabilize premiums where markets are thin, and reduce administrative churn so people don’t fall in and out of coverage because their income fluctuates month to month.

In startup terms, this isn’t complicated: you can’t build new businesses on top of a trapdoor.

RELATED ARTICLES

The Missing Middle in Black Entrepreneurship

Black entrepreneurship has expanded dramatically. The next challenge is helping more Black-owned businesses move from self-employment to employer firms and sustainable scale.

Cash Strategy: Put Every Dollar in the Right Place

Your checking account, emergency fund, short-term savings, and investments should not be managed the same way. This cash strategy helps assign every dollar to the right financial job.

Leave Comment

Cancel reply

Gig Economy

Business / Aug 08, 2026

The Missing Middle in Black Entrepreneurship

Black entrepreneurship has expanded dramatically. The next challenge is helping more Black-owned businesses move from self-employment to employer firms and sustainable scale.

By FMC Editorial Team

Personal Finance / Aug 01, 2026

Cash Strategy: Put Every Dollar in the Right Place

Your checking account, emergency fund, short-term savings, and investments should not be managed the same way. This cash strategy helps assign every dollar to the right...

By Article Posted by Staff Contributor

Personal Finance / Aug 01, 2026

Best HYSA: How to Choose Beyond the Highest APY

A competitive interest rate matters, but it is only one part of choosing a high-yield savings account. Compare insurance, fees, access, transfer speed, and promotional conditions.

By Article Posted by Staff Contributor

Personal Finance / Aug 01, 2026

High-Yield Savings vs. CDs, Treasury Bills, and Other Safe Places for Cash

High-yield savings accounts are excellent for accessible cash, but they are not always the best choice. Compare HYSAs, CDs, Treasury bills, money market accounts, and I...

By Article Posted by Staff Contributor

American Middle Class / Aug 01, 2026

High-Yield Savings Accounts: A Safer Home for Your Cash

A high-yield savings account can pay several times the national savings rate while keeping qualified deposits federally insured. Here is how it works, what to watch...

By Article Posted by Staff Contributor

Real Estate / Jul 30, 2026

Mortgage Lock-In Is Freezing the Housing Market

Millions are trapped by 3% mortgages. Learn how mortgage lock-in worsens affordability—and why homeowners are renovating instead.

By FMC Editorial Team

Real Estate / Jul 26, 2026

Is South Florida More Expensive Than New York? The Complete 2026 Relocation Guide

Is South Florida more expensive than New York? Compare housing, taxes, insurance and 104 municipalities before you move.

By Article Posted by Staff Contributor

Personal Finance / Jul 25, 2026

The Time Value of Life Experiences: What Compound Interest Leaves Out,

Money compounds, but life experiences do too. Explore what compound interest leaves out—and how to balance saving with living.

By MacKenzy Pierre

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

By FMC Editorial Team

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

By MacKenzy Pierre

Latest Reviews

Business / Aug 08, 2026

The Missing Middle in Black Entrepreneurship

Black entrepreneurship has expanded dramatically. The next challenge is helping more Black-owned businesses move from...

Personal Finance / Aug 01, 2026

Cash Strategy: Put Every Dollar in the Right Place

Your checking account, emergency fund, short-term savings, and investments should not be managed the same...

Personal Finance / Aug 01, 2026

Best HYSA: How to Choose Beyond the Highest APY

A competitive interest rate matters, but it is only one part of choosing a high-yield...