The One-Income Family Is Becoming a Luxury. Here’s the Salary It Takes Now.

By Article Posted by Staff Contributor

The estimated reading time for this post is 859 seconds

One Income: Salary Needed for a Stay-at-Home Parent

The one-income family used to feel normal in the American middle class. Now it can feel like a luxury tier—priced just out of reach even for people who do everything “right.”

If you’re asking, “How much does one parent need to earn so the other can stay home with the kids?” you’re not being dramatic. You’re being honest about the math.

January 18, 2026

This post uses reputable public benchmarks and county examples to help you run your number. Always verify costs and benefits in your location.

One income is a system, not a salary. The paycheck has to carry taxes, benefits, risk, and the fact that there’s only one engine.

In many counties, the baseline starts near six figures. That’s not lifestyle inflation. That’s the current price of basic stability for a family of four in many places.

The second paycheck can shrink fast. Child care, commuting, and “working costs” can turn a salary into a smaller net than people expect.

One-income households need more runway. If one job goes down, the whole household takes the hit—so the emergency plan has to be stronger.

Test the plan before you jump. A 90-day trial can confirm the math without forcing a life-altering quit decision.

Intro: The One-Income Question

Somewhere tonight, two adults are standing in the kitchen doing the kind of math nobody posts on Instagram. Not “Where should we vacation?” math. The real stuff: mortgage, groceries, car insurance, the school calendar, the random fees that show up like they live in your house.

And then the question lands—quiet, heavy, and extremely modern: How much would one of us need to earn so the other can stay home and raise the kids?

Not because you’re trying to cosplay the 1950s. Because child care is expensive. Because two full-time schedules are breaking families at the seams. Because stability is starting to feel like something you have to “qualify” for.

This is not a guilt trip. It’s a clear-eyed look at the one-income family in 2026 America, with real public benchmarks and a worksheet you can use tonight.

Why It’s Harder Now

The squeeze isn’t your imagination. The biggest chunks of household spending are the things you can’t cancel. According to the Bureau of Labor Statistics, in 2024 the average household spent about 33.4% of annual expenditures on housing and 17.0% on transportation. Food was 12.9% and healthcare was 7.9%. (That’s not “fun money.” That’s life money.) BLS Consumer Expenditures—2024

When housing and transportation take up that much oxygen, the one-income dream doesn’t just get harder. It gets repriced into a different social class. You can be responsible, employed, and still feel like you’re one surprise away from the kind of stress that changes your personality.

What “One Income” Really Means

Most people say “one income” and mean “one salary.” But the salary is only the loudest part of the system. One income also means one set of benefits, one retirement match, one employer, one schedule, and one point of failure.

Health insurance is the biggest trap because it hides in plain sight. KFF’s 2025 Employer Health Benefits Survey reported average annual premiums for employer-sponsored family coverage at $26,993, with workers contributing an average of $6,850. That’s not a small line item. That’s a bill disguised as a perk.

So when you ask, “How much do we need?” the right question is: how much do we need to keep the whole system upright when one paycheck disappears?

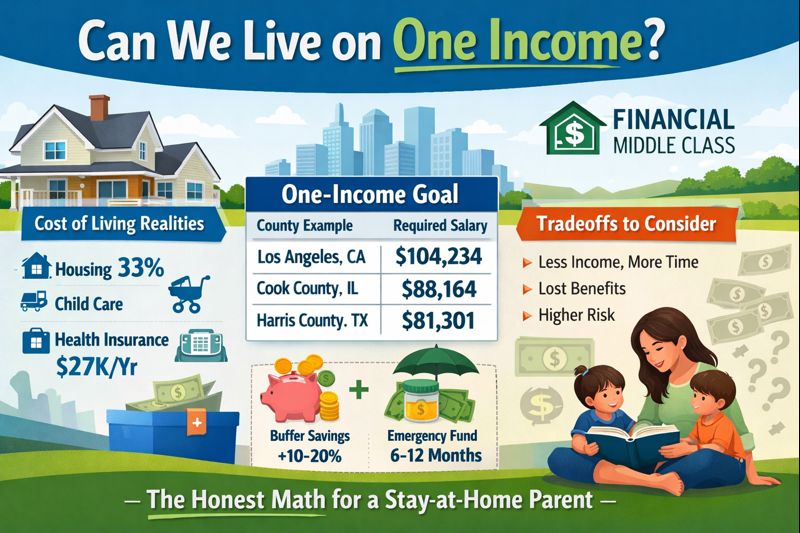

The Baseline Number (MIT Living Wage Calculator)

If you want a starting point that isn’t vibes, the MIT Living Wage Calculator is one of the cleanest public tools available. It estimates the local cost of basic needs, then adds payroll and income taxes using a consistent methodology. MIT notes its data was last updated on February 10, 2025.

For this article, the relevant family type is the one that matches the stay-at-home-parent setup: 2 adults, 2 children, 1 working adult. MIT publishes “required annual income after taxes” and “annual taxes” for each county. When we add those together, we get a practical “before-tax requirement” for what the one working parent needs to earn.

County Reality Check

Below are examples from MIT’s county pages for a household with 2 adults, 2 children, and 1 working adult. These are baseline estimates, not “comfortable living” numbers. They’re meant to cover basic needs plus taxes in that location.

| County (Example) | After-tax required income | Estimated annual taxes | Approx. before-tax requirement (sum) | Source |

|---|---|---|---|---|

| Los Angeles County, CA | $92,497 | $11,737 | $104,234 | MIT LA County |

| Palm Beach County, FL | $81,747 | $8,626 | $90,373 | MIT Palm Beach |

| Cook County, IL | $77,034 | $11,130 | $88,164 | MIT Cook County |

| Franklin County, OH | $75,514 | $8,936 | $84,450 | MIT Franklin County |

| Harris County, TX | $74,209 | $7,092 | $81,301 | MIT Harris County |

Here’s what makes those numbers sting: the U.S. Census Bureau reports median household income was $83,730 in 2024. That’s the middle household, not the struggling edge.

| County (Example) | Approx. before-tax requirement | Compared to $83,730 median |

|---|---|---|

| Los Angeles County, CA | $104,234 | +$20,504 |

| Palm Beach County, FL | $90,373 | +$6,643 |

| Cook County, IL | $88,164 | +$4,434 |

| Franklin County, OH | $84,450 | +$720 |

| Harris County, TX | $81,301 | -$2,429 |

That’s the receipt. In many places, a one-income family of four requires the working parent to earn at or above what the “middle” household makes nationally. If that makes your plan feel hard, it’s because it is.

Child Care: Villain & Plot Twist

Child care is the reason so many families start dreaming about one parent staying home. Child Care Aware reports the national average price of child care in 2024 was $13,128.

But the plot twist is brutal: child care is expensive enough to push families toward a stay-at-home setup, while the overall cost of living is high enough to block the stay-at-home setup. You end up working to pay for the privilege of working.

Care.com’s 2024 Cost of Care Report puts a human number on what parents feel: survey respondents said they spend 24% of household income on child care, while HHS considers child care “affordable” when it costs no more than 7% of household income.

The Second-Income Mirage

This is where the kitchen math turns into an argument. One parent sees the second paycheck and says, “We need it.” The other parent looks at child care, commuting, taxes, and convenience spending and says, “Do we?”

Sometimes the second income is absolutely worth it. Sometimes it’s real money. But sometimes it’s a stress subscription with a small refund.

| Line item | Parent B works | Parent B stays home |

|---|---|---|

| Gross pay (example) | $45,000 | $0 |

| Taxes (varies by household) | -$8,000 | $0 |

| Child care (national average) | -$13,128 | $0 |

| Commute + “working costs” (varies) | -$3,000 | $0 |

| Approx. net added to household | $20,872 | $0 |

This is not saying “quit your job.” It’s saying stop treating gross pay like the number that matters. The number that matters is what the household keeps after the costs of earning that money show up.

Your One-Income Number (do this in 10 minutes)

The goal isn’t a perfect number. The goal is a number that doesn’t collapse the first time life happens. Start with what you must pay, subtract what disappears, add what increases, then add a buffer so you’re not living on a knife edge.

Step 1: Add monthly must-pays

Mortgage/rent, utilities, groceries, car payments, insurance, debt minimums, phone/internet, medical, and anything that will still exist if one paycheck disappears.

Monthly Must-Pays = ________

Step 2: Subtract costs that disappear

Paid child care, commuting/parking, work clothes, and the “we’re too tired to cook” spending that quietly comes with two exhausted adults.

Minus Disappearing Costs = ________

Step 3: Add costs that increase (benefits cliff)

Health insurance changes, higher premiums, higher deductibles, and anything you were getting through the second employer (HSA, match, subsidized coverage).

Plus Increased Costs = ________

Step 4: Add buffer + retirement floor

Add a cushion (even 10% is something) so the plan has oxygen. Then set a retirement “floor” so you don’t accidentally pause the future for years.

Buffer + Retirement Floor = ________

Step 5: Convert to a gross salary target

Multiply your final monthly number by 12, then sanity-check against your paystub and benefits. If the one working parent’s job is the benefits carrier, price that carefully.

Annual “Need” (before taxes) ≈ ________

Risk & Emergency Runway

A one-income plan isn’t just about paying bills. It’s about surviving shocks. When there’s only one paycheck, you don’t get the cushion of “the other job” during a layoff, a health event, or a slow hiring cycle.

| Household setup | Runway that avoids panic | What it protects you from |

|---|---|---|

| Two-income household (stable jobs) | 3–6 months | Layoffs, short gaps, surprise bills |

| One-income household (stable job) | 6–9 months | Single-point failure risk |

| One-income household (variable income) | 9–12 months | Income swings + longer recoveries |

This isn’t fearmongering. It’s a respect for reality. A one-income family can be beautiful and stable, but it needs more runway because it has fewer backups.

3 Ways Families Make It Work

Most families who pull this off don’t do it with one heroic salary and a motivational quote. They do it with structure. They pick a setup that matches their stress points and their risk tolerance.

| Setup | Money | Time with kids | Stress profile | Long-term career impact |

|---|---|---|---|---|

| One full-time income + one stay-at-home parent | Lower cash, simpler logistics | Highest | Higher money risk, lower logistics stress | Higher for the at-home parent unless you plan re-entry |

| One full-time + one part-time/shift work | More cash, some benefits possible | High | Very tiring but often workable | Medium |

| Two full-time incomes + child care | Highest cash potential | Lowest | High logistics stress | Lower, but burnout risk rises |

If none of these feels great, that’s not you failing. That’s you noticing the truth: American families are being asked to buy stability at premium prices.

Protect the Stay-at-Home Parent

Here’s my skeptical note, delivered with respect: love is not a benefits package. If one parent stays home, the household has to treat that role like real labor that deserves real protection.

That means keeping retirement contributions alive in some form, keeping credit active, and building a re-entry plan so the at-home parent doesn’t become financially invisible. It also means talking honestly about power. Money changes relationships if you pretend it won’t.

And remember, this is not just a “mom” topic anymore. Pew Research Center found that in 2021, 18% of parents didn’t work for pay, and the share of stay-at-home parents who are dads has grown.

The 90-Day One-Income Test Drive (no quitting required)

Week 1: Freeze the future budget

Pick the “future one-income” spending level you want to test. Pay bills from the primary paycheck only. Park the second paycheck in savings and don’t touch it.

Weeks 2–4: Track what breaks the plan

Write down the friction points: groceries, gas, school fees, medical costs, surprise spending. Don’t moralize it. Collect the truth.

Month 2: Stress-test benefits and backup care

Confirm health insurance if one parent stops working. Price the difference. If child care is the driver, test backup options like part-time care, staggered shifts, or family support.

Month 3: Decide with evidence

If you can run the household on one paycheck for 90 days and still build savings, you’ve proven the plan. If you can’t, you didn’t fail—you learned early and cheaply.

Real questions middle-class families ask

Is it smarter to stay home if my paycheck mostly covers child care?

Sometimes, yes. But don’t stop at child care. Include taxes, commuting, benefits, and the long-term cost of stepping out of the workforce. The 90-day test drive gives you evidence instead of guesses.

What if the stay-at-home parent carried the health insurance?

That’s the benefits cliff. Price replacement coverage and out-of-pocket costs before you decide. A “good salary” can get eaten by premiums and deductibles if coverage worsens.

How much should we save before going one-income?

Because one income is one point of failure, many families aim for a longer runway than they would on two incomes. The right runway depends on job stability, health risk, and how fast you could replace income.

What if we’re in a high-cost area and the number feels impossible?

Then the decision becomes structural: housing, commute, job market, and child care alternatives. Some families solve it with part-time work, staggered shifts, downsizing, or relocating. None of those are easy, but they are real levers.

How do we protect the stay-at-home parent financially?

Keep retirement contributions alive, keep credit active, and keep a re-entry plan. Treat the role like it deserves protections, not like it’s invisible labor.

What’s your one-income dealbreaker?

If you’ve run this math—or lived it—what surprised you most: child care, housing, health insurance, or the risk of relying on one paycheck?

The one-income dream didn’t die because parents stopped valuing family. It got priced out. And if you’re staring at your budget wondering why something “normal” feels impossible, that’s not you failing. That’s the bill telling the truth.

RELATED ARTICLES

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

Leave Comment

Cancel reply

Gig Economy

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs. Read now.

By FMC Editorial Team

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market isn’t the economy—read now.

By MacKenzy Pierre

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan to escape 25% APR debt.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

What To Do If You Get Fired With an Outstanding 401(k) Loan

Fired with a 401(k) loan? Avoid taxes, offsets, and deadline traps with this step-by-step checklist. Read now.

By Article Posted by Staff Contributor

American Middle Class / Feb 09, 2026

The Real Math of Money in Relationships

Split finances without resentment. Any couple, any income ratio. Use the worksheet + rules—start today.

By Article Posted by Staff Contributor

American Middle Class / Feb 03, 2026

Investing or Paying Off the House?

Invest or pay off your mortgage? See a $500k example with today’s rates, dividends, and peace-of-mind math—then choose your plan.

By Article Posted by Staff Contributor

American Middle Class / Jan 30, 2026

Gold, Silver, or Bitcoin? Start With the Job—Not the Hype

Gold, silver or Bitcoin? Learn what each is for—and how to size it—before you buy. Read the framework.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Florida Homeowners Pay the Most in HOA Fees

Florida HOA fees are surging. See what lawmakers changed, what’s next, and how to protect your budget—read before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 29, 2026

Why So Many Homebuyers Are Backing Out of Deals in 2026

Why buyers are backing out of home deals in 2026—and how to avoid costly surprises. Read the playbook before you buy.

By Article Posted by Staff Contributor

American Middle Class / Jan 28, 2026

How Money Habits Form—and Why “Self-Control” Is the Wrong Villain

Learn how money habits form—and how to rewire spending and saving using behavioral science. Read the framework and start today.

By FMC Editorial Team

Latest Reviews

American Middle Class / Feb 18, 2026

How Wealth Is Passed Across Generations in the United States: Mechanisms, Evidence, and the Policy Debate

How wealth passes between generations—trusts, taxes, and the debate. Get the facts, figures, and tradeoffs....

American Middle Class / Feb 16, 2026

The S&P 7,000: How Wall Street Disconnects from Main Street

S&P 7,000 can rise while wages, benefits, and towns fall behind. See why the market...

American Middle Class / Feb 16, 2026

The “Resilient Consumer” Is Real—But So Is the Interest Bill

Credit card balances are rising as savings fall. See what it means—and the 30/60/90 plan...