Envelope Budgeting in a Digital World: How to Use the Old-School Method with Modern Apps

By Article Posted by Staff Contributor

The estimated reading time for this post is 939 seconds

If you’re like most people I work with, you “have a budget.”

It’s somewhere in an app, a dusty Excel file, or that notebook you were excited about in January and stopped updating by March. Meanwhile, your card is still doing laps every week. Groceries creep up. DoorDash creeps in. The credit card quietly fills the gap, and the balance never really goes down.

On paper, you’re budgeting. In real life, you’re still guessing.

That’s the gap envelope budgeting is built to close. It’s old-school. It’s simple. And it hits you where the spreadsheet never does: in the moment, before you swipe.

The twist? Your life runs on direct deposit, autopay, and tap-to-pay. So how do you use a paper-and-cash method in a digital world without turning your whole life into a trip to the ATM?

That’s exactly what we’re going to walk through—especially if you hate spreadsheets and just want a system that actually changes your behavior, not just logs your mistakes.

What Envelope Budgeting Really Is (and What It Isn’t)

Envelope budgeting isn’t a fancy trend. It’s a basic question:

“If I only had this much for groceries, gas, eating out, and fun this month… how would I spend it?”

You break your monthly money into categories—those are your “envelopes.” Each envelope gets a fixed dollar amount. You only spend from that envelope for that purpose. When it’s gone, you’re done. If you keep spending, you have to steal from another envelope on purpose.

That’s the magic. Not the paper. Not the app. The limits.

Most budgets track what already happened:

- “You spent $873 on food last month. Ouch.”

- “You were $200 over in shopping. Again.”

Envelope budgeting flips the script:

- “You get $600 for groceries this month. Period.”

- “You get $200 for eating out. If you blow it early, you feel it.”

You’re not just watching the car crash in slow motion; you’re putting up guardrails before you hit the road.

A few key terms you’ll see in this article:

- Envelope: A category with a set dollar limit (groceries, gas, eating out, kids, etc.).

- Sinking fund: An envelope for non-monthly but predictable expenses—car repairs, holidays, back-to-school, insurance premiums.

- Fixed expenses: Bills that don’t move much month to month: rent, car note, insurance.

- Variable expenses: The wobbly stuff: groceries, gas, restaurants, “I deserve this” shopping.

Envelope budgeting lives mostly in that variable category zone—that’s where money leaks, and where this method does its best work.

Why the Envelope Method Is Back (Thank You, FinTok and Higher Prices)

If you spend any time on TikTok or Instagram, you’ve probably seen it already: “cash stuffing.”

People lay out their paychecks in neat stacks of cash, slide bills into labeled envelopes or binders—Groceries, Gas, Nails, Date Night, Debt—and talk through every single dollar. It’s oddly soothing. It’s also the exact same system your grandmother might have used to keep the lights on and the mortgage paid.

Why is it back?

Because the math stopped working for a lot of households.

Groceries, rent, and everyday expenses have climbed faster than many paychecks. Surveys show the majority of Americans who say they budget still blow past their budgets and patch the hole with credit cards. A big chunk are living paycheck to paycheck even though they’re “doing the right things” on paper.

People aren’t just asking, “What should I do with my money?” anymore. They’re asking, “How do I stop feeling out of control every time I tap my card?”

Envelope budgeting gives you something a pretty budgeting app doesn’t: a hard limit you can see and feel—whether that’s a thin stack of cash or a red number staring back at you in an app.

How the Original Cash Envelope System Works (The Grandma Version)

Let’s start with the classic, no-app, no-spreadsheet, no-frills version. The one that kept families afloat before “fintech” was a word.

Step 1: Figure out your real take-home income.

Not your salary. Not your “I make $80,000” headline. What actually lands in your checking account this month after taxes, insurance, and retirement contributions.

Step 2: Cover the non-negotiables first.

Before you stuff a single envelope, your top priority is survival:

- Housing (rent or mortgage)

- Utilities

- Transportation to get to work

- Minimum debt payments

- Basic insurance

You don’t cut the light bill so you can make your “Brunch” envelope look prettier.

Step 3: Choose the right envelope categories.

This is where most people go wrong. They create 25 envelopes on day one. Don’t.

Start with the categories where you routinely overspend:

- Groceries

- Eating out and takeout

- Gas/transportation

- Personal spending (“Target runs,” coffee, little treats)

- Maybe one kids or family category

That’s enough. You can add more later.

Step 4: Withdraw the cash and stuff the envelopes.

Let’s say you have $2,000 left after fixed bills this month.

You might decide:

- Groceries: $600

- Gas: $250

- Eating out: $200

- Personal: $150

- Kids/Family: $100

- Sinking funds (car repairs, holidays, etc.): $400

- Everything else: $300 buffer

You pull out the cash for your envelopes, label them, and put the money in.

Step 5: Spend from the right envelope. No cheating.

Grocery store? Use the Groceries envelope. Fast food? Eating Out envelope. Gas? Gas envelope.

When the envelope is empty, you have a choice:

- Stop spending in that category, or

- Consciously move money from another envelope and feel the trade-off.

That feeling—that little moment of friction when you realize, “If I do this, something else has to give”—is the power of the system.

You don’t need an MBA for this. You need envelopes, a pen, and the willingness to stop when the cash runs out.

Where Cash Envelopes Break Down in a Digital Life

Let’s be honest. Your life isn’t 1975.

- Your rent is on autopay.

- Your Netflix, cell phone, and car insurance pull automatically.

- Some places barely want to accept cash, and you’re not paying your student loans in twenties.

That’s the first friction with full-on cash envelopes: the world moved on.

Other problems:

- Walking around with a lot of cash is a risk. If your wallet goes missing, that money is gone.

- Cash at home isn’t insured against theft or disasters. Money in a bank (up to the limits) is.

- Most of your larger bills and subscriptions live online, not in a physical envelope.

Then there’s the human side: some people try cash envelopes and keep using their card. If you don’t track both, you can end up double-spending—empty envelopes on the table and a full balance on the credit card.

So yes, the grandma version still works beautifully for some people. But for many middle-class households, going “all cash, all the time” isn’t realistic.

You live in a digital world. Your budgeting method has to live there too.

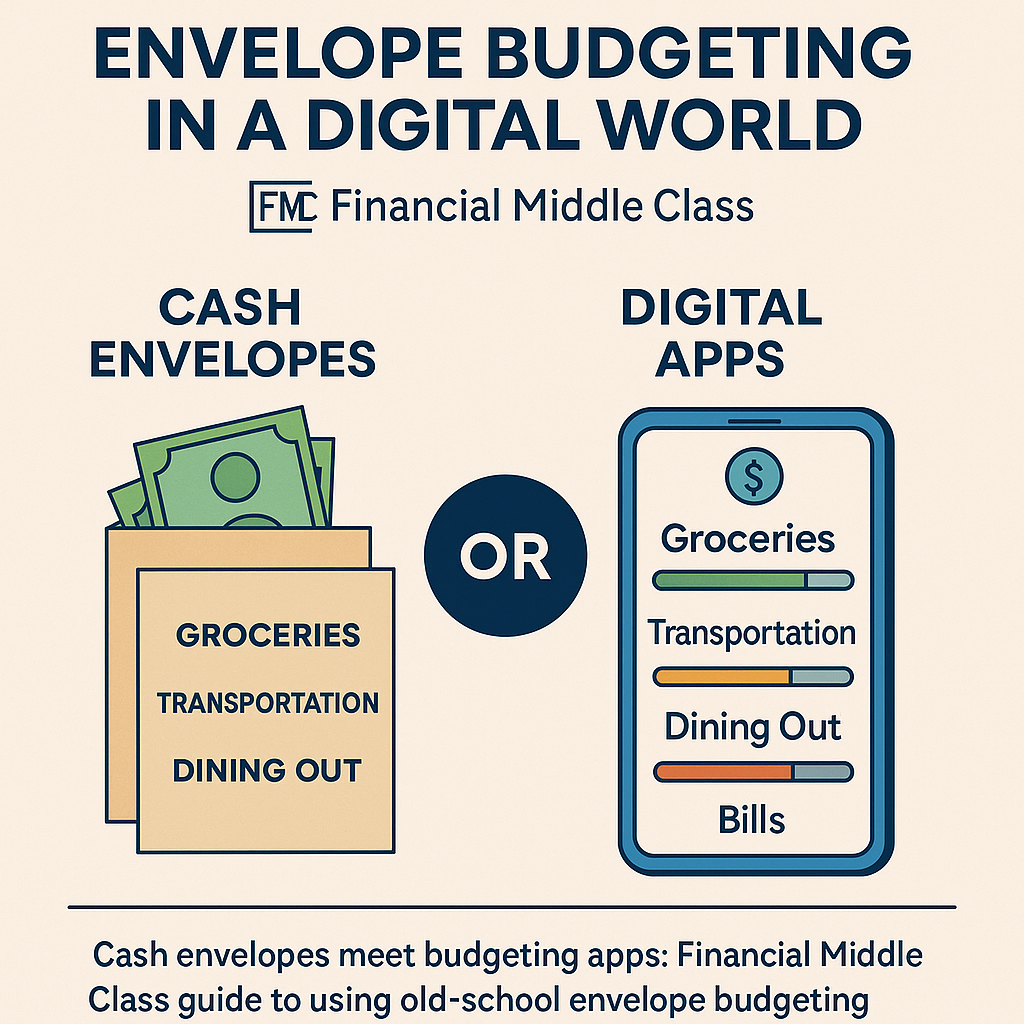

Enter Digital Envelopes: Same Logic, New Tools

Digital envelope budgeting takes the exact same idea and moves it onto your phone or laptop.

Instead of paper envelopes, you have categories inside an app:

- Groceries

- Gas

- Eating Out

- Debt Payoff

- Holidays

- Car Repairs

You assign your dollars to those categories inside the app. Every time you get paid, you “stuff” the digital envelopes. Every time you spend, you subtract from that envelope—either automatically (if your app syncs with your bank) or manually.

The key difference from a generic “spending tracker” is this:

You assign the money before you spend it. You’re not just looking back at a mess; you’re telling your dollars where to go on purpose.

A lot of modern tools are built on what’s called zero-based budgeting: every dollar that hits your account gets a job. None of it gets to just sit there as “miscellaneous” or “we’ll see.”

That doesn’t mean your life becomes a spreadsheet. It means your money has marching orders.

A Quick Tour of Tools (For People Who Hate Spreadsheets)

You do not have to become a software engineer to use this stuff. Think of these tools as digital envelope binders.

Here’s a quick tour in plain language:

Goodbudget

Digital envelopes in a simple app. You create envelopes, assign money, and track your spending. Good if you want structure without 1,000 features. It’s also friendly for couples who want to share a budget.

Actual Budget

Think: envelope/zero-based budgeting with a big focus on privacy. Your data can stay local on your device instead of being shipped to somebody’s cloud. Good for people who are nervous about connecting their accounts or want something fast and minimal.

RealBudget

Another straightforward envelope-style tool. You create envelopes, track spending, and keep it simple. Less about “advanced reports,” more about keeping you honest.

YNAB (You Need A Budget)

This one doesn’t call itself an envelope app, but it might as well. It’s built around giving every dollar a job, moving money between categories when reality hits, and staying one month ahead. Great for people who want a deep system and are willing to climb a small learning curve.

Most of these apps offer:

- A way to set up categories (envelopes).

- A way to assign dollars as they come in.

- A way to track transactions against your plan.

Some will connect to your bank and pull transactions automatically. Others let you skip the bank connection and log spending yourself.

Here’s the part nobody says out loud: you don’t need the perfect app.

Pick one that feels understandable. If the tutorial makes your head hurt, it’s not your app. The method is what matters. You can always change tools later.

The Hybrid Play: Cash for Problem Categories, Apps for the Rest

All-or-nothing thinking kills more budgets than bad math.

You don’t need to go “all cash” or “all digital.” In fact, for most middle-class households, the sweet spot is a hybrid system:

- Cash envelopes for 1–3 problem categories where you really need to feel the money leaving.

- Digital envelopes in an app for fixed bills and savings goals.

Picture this:

A two-income family with kids. Most bills are on autopay. The pain points are:

- Groceries (impulse buys, wasted food)

- Eating out (weeknights when everyone’s tired)

- Amazon “just because” orders

Here’s a hybrid approach that actually fits their life:

- Rent, utilities, insurance, subscriptions → live in digital envelopes inside an app. The money is planned and set aside there.

- Groceries, Eating Out, Personal Spending → full-on cash envelopes. They pull the monthly or biweekly amount for those categories and spend only from those envelopes.

- Sinking funds like holidays, car repairs, back-to-school → digital envelopes in the app they fund every paycheck.

Now the dangerous categories have hard limits they can touch. Everything else stays modern and automated.

That’s what a realistic envelope system looks like in 2025. Not a TikTok challenge. A blended setup that respects the fact that your life runs online.

Step-by-Step: Building Your Envelope System in 7 Moves

Let’s get practical. Here’s how you set this up without a spreadsheet, without a mental breakdown, and without trying to budget every penny of your life on day one.

- Get honest about your take-home income.

Add up what actually hits your account in a normal month. If your income is variable, look at the last 3–6 months and use a conservative average.

- Cover the non-negotiables first.

List:

- Housing

- Utilities

- Transportation

- Minimum debt payments

- Insurance

These get funded before you touch a single envelope.

- Pick 3–5 variable categories to envelope first.

Circle the trouble spots. Common ones:

- Groceries

- Eating out and takeout

- Gas/transportation

- Personal “fun money”

- Kids/activities

Start here. Do not try to envelope 25 categories. You’re building a new habit, not building a NASA control room.

- Choose your format: cash, digital, or hybrid.

Ask yourself:

- Do I overspend more when I tap or when I swipe?

- Do I freak out at the idea of carrying cash?

- Am I more likely to open an app or look in my wallet?

If you’re very card-heavy and rarely touch cash, a digital-first or hybrid system probably makes more sense. If swiping cards is your weakness and you’re willing to make a big change for a few months, cash envelopes for a couple of categories will wake you up fast.

- Set amounts based on your real history, not fantasy.

Pull up 1–3 months of bank and card statements and see what you actually spent in your chosen categories.

If you’ve been spending $900 a month on groceries, don’t pretend you can drop to $400 overnight without a plan. Maybe you set your grocery envelope at $750 the first month, then work it down if that feels doable.

The envelope is a tool, not a punishment. It needs to be strict enough to matter and realistic enough to maintain.

- Run a 30-day envelope experiment.

Commit for one month:

- Stuff the envelopes (physical or digital).

- Spend only from the right envelope.

- When an envelope runs low, adjust your behavior instead of reaching for a credit card.

You’re not trying to “win” some challenge. You’re trying to learn:

- Where does the money actually go?

- Which category runs out first?

- Which envelope always has money left?

At the end of 30 days, the point isn’t perfection. It’s insight.

- Adjust and extend to 60–90 days.

After the first month:

- Increase categories that were unrealistically low.

- Decrease categories where you always had extra.

- Add one or two sinking funds (car repairs, holidays) if you’re ready.

By 60–90 days, most people have a much clearer picture of their spending—and the envelope system feels less like a stunt and more like their new normal.

Common Envelope Budgeting Fails (And How to Fix Them)

Let’s talk about the ways this can go sideways, because they will show up.

Fail #1: Too many envelopes.

If you start with envelopes for everything—haircuts, dog treats, school snacks, coffee, snacks, date night—you will burn out.

Fix: Start with 3–5. Add more only when the first set feels automatic.

Fail #2: Ignoring irregular expenses.

You get blindsided by car repairs, holidays, or back-to-school shopping. The envelopes look good… until that one big expense nukes your whole month.

Fix: Add sinking funds once you have basic envelopes in place. Even $25–$50 a month into a “Car Repair” envelope is better than pretending your 10-year-old car will never need work.

Fail #3: Treating it as a 30-day TikTok challenge only.

You go all-in for a month, film your cash-stuffing videos, and stop as soon as the novelty wears off.

Fix: Decide upfront that the first 30 days are practice. Months 2 and 3 are where you actually judge the method. Systems beat stunts.

Fail #4: Going “app-only” and never opening the app.

You download a beautiful digital envelope tool, connect your bank, and then… ignore it.

Fix: Set a weekly money date. Same time every week, 20–30 minutes. You and your envelopes. Update, adjust, and move on with your life.

Fail #5: Marrying the app instead of the method.

Apps shut down. Mvelopes did. Others have merged, changed pricing, or overhauled features. If your entire “budget” is an app you don’t understand, you’re at risk.

Fix: Once a quarter, export your data if the app allows it, and keep a simple list of your categories and target amounts somewhere you control—a note on your phone, a PDF, a piece of paper. If your app disappeared tomorrow, you should be able to rebuild your envelope system in under an hour.

Data, Privacy, and the Fine Print

Any time you connect your bank accounts to an app, your data is moving through extra hands. Most reputable tools encrypt and limit access, but “secure” doesn’t mean “risk-free.”

A few simple guidelines:

- If you’re uncomfortable linking accounts, pick a tool that allows manual entry or local storage.

- Read the short version of the privacy policy. You don’t need a law degree, but you do need to know if they’re selling your data to third parties.

- Get familiar with the export button. If there’s no easy way to download your data… that should give you pause.

Again, the goal is not to live in fear. It’s to build a system you understand and control, not just one you log into.

How to Make Envelope Budgeting Stick

Budgets die in silence. The way you keep this one alive is by giving it a rhythm.

Weekly money check-in

Once a week, same day, same general time:

- Refill cash envelopes if you’re doing physical.

- Update your digital envelopes or reconcile transactions.

- Look at which envelopes are burning the fastest.

- Make tiny adjustments instead of waiting for a blowup.

Handling irregular income

If your income bounces around, use a priority list for funding envelopes:

- Survival bills (housing, utilities, basic food, transportation).

- Minimum debt payments.

- Essential variable envelopes (groceries, gas).

- Sinking funds (car repairs, medical, holidays).

- Fun money.

When the money is gone, you stop moving down the list. That’s envelope thinking at the income level.

Emotionally, give yourself room to be human

You will overspend one month. You will raid one envelope to rescue another. You might have a week where the gas envelope hits zero and you’re annoyed.

None of that means the system “doesn’t work.” It means real life is happening. The win is you noticed the problem early and had to make a conscious trade-off instead of letting the credit card quietly absorb it.

Pick a Lane and Give It 90 Days

You don’t need more financial noise. You need a method that forces you to admit, in advance, what you’re actually willing to spend on food, gas, fun, and all the little leaks that are killing your savings.

Envelope budgeting does that.

- If you need a shock to the system, start with cash envelopes for your worst 1–3 categories and watch how differently you move when the bills are visible.

- If you can’t imagine living without tap-to-pay, set up digital envelopes in an app and let it do the math while you focus on behavior.

- If you’re living in the messy middle like most of the Financial Middle Class, build a hybrid system that keeps your autopay bills digital and your problem categories on a short cash leash.

Don’t overthink it. Don’t go hunting for the “perfect” app. Don’t design the world’s most complicated envelope spreadsheet.

Pick three to five envelopes. Decide whether they live in your wallet or on your phone. Give the system 60–90 days.

If you’ve been budgeting for years and still feel broke, you don’t need another tab in Excel. You need a limit you can see—and a plan you can actually stick to in the real world you’re living in now.

RELATED ARTICLES

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

Leave Comment

Cancel reply

Gig Economy

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

By FMC Editorial Team

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

By MacKenzy Pierre

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan to escape 25% APR debt.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

What To Do If You Get Fired With an Outstanding 401(k) Loan

Fired with a 401(k) loan? Avoid taxes, offsets, and deadline traps with this step-by-step checklist. Read now.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

The Real Math of Money in Relationships

Split finances without resentment. Any couple, any income ratio. Use the worksheet + rules—start today.

By Article Posted by Staff Contributor

American Middle Class / Feb 03, 2026

Investing or Paying Off the House?

Invest or pay off your mortgage? See a $500k example with today’s rates, dividends, and peace-of-mind math—then choose your plan.

By Article Posted by Staff Contributor

American Middle Class / Jan 30, 2026

Gold, Silver, or Bitcoin? Start With the Job—Not the Hype

Gold, silver or Bitcoin? Learn what each is for—and how to size it—before you buy. Read the framework.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Florida Homeowners Pay the Most in HOA Fees

Florida HOA fees are surging. See what lawmakers changed, what’s next, and how to protect your budget—read before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Why So Many Homebuyers Are Backing Out of Deals in 2026

Why buyers are backing out of home deals in 2026—and how to avoid costly surprises. Read the playbook before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 28, 2026

How Money Habits Form—and Why “Self-Control” Is the Wrong Villain

Learn how money habits form—and how to rewire spending and saving using behavioral science. Read the framework and start today.

By FMC Editorial Team

Latest Reviews

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs....

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market...

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan...